Managing import-related risks is no longer optional – it’s necessary. Trade credit insurance (TCI) helps businesses protect against unpaid invoices and political instability, covering up to 95% of losses. With U.S. bankruptcies at their highest since 2010 and tariff fluctuations creating financial uncertainty, TCI provides a safety net while also improving access to financing.

Here’s what you need to know:

- Coverage: TCI protects against buyer insolvency, payment delays, and political risks like currency inconvertibility or trade embargoes.

- Compliance: U.S. importers must follow strict regulations, including Title 19 CFR and EXIM Bank requirements, to ensure insurance validity.

- Exclusions: Policies exclude non-U.S.-made goods, unapproved Letters of Credit, and losses without pre-shipment endorsements.

- Financial Impact: Insured receivables allow businesses to secure better financing terms, with advance rates up to 85% and lower borrowing costs.

Trade Credit Insurance Coverage Rates and Financial Benefits for Importers

Core Elements of Import Insurance Rules

What Trade Credit Insurance Covers

Trade credit insurance acts as a safety net for businesses, protecting them from financial losses caused by unpaid invoices and political instability. On the commercial side, it covers extended defaults, ensuring businesses aren’t left without payment for goods or services provided. Political risks, on the other hand, include scenarios like currency restrictions, license cancellations, expropriation, wars, or revolutions.

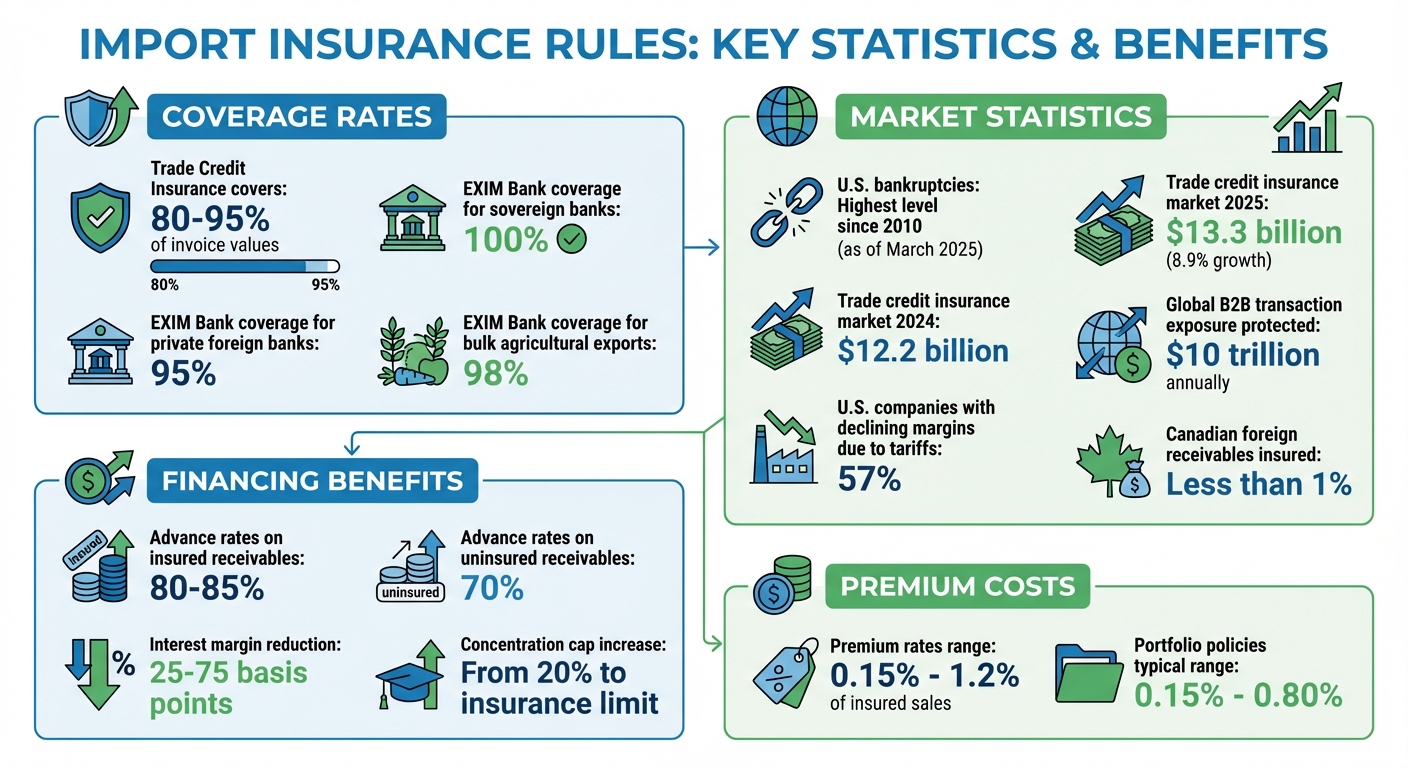

There’s also specialized insurance for situations where overseas banks fail to honor irrevocable Letters of Credit. The Export-Import Bank of the United States (EXIM) assumes a significant portion of the risk: up to 100% for sovereign banks, 95% for private foreign banks, and even 98% for bulk agricultural exports.

Another layer of protection is pre-shipment coverage, which safeguards manufacturers against costs incurred for goods that can’t be shipped due to political events. Ken Click, a Business Development Specialist at EXIM, emphasizes the importance of pre-shipment endorsements:

If a ban or regulation is instated before the shipment date and there is no Pre-Shipment endorsement on the policy, the exporter becomes ineligible for coverage.

This coverage is particularly important for custom-made or long-lead-time goods, where disruptions can lead to significant financial losses.

Compliance Requirements for U.S. Importers

U.S. importers must navigate strict regulations to ensure their insurance policies are valid and effective. These rules are primarily outlined under Title 19 of the Code of Federal Regulations, which governs customs procedures. For instance, under 19 CFR 142.26, importers who fail to pay duties or provide a valid reason for non-payment risk losing immediate release privileges, which can halt imports entirely.

Transactions involving Letters of Credit must align with the Uniform Customs and Practice for Documentary Credits (UCP 600), a set of guidelines established by the International Chamber of Commerce in 2007. EXIM insurance policies exclude certain non-standard structures like revocable or conditional Letters of Credit. Additionally, banks must secure an Exporter Certificate to confirm that goods were made in and shipped from the U.S., ensuring compliance with EXIM’s requirement that products contain at least 50% U.S. content (excluding markup).

Importers also need to coordinate with Partner Government Agencies (PGAs), which oversee specific commodities for safety and compliance. For smaller shipments, the Section 321 de minimis rule under the Tariff Act of 1930 provides an exemption for imports valued at $800 or less, potentially reducing insurance and bonding needs.

Under 16 CFR § 1009.3, federal law designates importers as the "manufacturer of record" for consumer goods when foreign suppliers are beyond the reach of U.S. courts. Gordon B. Coyle, CEO of The Coyle Group, explains:

Under 16 CFR § 1009.3… importers have ‘responsibilities and obligations comparable to those of domestic manufacturers.’ When a foreign manufacturer cannot be reached through U.S. jurisdiction, liability shifts fully to the importer.

This means importers bear full responsibility for any injuries or damages caused by their products, making product liability insurance a necessity.

Understanding Policy Exclusions

While trade credit insurance offers broad protection, it comes with several exclusions that businesses must be aware of. For instance, if a government imposes a ban or regulation before the shipment date, coverage won’t apply unless a pre-shipment endorsement is in place. Shipping goods under such circumstances without this endorsement leaves businesses exposed to full financial risk.

EXIM policies also have strict origin requirements: goods must be made in and shipped from the United States to qualify for coverage. Products manufactured abroad are not eligible. In addition, failing to notify the insurer promptly when a loss occurs can jeopardize a claim. For example, if political risks arise while goods are in transit, policyholders must contact the insurer to explore options like redirecting the shipment. Without this step, claims may be denied.

Sanctions enforced by the Office of Foreign Assets Control (OFAC) further limit coverage. Importers dealing with sanctioned countries may face higher premiums or outright denial of coverage. Additionally, standard General Liability policies often exclude coverage for goods made outside the U.S., so importers shouldn’t assume their existing insurance extends to such products.

Other exclusions include non-standard Letters of Credit and situations where international buyers were legally unable to import the goods at the time of shipment. While documented interest on defaulted payments may be covered, this is typically limited to a 180-day period following the foreign bank’s default.

sbb-itb-b840488

How Import Insurance Rules Affect Businesses

Protecting Against Financial Risks

Trade credit insurance has reshaped how businesses manage their accounts receivable. Marc Wagman, Managing Director of Credit and Political Risk at Gallagher, explains its importance:

Typically, receivables – the lifeblood of a company fueling cash flow – are the largest uninsured asset on the balance sheet. Having the insurance greases the wheels of global trade.

These policies typically cover 80% to 95% of invoice values when buyers fail to pay due to insolvency or prolonged defaults. This safety net becomes especially crucial during economic downturns. For instance, U.S. bankruptcies through March 2025 reached their highest level since 2010. Yet, in Canada, where international sales account for about 40% of export revenue, less than 1% of foreign receivables are insured. This leaves billions of dollars in cash flow unprotected.

The financial impact of unpaid invoices isn’t the only concern. A July 2025 survey revealed that 57% of U.S. companies experienced declining gross margins directly tied to rising tariff costs. When suppliers in high-tariff regions struggle financially, insurers like Export Development Canada report higher loss ratios. Without insurance, businesses either absorb these losses or reserve capital that could otherwise fuel growth and innovation. By mitigating these risks, trade credit insurance also unlocks better trade financing opportunities.

Effects on Trade Financing and Credit Access

Insured receivables open doors to more favorable financing terms. Businesses with trade credit insurance policies can secure advance rates of 80–85% on insured receivables, compared to just 70% for uninsured accounts. Additionally, concentration caps – usually limiting any single customer to 20% of the borrowing base – can expand to match the insurance limit when receivables are covered. This also lowers borrowing costs, with interest margins dropping by 25–75 basis points.

This financing edge is critical since many businesses depend on credit lines tied directly to their insurance limits. If an insurer cancels coverage, the business might immediately lose its ability to fund transactions. Trade credit insurers currently safeguard an estimated $10 trillion in B2B transaction exposure annually, underscoring their role in global commerce. Sarah Murrow, President and CEO of Allianz Trade Americas, highlights this importance:

As was demonstrated during COVID, trade credit insurance is vital to keeping liquidity in supply chains. It is the glue that keeps world trade going.

Beyond improving financing, these policies also help businesses adapt to shifting political and economic landscapes.

Responding to Political and Economic Changes

In addition to financial benefits, trade credit insurance offers structured support for navigating geopolitical challenges and trade disputes. Political risk coverage protects businesses against issues like currency inconvertibility, expropriation, war, and the loss of import/export licenses. If political events disrupt transit, insurers can assist in redirecting shipments.

The global trade credit insurance market is expected to grow from $12.2 billion in 2024 to $13.3 billion in 2025, reflecting an 8.9% annual growth rate. This surge reflects businesses seeking protection against ongoing disruptions, such as unpredictable tariff changes and trade disputes. Even historically reliable trade routes, like Canada-U.S. commerce, face reevaluations due to retaliatory tariffs and reciprocity policies.

Despite economic uncertainty, the market remained in a "prolonged soft market" through late 2025, with competitive pricing and high capacity due to low post-pandemic claims. However, Ian Watts, Credit Risk Specialty Growth Leader at WTW, notes that external risks are always part of the equation:

Anything in the external economic environment creating additional risk for companies – tariffs, high interest rates, geopolitical tensions – will be plugged into the algorithms and risk assessments.

Best Practices for Compliance and Coverage

Selecting the Right Insurance Policy

Picking the right trade credit insurance policy starts with understanding the available options. Businesses can choose to cover their entire portfolio (Whole Turnover), focus on a specific group of key accounts (Named Buyer), or insure a single high-value transaction (Single Buyer). This decision lays the groundwork for a solid risk management strategy. Whole Turnover policies often come with better pricing and are viewed favorably by banks, while Named Buyer policies help manage concentration risk.

Another key consideration is the type of policy limits. Cancellable limits allow insurers to adjust or withdraw coverage for future shipments, offering flexibility but less certainty. On the other hand, non-cancellable limits remain fixed throughout the policy period, making them more reliable when using insured receivables as collateral. Premium rates generally fall between 0.15% and 1.2% of insured sales volume, with portfolio policies typically ranging from 0.15% to 0.80%.

To secure the best terms, prepare a thorough submission package before requesting quotes. Include audited financial statements, a 12-month accounts receivable aging report, a list of top buyers by exposure, and historical bad-debt records. If you’re planning to use the policy to negotiate better bank terms, review the specimen policy wording with your lender ahead of time.

Adding Insurance to Your Risk Management Plan

Incorporating trade credit insurance into your overall risk management strategy can help strengthen your financial position. The policy outlines the responsibilities of both parties, such as covered risks, exclusions, claim timelines, and recourse for insured receivables.

Start by identifying your specific needs based on factors like the type of goods you sell, the political stability of buyer countries, and industry norms. For businesses with intricate supply chains, policies like Stock Throughput (STP) can provide coverage from the procurement of raw materials to final delivery. Meanwhile, Political Risk Insurance (PRI) can protect against losses caused by expropriation, political unrest, or currency-related issues.

To ensure seamless coverage, align your insurance policies with your supply contracts by using International Commercial Terms (Incoterms). This helps eliminate coverage gaps during the transfer of risk. Additionally, assess your suppliers’ reliability, quality control, and financial health through international business reports. Assign a team member to handle limit requests, monitor overdue accounts, and ensure compliance with stop-shipment rules. By combining these strategies with expert guidance, your risk management efforts can become even more effective.

Partnering with Brokers and Insurance Providers

Collaborating with experienced brokers can simplify compliance and ensure your insurance aligns with trade financing requirements. Expert brokers understand the complexities of regulatory standards and can help you secure tailored coverage. For U.S. importers, for example, compliance with Federal Motor Vehicle Safety Standards (FMVSS) and Environmental Protection Agency (EPA) emissions regulations is critical before shipping vehicles.

Customs brokers assist with mandatory filings, such as DOT Form HS-7 and EPA Form 3520-1, at the time of entry. They also help secure necessary bonds. For example, importers of nonconforming vehicles must post a DOT bond worth 1.5 times the vehicle’s dutiable value, in addition to the standard CBP entry bond.

Specialized brokers can also create layered programs or provide additional coverage for major accounts, often at a minimal cost. To ensure your coverage meets federal compliance standards and trade financing needs, work with brokers registered with recognized authorities. Their expertise can streamline the entire process, making it easier to manage compliance and secure the right insurance.

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

Conclusion: Managing Import Insurance Requirements

Effective risk management in importing starts with adhering to core insurance rules and ensuring your coverage is well-rounded. These steps not only shield your business from financial risks but also open doors for growth.

Consider this: U.S. bankruptcies are hitting record highs, and the trade credit insurance market is on track to reach $13.3 billion by 2025. Trade credit insurance, for instance, can help importers recover up to 90% of an invoice’s value if a buyer fails to pay. Plus, having insured receivables can lower your cost of capital by 25 to 75 basis points. These numbers highlight the importance of staying compliant with import regulations to safeguard your operations.

Meeting U.S. Customs and Border Protection (CBP) standards is non-negotiable. Properly classifying goods under the HTS, marking their origin, and valuing them correctly are all essential. Non-compliance could lead to penalties exceeding $1,000 or even the loss of your goods. It’s also crucial to keep an eye on the Office of Foreign Assets Control (OFAC) list, as importing from sanctioned nations may result in legal consequences or loss of insurance coverage.

To minimize risks, diversify your insurance portfolio. A combination of Marine Cargo, Trade Credit, and Political Risk insurance offers well-rounded protection. Additionally, adjusting insured values to reflect tariff increases ensures you’re not caught underinsured when you need coverage the most. This layered approach strengthens your risk management and keeps your business on stable footing.

FAQs

Do I need trade credit insurance if I already use Letters of Credit?

Letters of Credit (LCs) offer upfront payment security by ensuring specific conditions are fulfilled before funds are released. On the other hand, trade credit insurance steps in to protect businesses from non-payment risks, covering up to 95% of unpaid invoices if a buyer defaults. When used together, these tools can work seamlessly: LCs focus on securing individual transactions, while trade credit insurance addresses broader, ongoing risks like buyer insolvency or unforeseen political disruptions. This combination strengthens your risk management approach and provides a solid foundation for business expansion.

What can cause an import insurance claim to be denied?

When it comes to import insurance claims, there are several reasons they might be denied. These include disputed invoices, failing to meet reporting deadlines, not adhering to policy terms, or providing incomplete or incorrect documentation. Some of the most frequent challenges involve:

- Invoicing that falls outside the approved payment terms.

- Filing the claim after the deadline has passed.

- Disputes between buyers and sellers over transactions.

- Specific exclusions outlined in the insurance coverage.

To reduce the risk of having a claim denied, it’s crucial to meet all outlined requirements and ensure your documentation is complete and accurate. Attention to these details can save you time and prevent unnecessary complications.

How does insured receivables coverage increase my borrowing base?

Insured receivables coverage strengthens your borrowing base by increasing the reliability of your receivables as collateral. This added security encourages lenders to include more invoices in the borrowing base and provide higher advance rates. The result? Broader financing opportunities and better access to the working capital your business needs.