When businesses operate internationally, trade sanctions can complicate dispute resolution by disrupting contracts and legal processes. Sanctions, such as asset freezes, trade bans, or service restrictions, can block access to funds, legal representation, or arbitration processes. This creates three major challenges for businesses:

- Unclear enforcement: Different countries enforce sanctions inconsistently, leading to confusion and delays in resolving disputes.

- Conflicting rules: Cross-border disputes are complicated by jurisdictions with opposing sanctions policies.

- Evasion risks: Attempts to bypass sanctions can result in contract invalidation or severe penalties.

To manage these risks, businesses should focus on three key strategies:

- Compliance programs: Conduct regular screenings of partners and supply chains to avoid violations.

- Sanctions clauses in contracts: Clearly define sanctions-related terms and remedies for disruptions.

- Trade credit insurance: Protect against financial losses caused by frozen assets or payment blockages.

Sanctions and trade controls – what you need to know

sbb-itb-b840488

Main Risks Sanctions Create for Dispute Resolution

When sanctions intersect with dispute resolution, businesses face three major challenges that can upend even the best-laid legal plans. These challenges stem from inconsistent enforcement, conflicting cross-border regulations, and complications arising from evasion attempts. Together, they create a web of legal hurdles that can escalate disputes and increase costs across jurisdictions.

Unclear Sanctions Enforcement

Sanctions enforcement is anything but uniform, often leaving businesses caught in a "sanctions whipsaw". For instance, a company might comply with U.S. sanctions only to find itself penalized in Europe – or vice versa. The U.S. tends to act swiftly with broad sanctions, while the European Union prefers phased implementation. This disparity creates uncertainty, especially when a counterparty is sanctioned in one jurisdiction but not another.

The complexity grows with the sheer number of U.S. sanctions programs – currently 37 – each with its own rules. Licensing delays add another layer of difficulty. Even when businesses secure licenses, getting approval to pay legal fees or arbitration costs can take months, undermining their ability to mount an effective defense. In the U.K., for example, a General License limits arbitral fee payments for Russian-designated entities to $500,000 per arbitration. Exceeding this cap requires a specific license, which can further delay proceedings.

"The trend is not toward harmonization; it is toward fragmentation. More regulators, more lists, more politics, and more companies caught in the middle." – Morgan McDaniel, The Wallenstein Law Group

Such fragmented frameworks across nations only add to the uncertainty.

Different Sanctions Rules Across Countries

Cross-border disputes become even more complicated when jurisdictions enforce conflicting sanctions policies. For example, the European Union’s blocking statute prohibits European companies from complying with specific U.S. extraterritorial sanctions, creating a regulatory deadlock where adhering to one jurisdiction’s rules means violating another’s.

Russia’s Federal Law No. 171-FZ highlights this issue. In December 2021, the Russian Supreme Court ruled in JSC Uraltransmash v. PESA that foreign sanctions against a Russian party justified moving disputes from international arbitration to Russian courts, even when a valid arbitration agreement existed. The court deemed the sanctions an "obstacle to justice."

Adding to the confusion, courts interpret the "public policy" exception differently across jurisdictions. For instance, French courts reject unilateral U.S. sanctions as incompatible with French international public policy, while they defer to sanctions issued by the UN or EU. Similarly, in January 2025, the English High Court dismissed claims in LLC EuroChem v. Societe Generale SA under on-demand bonds, as payment in France or Italy would have breached EU sanctions – even though the contract was governed by English law.

Legal Problems from Sanctions Evasion

Evasion strategies, such as shadow trading or cryptocurrency transactions, introduce yet another layer of risk. While these tactics might seem like a workaround, they often lead to severe legal consequences, including contract invalidation and criminal charges. Violating U.K. sanctions, for example, can result in fines and up to seven years of imprisonment.

Evasion also complicates dispute resolution. Courts may use doctrines like frustration or supervening illegality to void contracts if fulfilling them requires an illegal act. A notable example is the April 2024 U.K. Supreme Court decision in RTI Ltd v. MUR Shipping BV. The court ruled that a "reasonable endeavors" obligation in a force majeure clause did not require a party to accept payment in Euros instead of U.S. dollars to bypass sanctions. This decision confirmed that parties cannot be forced to restructure agreements to sidestep sanctions, even if it seems technically possible.

The challenges don’t stop with contract enforcement. Under Article V(2)(b) of the New York Convention, courts may refuse to enforce an arbitral award if it violates the enforcing state’s public policy, which often includes sanctions compliance. Even when arbitration rulings favor a party, asset freezes or public policy considerations can render the awards unenforceable, leaving businesses unable to collect on their claims.

How to Reduce Sanctions-Related Risks

To navigate the challenges of fragmented enforcement and conflicting sanctions rules, businesses should take a three-pronged approach to minimize risks and safeguard their operations. This involves creating strong compliance programs, embedding precise contract provisions, and leveraging financial tools to manage political risks effectively.

Build Strong Sanctions Compliance Programs

A solid compliance program goes beyond just having a policy on paper. Start by appointing a dedicated compliance officer who can oversee regular screening of business partners, supply chains, and beneficial owners. The goal is to identify any connections to sanctioned jurisdictions or individuals early on. Keep thorough records of all due diligence activities – these can serve as crucial evidence of proactive compliance during audits or legal reviews. Additionally, provide targeted training for teams in trade, procurement, and finance to help them spot and address sanctions-related issues before they escalate.

This groundwork not only reduces risk but also ensures that your contracts are built on a solid compliance framework.

Add Sanctions Clauses to Contracts

Sanctions clauses have become an essential feature of international commercial agreements. As Reed Smith LLP explains, "The sanctions clause has become a ‘must have’ contractual clause". These clauses should clearly define the relevant jurisdictions – such as the U.S., UK, EU, and UN – and specify whether they cover only direct sanctions or also address secondary sanctions risks.

Precision is key. Clearly define what qualifies as a "sanctioned person", including entities owned or controlled by designated individuals. For example, in the 2023 Singapore Court of Appeal case, Kuvera Resources Pte Ltd v. JPMorgan Chase Bank, N.A., JP Morgan flagged a vessel as potentially Syrian-owned and refused payment under a letter of credit. The court ruled against the bank, noting it failed to objectively prove the vessel was subject to sanctions.

Contracts should also outline specific triggers and remedies for breaches tied to sanctions. Make sure these provisions are aligned with arbitration clauses, as some institutions, like the LCIA, hold licenses that allow them to facilitate payments from sanctioned entities.

While well-crafted contracts reduce legal risks, financial safeguards provide additional protection against the fallout from sanctions.

Use Trade Credit Insurance for Political Risk Coverage

Sanctions can disrupt access to critical payment systems like SWIFT, leaving even willing parties unable to fulfill their obligations. Trade credit insurance offers a safety net by covering losses due to payment failures or insolvencies caused by sanctions. This type of coverage is especially beneficial during sudden geopolitical shifts, which can leave businesses with frozen assets or funds they can’t access.

Beyond payment defaults, trade credit insurance also addresses broader political risks tied to sanctions. These include blocked assets, restrictions on payment systems, travel bans that prevent in-person participation in hearings, or IT service limitations that hinder the use of remote technologies during disputes. For more details on selecting the right coverage for your specific needs, resources like CreditInsurance.com can provide helpful guidance.

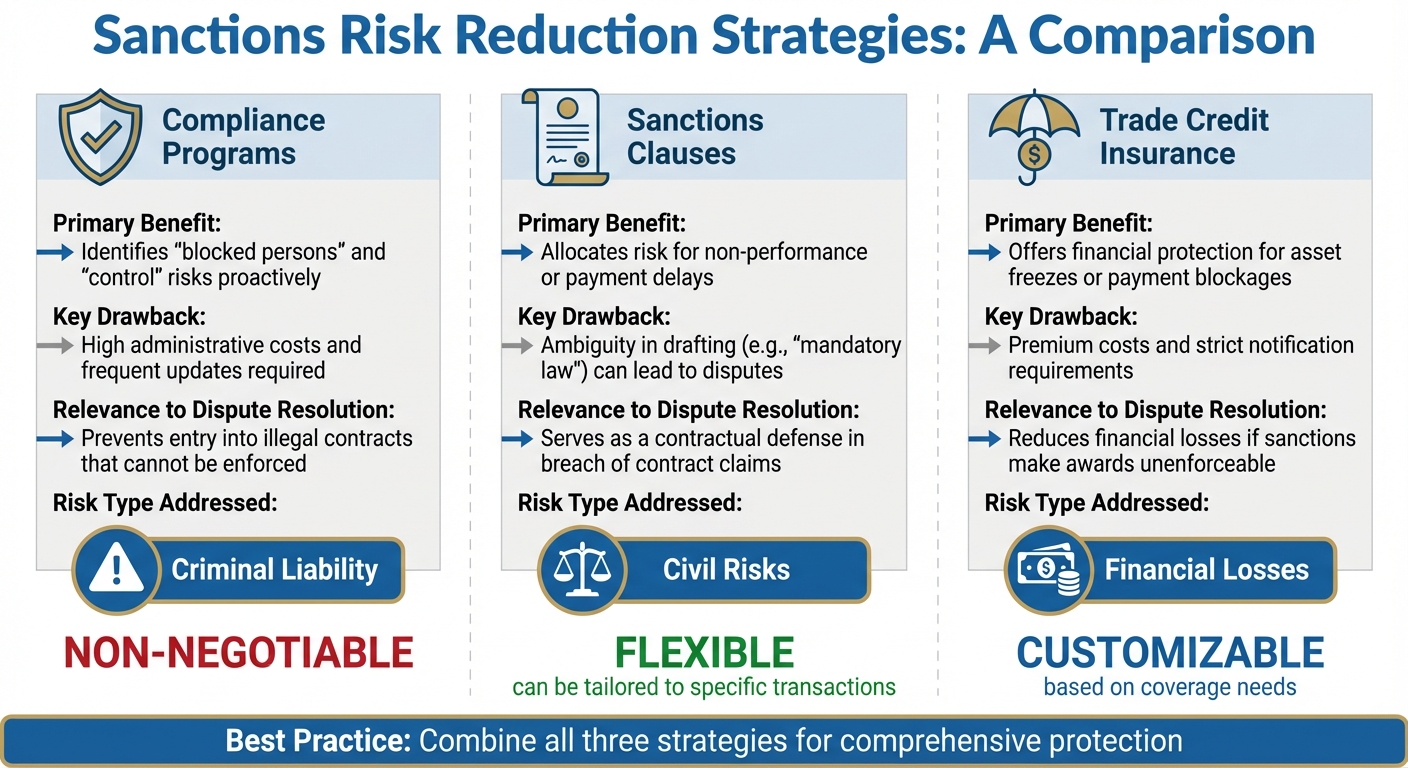

Comparing Risk Reduction Strategies

Three Strategies to Reduce Sanctions-Related Business Risks

Each risk reduction strategy tackles a specific type of risk: compliance programs help avoid criminal liability, sanctions clauses manage civil risks, and trade credit insurance protects against financial losses. Here’s how they work:

- Compliance programs focus on preventing criminal liability by thoroughly screening counterparties and beneficial owners before agreements are finalized.

- Sanctions clauses address civil risks by providing contractual remedies, such as the ability to suspend or terminate agreements when sanctions hinder performance.

- Trade credit insurance safeguards against financial losses caused by frozen payment systems or inaccessible assets due to political events.

While these strategies cover distinct risk areas, it’s important to note that civil law risks can be allocated through contracts, but criminal or administrative liabilities tied to sanctions breaches cannot be transferred. This makes compliance programs a non-negotiable requirement for regulatory adherence, whereas sanctions clauses are flexible and can be tailored to fit specific transactions.

Strategy Comparison Table

| Strategy | Primary Benefit | Key Drawback | Relevance to Dispute Resolution |

|---|---|---|---|

| Compliance Programs | Identifies "blocked persons" and "control" risks proactively. | High administrative costs and frequent updates required. | Prevents entry into illegal contracts that cannot be enforced. |

| Sanctions Clauses | Allocates risk for non-performance or payment delays. | Ambiguity in drafting (e.g., "mandatory law") can lead to disputes. | Serves as a contractual defense in breach of contract claims. |

| Trade Credit Insurance | Offers financial protection for asset freezes or payment blockages. | Premium costs and strict notification requirements. | Reduces financial losses if sanctions make awards unenforceable. |

Institutional arbitration can complement these strategies. For example, organizations like the LCIA have experience handling payment clearances and may hold general licenses for fees. This makes them more efficient than ad hoc proceedings, where individual arbitrators must secure their own licenses. Such administrative support minimizes the risk of payment issues disrupting the dispute resolution process.

The best approach often combines all three strategies: compliance programs to avoid violations, well-drafted sanctions clauses to manage commercial risks, and trade credit insurance to mitigate financial losses when sanctions disrupt payments. Together, these tools provide a comprehensive framework for protecting your business from sanctions-related challenges in dispute resolution.

Conclusion: Protecting Your Business from Sanctions Risks

Trade sanctions create three major challenges for businesses: criminal liability from accidental violations, civil risks due to disrupted operations, and financial losses from frozen assets. To illustrate the growing complexity, the UK’s Russia sanctions framework expanded from 64 pages in January 2022 to a staggering 529 pages by early 2025, with trade prohibitions multiplying fivefold. In the U.S., approximately 2,500 entries were added to the primary sanctions list in 2023 alone. Clearly, businesses can no longer afford to take a passive approach to sanctions risk.

As Reed Smith aptly pointed out, sanctions protections have shifted from being optional to absolutely essential. This shift means businesses must now treat sanctions risk management with the same seriousness as they do financial planning or cybersecurity.

To effectively navigate these risks, companies need a comprehensive strategy that integrates compliance programs, contractual safeguards, and financial protections. Each addresses a different aspect of risk, but none is sufficient on its own. Together, they form a robust defense: automated screening to flag risks early, carefully drafted contracts to manage disruptions, and political risk insurance to mitigate financial exposure. Below are actionable steps businesses can take to stay ahead.

Key Points for Businesses

To reduce sanctions risks, businesses must adopt proactive and dynamic measures. Regulatory updates occur daily, and staying compliant requires constant vigilance. For example, the EU now mandates that payment service providers verify customer sanctions status at least once per day, moving away from one-time checks. This makes real-time automated screening tools essential, along with meticulous documentation of compliance efforts.

Beyond compliance, contractual safeguards are vital. Businesses should update force majeure clauses to explicitly include sanctions as a triggering event. These clauses should clarify whether sanctions must "prevent" or simply "hinder" performance and outline remedies such as suspension or termination rights. Additionally, when choosing arbitration forums, opt for sanctions-neutral venues and institutions that hold general licenses for handling fees from sanctioned entities. For instance, the UK government allows payment of arbitral fees up to £500,000 per arbitration under its General License for Russian sanctions.

Financial protection is equally important. Sanctions can freeze payment systems or render assets inaccessible, leaving businesses vulnerable to significant losses. Political risk insurance can provide a financial safety net, ensuring cash flow is preserved even during geopolitical disruptions. Platforms like CreditInsurance.com offer resources to help businesses evaluate coverage options tailored to the unpredictable nature of international trade.

Finally, businesses must prepare for sanctions-triggered disputes by developing a board-approved crisis playbook. This playbook should outline clear responses to geopolitical events, including pre-approved templates for force majeure notices, alternative supply chain plans, backup financing options, and immediate legal hold procedures to preserve evidence across affiliates. As Duane Morris LLP advises:

Build a board-approved crisis and opportunity playbook that maps geopolitical triggers to defined responses.

FAQs

Can sanctions stop me from using arbitration?

Sanctions can throw a wrench into arbitration by interrupting proceedings, slowing down the enforcement of awards, or triggering contractual clauses such as force majeure. These complications can stall or even derail arbitration efforts. To navigate these challenges, businesses should proactively assess potential risks and consider strategies to minimize disruptions, ensuring dispute resolution stays on track.

What should a sanctions clause include?

A sanctions clause needs to clearly outline the scope of sanctions, detail the responsibilities of all parties involved, and specify the conditions under which obligations may be suspended or terminated. It should also provide enough flexibility to account for changing geopolitical situations. Using clear and precise language is crucial to prevent misunderstandings and ensure adherence to trade regulations.

How does trade credit insurance help if payments are frozen?

Trade credit insurance offers a safety net for businesses by providing financial protection when payments are halted due to sanctions. It helps companies manage cash flow by covering or minimizing losses from non-payment, ensuring they can stay steady even in tough times.