When it comes to trade credit claims, timing is everything. Missing the notification deadlines outlined in your insurance policy can lead to denied claims, leaving you to bear the financial loss. Here’s what you need to know:

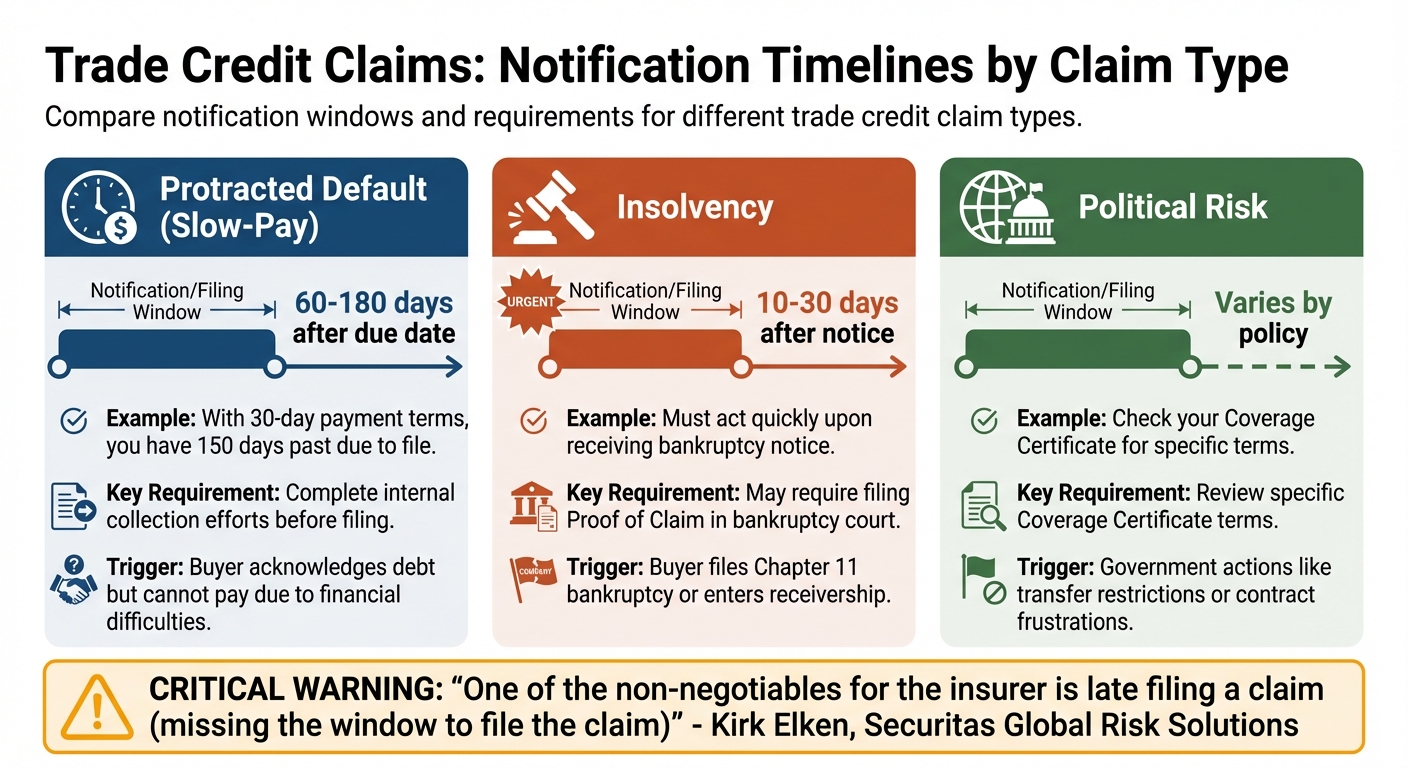

- Deadlines are strict: Most policies require overdue accounts to be reported within 30–90 days of the payment due date. Insolvency claims often have even shorter timelines (10–30 days).

- Act fast: Early notification allows insurers to investigate and mitigate losses through collection efforts or repayment plans.

- Know your policy: Different claims (e.g., protracted default vs. insolvency) have specific reporting windows. Always review your policy for details.

- Documentation matters: Ensure all required paperwork (invoices, proof of delivery, contracts, etc.) is accurate and submitted on time.

Failing to meet these requirements could result in losing coverage, even if you’ve paid your premiums. Stay ahead by tracking deadlines, notifying your insurer promptly, and keeping thorough records.

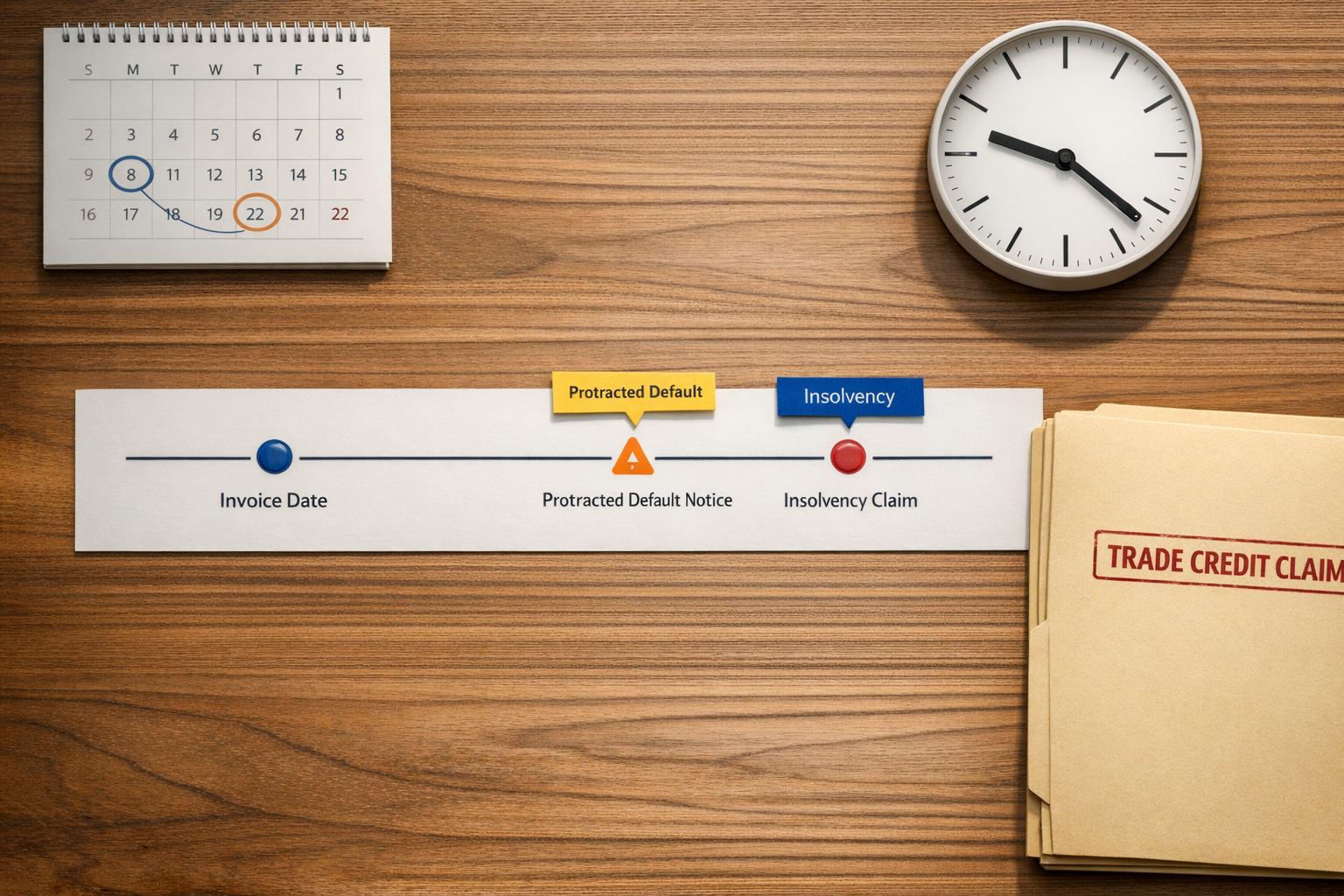

Timeline Basics and Key Terms

Trade Credit Claims Notification Timelines by Claim Type

What Notification Timelines Mean

Notification timelines refer to specific timeframes outlined in your policy, during which you need to report a buyer’s non-payment or formally file a claim. These deadlines are strict and are triggered by particular events, like when an invoice becomes overdue or if a buyer declares bankruptcy.

Most policies include a waiting period before you can file a claim. For instance, you might have to wait anywhere from 60 to 180 days after a payment is overdue before your insurer processes the claim. However, there’s also a maximum filing deadline you must meet. For example, under certain EXIM multi-buyer policies, you need to submit proof of loss within 240 days of the invoice becoming overdue. Missing this deadline could result in your claim being denied.

If your debtor is making partial payments or adhering to a payment plan, you may request an extension for the filing window. But this request must be made before the original deadline expires. Kirk Elken, Co-founder of Securitas Global Risk Solutions, emphasizes:

"One of the non-negotiables for the insurer is late filing a claim (missing the window to file the claim)".

Knowing these deadlines is crucial, as different claim types come with varying notification timelines.

How Policy Types Affect Notification

The type of claim you’re filing determines your timeline. For a protracted default (also called slow-pay), the buyer acknowledges the debt but cannot pay due to financial difficulties, such as declining sales, loss of customers, or fraud. In these cases, you typically have up to 180 days from the invoice date to file. If your payment terms were 30 days, this leaves you with 150 days past due to submit your claim.

Insolvency claims follow a different timeline. When a buyer files for Chapter 11 bankruptcy or enters receivership, you must act quickly – usually within 10 to 30 days of receiving notice. These shorter timeframes exist because the insurer may need to file a Proof of Claim with the bankruptcy court on your behalf. For political risk claims, which are triggered by government actions like transfer restrictions or contract frustrations, timelines vary depending on your policy. Always consult your Coverage Certificate for details.

| Trigger Event | Notification/Filing Window | Key Requirement |

|---|---|---|

| Protracted Default | 60–180 days after due date | Complete internal collection efforts |

| Insolvency | 10–30 days after notice | May require filing a Proof of Claim in court |

| Political Risk | Varies by policy | Review specific Coverage Certificate terms |

It’s essential to review the "Claims and Overdue" section of your Coverage Certificate to understand the specific waiting periods and deadlines for your policy. These details differ among insurers and policy types, so assuming timelines are universal could lead to costly mistakes.

sbb-itb-b840488

How to Notify Insurers of Trade Credit Claims

Step 1: Identify the Trigger Event

Start by identifying the event that requires you to notify your insurer. A protracted default happens when a buyer acknowledges their debt but struggles to pay – this could be due to issues like declining sales or losing key customers. On the other hand, insolvency occurs when a buyer files for Chapter 11 bankruptcy or goes into receivership.

These scenarios have different timelines. For protracted defaults, you usually have up to 180 days from the invoice date to file a claim. For example, with standard 30-day payment terms, this means about 150 days after the invoice becomes overdue. Insolvency claims, however, generally need to be reported within 10 to 20 days of receiving notice of the filing. This shorter timeframe allows the insurer to file a Proof of Claim with the bankruptcy court on your behalf.

Once you’ve confirmed the trigger event, make sure to report it to your insurer without delay.

Step 2: Complete Initial Reporting

Most policies include a Maximum Extension Period (MEP) – the deadline for notifying your insurer about an overdue account before it can be turned into a formal claim. To calculate this, add the MEP to the invoice’s due date. For instance, if the invoice is due on March 31, 2026, and the MEP is 45 days, you must notify your insurer by May 15, 2026.

For accounts exceeding $100,000, reporting may be required once they are 60 days past due. If a debtor is on a payment plan, request an extension to file within the original claim window. This ensures you retain your right to file if the plan falls through. Additionally, any repayment schedules you negotiate with a delinquent customer must be approved by your insurer. As Heather Smart Johnson from CreditInsurance.com cautions:

"If the payment plan was not approved by the insurance company, your claim may be denied".

Once the initial report is submitted, gather the necessary documentation to file your Proof of Loss promptly.

Step 3: File Proof of Loss

Prepare and submit the Proof of Loss package within the required deadline, ensuring all documents are accurate and consistent. Typically, you’ll need to include:

- Signed contracts or purchase orders

- Unpaid invoices

- Bills of lading (BOL) or proof of delivery (POD)

- A current statement of account

- Records of your internal collection efforts

It’s crucial to file against the correct legal entity. Listing the parent company instead of the specific subsidiary responsible for the debt can result in claim denial. For insolvency claims, include the insolvency practitioner’s letter, a completed Proof of Debt form, and confirmation of your creditor ranking. If you’re filing under discretionary coverage, a current 12-month credit report may also be required.

Insurers often begin reviewing claims within 24 hours of receiving the complete package. Make sure every document is in order to avoid delays or complications.

Common Problems and How to Prevent Them

Missing Deadlines

Missing deadlines is one of the most common reasons claims get rejected. Businesses often delay recognizing a loss or misunderstand the events that trigger their policies. On top of that, focusing on debt collection efforts can sometimes cause companies to miss the critical filing window.

And the consequences? They’re no joke. Credit Guarantee highlights:

"Late claims impact the Trade Credit Insurer’s ability to claim expended funds, thus undermining its ability to continue to serve its clients".

To avoid these pitfalls, implement automated tracking systems to monitor aging reports. Set up alerts to flag overdue accounts as they near important deadlines. For prolonged defaults, keep an eye on deadlines between 150 to 180 days after an invoice becomes overdue. For insolvency-related claims, you might only have 10 to 20 days from the date you’re notified of the filing. If partial payments cause delays, request an extension within the original filing window. Staying on top of deadlines and ensuring error-free documentation are your best defenses against losing out on recoverable funds.

While meeting deadlines is crucial, ensuring your documentation is accurate is just as important.

Errors in Documentation

Even if you meet every deadline, submitting inaccurate or incomplete documentation can still derail your claim. Documents like purchase orders, invoices, and bills of lading (or proof of delivery) need to align perfectly to validate the debt. Any discrepancies can lead to processing delays or outright rejections.

For example, back in December 2005, Mizuho Securities Co. faced a documentation error that had catastrophic results. A trader accidentally entered an incorrect order quantity, leading to a loss of roughly $340 million in just one day.

To minimize these risks, maintain a centralized database for customer and product information. Use automated tools to populate forms and reduce human error. Before submitting a claim, double-check every detail against the original purchase order and confirm that the payment terms align with your policy. Kevin Dorse, EVP at Amwins Brokerage, emphasizes the importance of submitting initial loss notices with the help of an agent whenever possible. This ensures accurate policy identification and proper presentation of information.

Conclusion

Your claim notification process plays a crucial role in protecting your coverage. Adhering to your policy’s notification timelines is key to shielding your business from financial losses. As Kirk Elken, Co-founder of Securitas Global Risk Solutions, warns:

"One of the non-negotiables for the insurer is late filing a claim (missing the window to file the claim)".

Failing to meet this critical deadline could allow your insurer to deny liability, leaving you to bear the full financial burden.

To ensure your claims are handled smoothly, follow these steps:

- Identify the trigger event, such as insolvency or protracted default.

- Report claims promptly, sticking to the timeframes outlined in your policy. For instance, many policies require reporting accounts that are 60 days past due, especially for high-value receivables exceeding $100,000.

- Keep thorough documentation of purchase orders, invoices, and shipping records to support your claim.

Timely notification isn’t just about compliance; it enables your insurer to act quickly. In fact, early notification allows insurers to begin recovery efforts within 24 hours. This swift action is essential, as trade credit insurance typically covers 75% to 95% of outstanding debt, helping protect your cash flow and working capital.

Additionally, take proactive steps like requesting and documenting payment plan extensions within the original filing window. Always secure written approval for revised payment schedules, file claims against the correct legal entity, and address disputes quickly to avoid delays.

FAQs

What is the trigger event for reporting a claim?

When a claim needs to be reported, it’s typically due to non-payment resulting from either customer insolvency or a prolonged default. To stay within the guidelines of your policy, you’ll need to report this within the timeframe specified – often up to 180 days from the invoice date. Be sure to carefully review your policy terms to ensure you meet all reporting requirements.

How do I calculate my policy’s notification deadline for an overdue invoice?

To figure out your notification deadline, take a close look at your trade credit insurance policy. Many policies give you up to 180 days from the invoice date to notify the insurer, but this isn’t always the case. Check your Coverage Certificate or the terms of your policy to pinpoint the exact timeline. Following the notice requirements carefully is crucial to avoid any risk of having your claim denied.

What mistakes can cause a claim to be denied even if I report on time?

Reporting your claim on time is important, but it doesn’t automatically mean it will be approved. There are several common reasons why claims might be denied, such as:

- Disputed invoices: If there’s a disagreement over the invoice, it could lead to a denial.

- Missing deadlines: Claims reported after the allowed timeframe may not be considered.

- Ignoring past-due reporting rules: Failing to follow these rules can jeopardize your claim.

- Shipping to past-due buyers: Continuing to send goods to buyers who are already overdue on payments can result in issues.

- Invoicing outside approved terms: If invoices don’t align with the agreed-upon payment terms, this could also lead to denial.

To avoid these pitfalls, make sure to carefully follow all policy requirements and guidelines.