Undiversified credit portfolios face significant risks that can jeopardize financial stability. These risks arise from over-concentration in specific borrowers, industries, or regions, making portfolios vulnerable to defaults and economic downturns. Key issues include:

- Concentration Risk: Heavy reliance on single borrowers or sectors amplifies the impact of defaults.

- Sector and Geographic Vulnerability: Focused exposure to specific industries or regions increases susceptibility to localized downturns.

- Systematic Risks: Undiversified portfolios are more exposed to macroeconomic shocks, such as interest rate hikes or financial crises.

- Higher Capital Requirements: Regulatory guidelines demand larger capital buffers for concentrated portfolios, straining resources.

To mitigate these risks, diversification across borrowers, industries, and regions is critical. Additionally, credit insurance can provide a safety net by transferring the risk of defaults to insurers. Combining these strategies ensures better financial stability and reduces potential losses.

Concentration risk & diversification for credit portfolio: Herfindahl-Hirschman Index HHI & Basel

sbb-itb-b840488

Main Risks of Undiversified Credit Portfolios

Undiversified credit portfolios carry interconnected risks that can escalate quickly, potentially threatening an institution’s financial health. Below, we break down these risks to illustrate how a lack of diversification can undermine stability.

Concentration Risk from Single Counterparties

Relying heavily on a small group of customers or accounts creates name concentration risk. This lack of diversification means a single default could result in catastrophic losses.

"Historical experience shows that concentration of credit risk in asset portfolios has been one of the major causes of bank distress."

– Basel Committee on Banking Supervision

Sector and Geographic Concentration

When credit exposure is concentrated in specific industries or regions, you face segment concentration. This type of clustering increases vulnerability to sector-specific downturns, regional economic slumps, or regulatory changes.

The collapse of Silicon Valley Bank in March 2023 is a stark example. Nearly half of the 130,000 venture-backed startups in the U.S. banked with SVB, creating a significant concentration within the tech startup ecosystem. Rising interest rates devalued SVB’s bond portfolio while also straining its tech-focused customer base. This dual pressure led to a downward spiral; by September 2022, the bank’s $15.9 billion in mark-to-market losses had wiped out its $11.8 billion in tangible common equity.

Similarly, Lehman Brothers‘ 2008 bankruptcy stemmed from an overexposure to mortgage-backed securities filled with subprime loans. When the U.S. housing market collapsed, the firm had no diversified assets to cushion the blow.

"When institutions fail to diversify their exposure across various sectors or regions, they expose themselves to heightened vulnerability."

– Risk management experts

Beyond sector-specific risks, undiversified portfolios are also more susceptible to large-scale economic disruptions.

Greater Exposure to Systematic Risks

Portfolios lacking diversification are especially vulnerable to macroeconomic shocks like interest rate hikes, global financial crises, or pandemics. These events can trigger simultaneous defaults across assets, amplifying losses.

A striking example is the 2021 collapse of Archegos Capital Management. Bill Hwang’s firm lost $20 billion in just two days due to concentrated, leveraged positions in a handful of stocks like ViacomCBS and Discovery. When these stocks declined simultaneously, Archegos faced margin calls it couldn’t meet, leading to massive liquidations that impacted global banks.

"The financial graveyard of history is filled with concentrated investors."

– Nick Maggiulli, COO of Ritholtz Wealth Management

Systematic risks are further compounded by firm-specific vulnerabilities.

Company-Specific Risk Exposure

Undiversified portfolios are also exposed to idiosyncratic risk – unexpected events tied to individual companies. These risks include management failures, fraud, product recalls, or competitive disruptions. Unlike systematic risks, these are isolated incidents that can still devastate concentrated holdings.

For example, in 2021, the Russell 3000 index showed significant performance variability. While the median stock delivered a +23% return, one in four stocks failed to grow, with returns flatlining at 0%. Without diversification to balance these outcomes, portfolios are left exposed to unpredictable losses unrelated to broader market trends.

Higher Capital Requirements and Profit Pressures

Undiversified portfolios demand significantly higher Economic Capital (EC) to guard against unexpected losses. EC calculations consider factors like default probabilities, loss severity, and exposure correlations, all of which intensify with concentration. Regulators enforce strict capital requirements to mitigate these risks.

Under Basel III, credit exposures are capped at 25% of an institution’s Tier 1 capital, with connected counterparties limited to 15%. Concentrations exceeding 100% of net worth are flagged as high-risk and require rigorous oversight.

Excessive concentration often forces financial institutions to maintain unsustainable capital buffers. During the 2008–2009 crisis, Bank of America faced severe strain due to its mortgage market concentration, necessitating a $45 billion government bailout to restore capital adequacy.

These capital pressures also lead to higher operational costs, requiring advanced risk management systems, frequent stress tests, and more extensive due diligence. Such costs are a direct consequence of undiversified credit portfolios and will be addressed in the next section.

| Risk Factor | Financial Consequence | Impact on Business |

|---|---|---|

| Single Counterparty Concentration | Higher Economic Capital (EC) | Reduces funds available for other investments |

| Sector/Geographic Clustering | Earnings Deterioration | Increases risk of insolvency during economic downturns |

| Regulatory Non-compliance | Capital Surcharges | Raises operational costs and lowers return on equity |

| High Asset Correlation | Deep Drawdowns | Slows recovery and demands more capital for stabilization |

Solutions to Reduce Risks in Undiversified Credit Portfolios

Concentration risk can be tackled effectively with well-thought-out measures. By taking deliberate steps, financial institutions and businesses can spread exposure and avoid devastating losses. Two main approaches stand out in managing this risk:

Applying Diversification Strategies

One of the most straightforward ways to address concentration risk is by diversifying your credit exposure. This means spreading your portfolio across various counterparties, industries, and regions, ensuring that no single event or default can severely impact your overall position.

Name diversification involves breaking down large, single-name exposures into smaller, more manageable allocations. For instance, instead of lending $10 million to one client, you could distribute the amount among several borrowers, each with a distinct risk profile. This minimizes the fallout from any single default.

Sectoral and industry diversification helps protect against downturns in specific industries. By distributing credit across sectors like technology, healthcare, manufacturing, and consumer goods, you can balance the risk. If one sector faces challenges, others may remain stable or even perform well, helping to buffer your portfolio.

Geographic diversification spreads loans across different regions, reducing risks tied to localized economic slumps, natural disasters, or regional regulations. For example, a portfolio concentrated in a single tech hub might face unique risks compared to one distributed across multiple regions.

In addition, incorporating a mix of asset classes – such as consumer debt, commercial loans, and government bonds – can help reduce market correlation and provide more stability.

But diversification requires discipline. To effectively manage risks, it’s crucial to set limits on exposure, conduct regular stress tests, and maintain strict position sizing.

"Excessive concentrations of credit have been key factors in banking crises and failures."

– Office of the Comptroller of the Currency (OCC)

The benefits of diversification are clear. Managing concentration risk effectively can result in capital relief of up to 21%, freeing up resources to support growth while maintaining a stable foundation.

While diversification spreads risk, credit insurance offers a way to transfer it.

Using Credit Insurance for Risk Protection

Diversification helps restructure risk, but credit insurance provides an extra layer of security by transferring the risk of non-payment to an insurer. This approach is particularly useful when a few large customers account for a significant portion of your revenue.

Credit insurance typically covers up to 90% of losses caused by bankruptcy, prolonged default, or political risks. For businesses exposed to high concentration risk, targeted coverage can protect against defaults from specific large clients.

Insurers also offer access to global databases and regional expertise to assess buyers and avoid high-risk counterparties. For portfolios concentrated in specific regions, credit insurance can shield against non-payment risks stemming from war, terrorism, currency instability, or trade law changes.

"Credit insurance policies can serve as high-quality collateral for banks. Banks view these policies as a tool for reducing credit risk… these benefits can be passed back to the multinational organization as improved financing terms."

– WTW

For example, in August 2024, an energy company faced strict concentration limits in its bankruptcy-remote Special Purpose Vehicle, which initially excluded its four largest international clients. By collaborating with Marsh‘s trade credit specialists to secure credit insurance, the company adjusted its limits to include these receivables, raising an additional $60 million.

Credit insurance premiums usually range from 0.1% to 0.4% of the invoice value. These costs are often far outweighed by the protection they provide against potential losses. Factors like industry type, annual turnover, bad debt history, and customer creditworthiness can influence premium rates.

Platforms like CreditInsurance.com provide resources to help businesses understand and implement credit insurance strategies. These tools clarify how insured receivables can improve financing terms and expand credit lines while protecting against risks like non-payment and customer insolvency.

When adopting credit insurance, it’s wise to segment your accounts receivable based on risk levels rather than applying blanket coverage. Focus on safeguarding high-value or high-risk accounts, and for critical buyers, opt for non-cancellable credit limits to ensure uninterrupted protection. Additionally, using credit insurance policies as collateral can help negotiate better financing terms and larger credit limits.

| Diversification/Protection Type | Focus Area | Risk Mitigated |

|---|---|---|

| Name | Individual Obligors | Firm-specific shocks |

| Sectoral | Industries (e.g., Energy) | Industry-specific downturns |

| Geographic | Regions, Cities, Countries | Local economic or political instability |

| Asset Class | Corporate, Consumer, Sovereign | High market correlation |

| Credit Insurance | High-value Counterparties | Non-payment, insolvency, political risks |

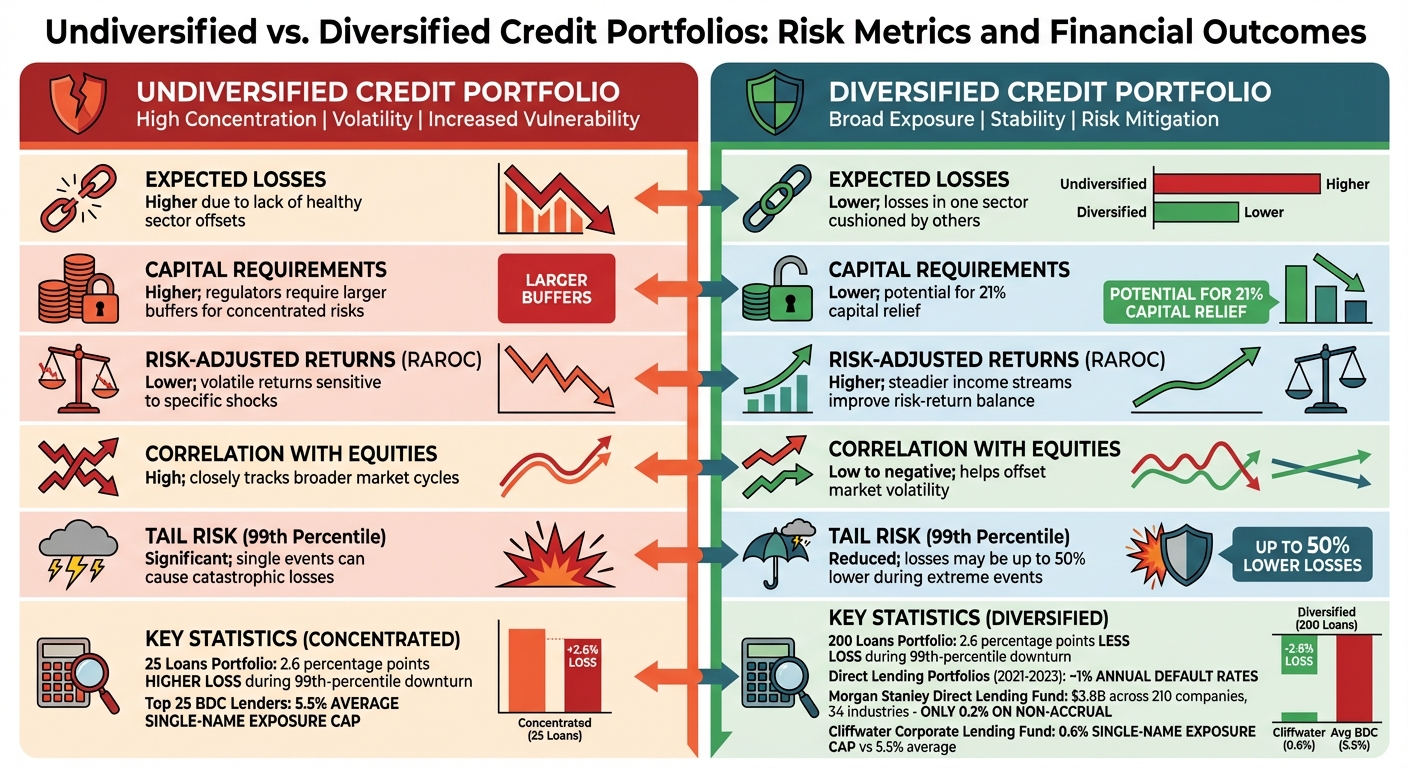

Comparison: Undiversified vs. Diversified Portfolios

Undiversified vs Diversified Credit Portfolios: Risk Metrics Comparison

Risk Metrics and Financial Outcomes Comparison

The contrast between undiversified and diversified credit portfolios becomes clear when examining key financial metrics. Concentrating credit exposure leaves investors vulnerable to isolated risks, while spreading exposure across multiple loans creates a cushion against unexpected economic shocks.

Take this example: a diversified portfolio containing 200 loans experienced 2.6 percentage points less loss during a 99th-percentile economic downturn compared to a concentrated portfolio with only 25 loans. That 2.6 percentage-point difference could mean the line between financial stability and insolvency. Let’s dive into some real-world examples to see these principles in action.

The Morgan Stanley Direct Lending Fund illustrates how diversification pays off. By Q1 2025, it had allocated $3.8 billion across 210 companies in 34 industries, with only two loans on non-accrual – just 0.2% of the portfolio’s total cost. Now compare that to the Blackstone Secured Lending Fund, which in August 2025 held a single, significant position: a loan to Medallia Inc. This loan accounted for 5.37% of net assets and was marked down to 87 cents on the dollar, resulting in a $42 million hit to the fund’s value.

As Larry Swedroe, an investment consultant and author, explains:

"In credit investing, it’s not about hitting home runs – it’s about consistently getting on base while avoiding strikeouts."

– Larry Swedroe

The takeaway? Diversified portfolios achieve more stable performance compared to their undiversified counterparts.

| Metric | Undiversified Portfolio | Diversified Portfolio |

|---|---|---|

| Expected Losses | Higher due to lack of healthy sector offsets | Lower; losses in one sector are cushioned by others |

| Capital Requirements | Higher; regulators require larger buffers for concentrated risks | Lower; potential for 21% capital relief |

| Risk-Adjusted Returns (RAROC) | Lower; volatile returns sensitive to specific shocks | Higher; steadier income streams improve the risk-return balance |

| Correlation with Equities | High; closely tracks broader market cycles | Low to negative; helps offset market volatility |

| Tail Risk (99th Percentile) | Significant; single events can cause catastrophic losses | Reduced; losses may be up to 50% lower during extreme events |

Between 2021 and 2023, diversified direct lending portfolios maintained trailing default rates around 1% annually – far below the rates seen in public high-yield debt. For instance, the Cliffwater Corporate Lending Fund (CCLFX) caps single-name exposure at 0.6% – a stark contrast to the 5.5% average concentration found in the largest 25 Business Development Company lenders. These figures emphasize how diversification and credit insurance serve as essential tools for managing portfolio risk effectively.

Conclusion: Why Diversification and Credit Insurance Matter

Relying on undiversified credit portfolios can expose businesses to serious risks, including concentration issues, sector-specific shocks, and broader economic downturns. History has shown that concentrated credit risk is a key factor in financial distress for banks. For example, the collapse of Silicon Valley Bank highlights how concentrated positions can destabilize financial institutions. Its $15.9 billion in mark-to-market losses completely wiped out its $11.8 billion equity base, underscoring the dangers of inadequate risk management.

Diversification plays a critical role in addressing these challenges. By spreading exposure across various sectors and regions, businesses can reduce the impact of localized economic disruptions. It also helps free up capital, allowing businesses to focus on growth instead of holding excessive reserves. However, diversification on its own may not fully shield businesses from every potential risk.

This is where credit insurance becomes a valuable tool. It acts as a safety net by transferring the risk of customer defaults to insurers. With this added layer of protection, businesses can confidently extend higher credit limits and explore new markets without fear of non-payment.

For a balanced and secure approach, businesses should combine diversification strategies with credit insurance. Platforms like CreditInsurance.com (https://creditinsurance.com) provide resources to help companies understand how credit insurance safeguards against non-payment, customer insolvency, and even political risks. This dual strategy not only reduces risks but also supports steady and sustainable growth.

FAQs

How do I know if my credit portfolio is too concentrated?

Your credit portfolio might carry more risk than you realize if a significant chunk of it is tied to just a handful of clients, industries, or geographic areas. To get a clear picture, pinpoint where risks are concentrated and think about how potential stress in those areas could affect your overall financial health. The solution? Diversification. Spreading out your exposure can help safeguard your portfolio and minimize the chances of major financial setbacks.

What diversification limits should I set for borrowers, industries, and regions?

To tackle credit concentration risks, it’s crucial to establish clear diversification limits. For borrowers, try not to let more than 10% of your revenue come from a single customer, and keep the combined revenue from your five largest customers under 25%. When it comes to industries and regions, aim to limit exposure to any one sector or area to 10-20%. Regularly assess these thresholds, perform stress tests, and make adjustments as needed to stay in line with your company’s overall risk management approach.

When does credit insurance make more sense than diversifying?

Credit insurance becomes especially useful when diversifying a credit portfolio isn’t enough to fully manage risk. For businesses that depend heavily on a small group of customers, specific industries, or particular regions, this type of insurance can help cushion the blow of defaults or economic downturns. It also makes stepping into new markets or working with unfamiliar clients less risky, offering a layer of security when diversification efforts fall short.