During recessions, businesses face increased risks of customer defaults. Retail and wholesale credit insurance offer protection, but they work differently:

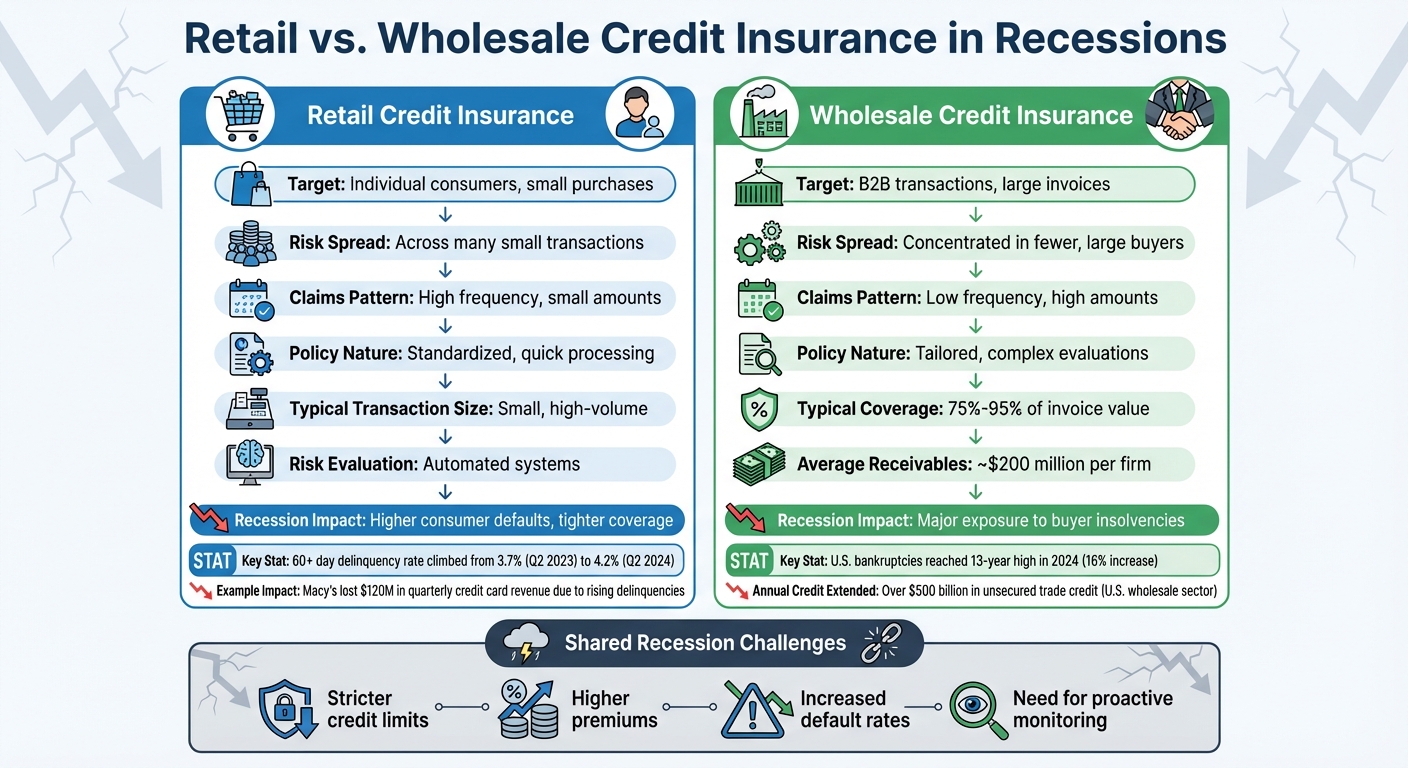

- Retail Credit Insurance: Covers individual consumer defaults (e.g., missed payments on financed purchases). It handles smaller, high-volume transactions and uses automated systems for risk evaluation.

- Wholesale Credit Insurance: Protects B2B sellers from large unpaid invoices. It’s tailored to specific industries and buyers, covering 75%-95% of invoice value.

Key differences:

- Retail deals with many small claims; wholesale faces fewer but larger claims.

- Wholesale risks are concentrated in fewer accounts, making defaults more impactful.

- Recessions lead to stricter credit limits and higher premiums for both types.

Quick Comparison

| Feature | Retail Credit Insurance | Wholesale Credit Insurance |

|---|---|---|

| Target | Individual consumers, small purchases | B2B transactions, large invoices |

| Risk Spread | Across many small transactions | Concentrated in fewer, large buyers |

| Claims | High frequency, small amounts | Low frequency, high amounts |

| Policy Nature | Standardized, quick processing | Tailored, complex evaluations |

| Recession Impact | Higher defaults, tighter coverage | Major exposure to buyer insolvencies |

Both types are vital for managing risks during economic downturns. Retailers should monitor consumer behavior, while wholesalers must track buyer creditworthiness and diversify risks.

Retail vs Wholesale Credit Insurance: Key Differences During Recessions

Recession Risks for Retail Credit Insurance

Higher Consumer Default Rates

During a recession, household budgets tighten, and spending priorities shift dramatically. This economic pressure often leads to payment challenges, especially in the retail sector. For example, the 60-plus day delinquency rate in retail climbed from 3.7% in Q2 2023 to 4.2% in Q2 2024. Meanwhile, over 56,000 businesses missed at least one financial trade payment in the same quarter – a 10.2% increase from the previous year. These trends directly impact retail credit insurance, as insurers face a surge in claims and respond by tightening coverage.

The financial strain is particularly severe in lower-income areas. By early 2025, the 90-day delinquency rate in the lowest-income 10% of ZIP codes hit 20.1%, nearly doubling from late 2022. Mark Cohen, Director of Retail Studies at Columbia Business School, summed it up:

"Delinquencies are a nasty and inevitable byproduct of a consumer economy that’s got a little superheated, that’s now cooling off. And now we’re looking at the hangover."

This reality forces credit insurers to rethink their risk models. For retailers, the fallout is tough – higher premiums and stricter underwriting come at a time when flexibility is desperately needed. The rising default rates also create ripple effects, as certain retail sectors face insolvency risks that compound these challenges.

Industry-Specific Insolvency Risks

Recessions don’t just affect individual defaults; they also amplify insolvency risks across specific retail sectors. Department stores and specialty retailers are especially vulnerable. Take Saks Global, for instance. In January 2026, the company filed for Chapter 11 bankruptcy following vendor issues, which led to the closure of its off-price division. This left high-end brands that depended on Saks facing uncertainty. Similarly, JOANN, a specialty craft retailer, declared bankruptcy in 2025, citing inventory shortages and ongoing retail struggles.

The trend of "second-time filers" highlights deeper structural issues. Forever 21’s U.S. operations filed for bankruptcy again in 2025, carrying $1.6 billion in debt. Under their restructuring plan, unsecured creditors – many of them retail suppliers – were projected to recover a mere 3% to 6% of their claims. Kirk Elken, Co-founder of Securitas Global Risk Solutions, explained:

"When those forces [price sensitivity, promotions, and leverage] overlap, the risk shifts from ‘slow pay’ to ‘sudden event.’"

For credit insurers, this means traditional warning signs, like gradual payment delays, may no longer provide enough time to act before a sudden default triggers a claim.

Private Label Credit Card Defaults

Private label credit cards, or store-branded cards, pose another significant risk during economic downturns. These cards are often the first payments consumers skip when financial stress mounts. Michael Ashley Schulman, Chief Investment Officer at Running Point Capital Advisors, noted:

"For stressed consumers, store cards are one of the first things they may be late or renege on before regular credit cards, car payments, and mortgages which they consider more important."

Serious delinquencies on credit cards (90+ days past due) jumped to 2.8% in Q1 2025 – a 52% increase from the previous year. This financial strain has immediate consequences for retailers. For example, Macy’s reported a $120 million drop in quarterly credit card revenue in August 2023 due to rising delinquencies, forcing an $80 million cut in its annual forecast. Macy’s credit cards carried a steep interest rate of 31.99% APR in August 2023, far above the national average of 22.39%. While these high rates attract riskier consumers, they also create a cycle where defaults spike during downturns, further weakening retailer finances and increasing the likelihood of credit insurance claims.

sbb-itb-b840488

Recession Risks for Wholesale Credit Insurance

Supply Chain Disruptions

Economic downturns can wreak havoc on supply chains, often setting off a domino effect of payment defaults. When one buyer within the wholesale network fails to pay, it can cascade through the system, turning what could have been a single issue into a larger, systemic problem.

Take the COVID-19 pandemic as an example – trade credit insurance rates in primary markets jumped by 20% to 30%, while rates in the excess market doubled. Recessions only make these challenges worse. Prolonged defaults become common as buyers struggle with cash-flow issues, delaying payments for extended periods. For wholesalers, this means filing claims in a tougher environment, where recovery rates are often lower due to unfavorable "workout" processes. These operational challenges quickly spill over into broader financial risks.

B2B Insolvencies and Payment Failures

The risks don’t stop at supply chains – wholesale insurers also face significant financial exposures. On average, a wholesale firm manages around $200 million in accounts receivable, and the U.S. wholesale sector extends over $500 billion in unsecured trade credit each year. Even a single default can hit the sector hard, given its typically slim profit margins.

Recent data paints a concerning picture. U.S. bankruptcies reached a 13-year high by mid-2024, showing a 16% increase from the previous year. On top of that, insurance payouts for bad debts rose by 23% in the first half of 2023. Warning signs often emerge before a buyer defaults – many max out their credit about a year beforehand. However, traditional indicators like payment delays may not give wholesalers enough time to act, leaving them with limited options to mitigate losses.

Mike Seff, Senior Vice President of Specialty Lines at Intact Insurance Specialty Solutions, summed up the current climate:

"The current environment of geopolitical conflict, policy volatility, inflationary pressure, supply chain fragmentation and shifting consumer dynamics has created a perfect storm of unpredictability."

Geopolitical and Market Instability

Geopolitical factors add another layer of complexity to the wholesale credit landscape during economic downturns. Tariffs, for example, can be imposed or increased, drastically changing the cost structure of cross-border trade. By early 2026, U.S. import tariffs had reached levels not seen since the 1930s.

Jerry Paulson, Senior Vice President at HUB International, highlighted the impact:

"If a company has to pay 15% to 20% more for raw materials [because of a tariff], the financial impact can be severe. Trade credit insurance helps solve this dilemma by covering the risk of unpaid invoices."

The economic backdrop doesn’t offer much relief, either. U.S. nonfinancial corporate debt climbed to $14.3 trillion by the first quarter of 2025 – a 25% increase compared to pre-pandemic levels. At the same time, global merchandise trade growth is expected to slow to just 0.9% in 2025, down from 2.9% in 2024. This mix of high debt and sluggish growth makes the wholesale sector particularly vulnerable.

Trade itself has become a tool in geopolitical conflicts, with sanctions, export controls, and discriminatory policies disrupting long-established supply chains. Insurers are responding by lowering credit limits for certain buyers or pulling out of high-risk sectors altogether. They’re factoring in external risks like tariffs, interest rates, and geopolitical tensions into their underwriting decisions. Wholesalers, in turn, may need to shift sourcing to countries with lower tariffs, which can place financial strain on their original suppliers.

Sarah Murrow, President and CEO of Allianz Trade Americas, put it this way:

"Trade credit insurance is vital to keeping liquidity in supply chains… It is the glue that keeps world trade going."

Despite its importance, trade credit insurance currently covers only about 15% of global trade. This leaves most wholesalers exposed to the growing risks brought on by economic, geopolitical, and market instability.

Retail vs. Wholesale Credit Insurance: Key Differences During Recessions

Risk Exposure Comparison

The main distinction between retail and wholesale credit insurance lies in how risk is spread. Retail risk is scattered across numerous small transactions, while wholesale risk is concentrated in a smaller number of large B2B accounts. For instance, wholesalers often manage about $200 million in accounts receivable, operating with slim net profit margins (usually under 3%) and gross margins between 13% and 15%. This setup means that a single major buyer default can erase the profits from many otherwise successful transactions. On the other hand, retail credit decisions are typically simpler, involving "accept or reject" choices for smaller loan amounts. As a result, individual defaults in retail have a much smaller impact on the overall portfolio.

During economic downturns, wholesalers tend to see some of the largest spikes in default rates across industries. Meanwhile, retail claims also rise, as higher interest rates and unemployment lead to financial strain on consumers. For example, lawsuits against real estate professionals increased by 9% between 2021 and 2022.

Claims Frequency and Severity Differences

The differences in risk exposure between retail and wholesale credit insurance lead to distinct claim patterns. Retail credit insurance sees a higher number of claims, but these are typically for smaller amounts, as individual consumers file claims during tough financial times. Wholesale credit insurance, by contrast, involves fewer claims, but each claim often represents a substantial financial hit, such as unpaid invoices worth millions.

The U.S. wholesale sector extends over $500 billion in unsecured trade credit annually. This means that when a corporate insolvency occurs, it can lead to claims worth millions of dollars. Wholesale claims also tend to have a "cross-excitation" effect, where an issue in one sector – like banking – can ripple through interconnected supply chains. For example, during the 2008–2012 financial crisis, over 400 U.S. bank closures caused cascading failures across wholesale networks. Retail claims, while they may cluster during periods of economic stress like rising unemployment, are generally isolated events and don’t trigger widespread chain reactions. These differences in claim behaviors play a major role in shaping policy terms and adjustments.

Policy Flexibility and Credit Limit Adjustments

Reflecting these contrasting risk profiles, the structure of retail and wholesale credit insurance policies varies significantly. Retail policies are straightforward and offer customizable options, allowing small businesses and individuals to tailor coverage to their needs without paying for extras they don’t require. Wholesale policies, on the other hand, are highly specialized. Credit limits are set on a per-buyer basis, factoring in variables like the buyer’s size, creditworthiness, and risk level. During recessions, these limits can be slashed by as much as 70% if a buyer’s credit rating drops significantly, such as from Aaa to Ba.

| Feature | Retail Credit Insurance | Wholesale Credit Insurance |

|---|---|---|

| Primary Target | Individuals and small businesses | Large enterprises and B2B firms |

| Policy Nature | Simple, pre-packaged, flexible | Highly tailored and specialized |

| Limit Basis | Standardized coverage | Per-buyer limits based on risk/size |

| Recession Response | Standardized adjustments | Aggressive limit reductions (up to 70%) |

| Claims Process | Streamlined procedures | Complex and time-intensive |

Wholesale policies typically cover 75% to 95% of an invoice’s value, with premiums ranging from 0.2% to 0.6% of total sales. These policies also require "headroom" – a buffer above anticipated accounts receivable – to manage late payments and market volatility. With the average U.S. Days Sales Outstanding sitting at 49 days, this buffer ties up significant capital, especially during economic downturns. Retail policies, in contrast, rely on standardized scoring methods and simpler claims processes, making them easier to navigate.

Managing Credit Insurance During Recessions

Retail Credit Insurance Strategies

For retail businesses, staying ahead during a recession means being proactive with credit management. Start by revising your payment terms to align with current economic conditions. Keep a close eye on overdue payments and follow up promptly. Regularly update and review your customers’ financial information, as this helps you spot potential risks early. Also, be mindful of external factors like supply chain disruptions or geopolitical events that could affect your customers’ ability to pay.

Reducing reliance on a single or small group of customers can also be a game-changer. If one major client becomes insolvent, the impact on your business will be less severe. Use credit intelligence tools provided by insurers to identify early warning signs, such as unusual credit line usage, which often surfaces up to a year before a default occurs.

Another effective tactic is implementing shorter workout periods. This approach can help businesses recover more effectively when customers face financial difficulties.

Wholesale Credit Insurance Strategies

Wholesale businesses face different challenges and need strategies tailored to their unique needs. Unlike retail businesses, wholesalers benefit from real-time credit intelligence and proactive adjustments. Monitoring services can provide valuable insights, helping you identify customers whose financial health might be deteriorating. For instance, a 2025 survey revealed that 80% of manufacturing and wholesale businesses found growth increasingly difficult due to heightened credit risks.

To address these challenges, wholesalers should adapt their policies to cover both commercial risks, such as insolvency or non-payment, and political risks, like government interference or trade restrictions. These risks tend to spike during economic downturns.

"Those that treat trade credit as a managed risk rather than a background function will be best positioned to navigate the next wave of global uncertainty." – Mike Seff, Senior Vice President of Specialty Lines, Intact Insurance Specialty Solutions.

Regularly auditing credit limits is another critical step. Limits that no longer align with your current operations can lead to unnecessary losses. To maintain financial stability in case a major buyer defaults, consider diversifying your financing channels. Combine trade credit insurance with tools like invoice factoring and supply chain financing to keep cash flow steady.

How CreditInsurance.com Helps with Risk Management

Whether you’re in retail or wholesale, having the right tools and support can make all the difference, especially during a recession. CreditInsurance.com offers a suite of online tools designed to help businesses assess risks and explore coverage options tailored to their needs. Their learning portal breaks down complex policies, explains risks, and clarifies technical terms, ensuring businesses fully understand their coverage.

For more personalized guidance, CreditInsurance.com also provides expert consultations. These experts can assist with custom risk assessments and help you determine appropriate credit limits for new customers, giving you the confidence to navigate uncertain times.

Credit Insurance as a Risk Mitigation Tool for International Trade

Conclusion

Recessions influence retail and wholesale credit insurance in unique ways. For retailers, the risk of sudden defaults and reduced coverage is a pressing concern. A striking example is Allianz Trade’s 50% reduction in Boohoo‘s supplier coverage in July 2023. On the other hand, wholesalers, operating with slim margins and managing large receivables, can face significant setbacks from even one buyer’s default.

Understanding these distinctions is crucial for weathering economic downturns. Retailers should prioritize clear communication with insurers and suppliers to maintain confidence, while wholesalers must keep a close eye on credit line usage. It’s worth noting that borrowers on the brink of default often max out their credit limits about a year before failing. Both sectors can reduce risks by diversifying their customer base and strengthening internal controls. Tailored insurance policies are key – retailers need flexibility to handle unpredictable consumer spending, while wholesalers require coverage suited for extended payment terms and larger exposures.

CreditInsurance.com provides the resources businesses need to tackle these challenges head-on. With tools like online risk assessments and personalized consultations on credit limits and policy structures, businesses can better prepare for financial turbulence. Considering that U.S. bankruptcies have spiked 16%, reaching a 13-year high in 2024, having a solid credit risk management plan is more important than ever. By taking proactive steps and leveraging expert support, businesses can navigate economic uncertainty and come out stronger.

FAQs

Which type of credit insurance do I need – retail or wholesale?

Choosing the right type of credit insurance – retail or wholesale – depends on your business model and financial needs. Retail credit insurance is tailored for businesses that sell directly to consumers or small businesses. It safeguards against non-payment, ensuring your cash flow remains steady even if customers fail to pay. On the other hand, wholesale credit insurance is designed for companies that offer credit as part of their supply chain operations. It helps mitigate risks associated with large trade credit agreements. To ensure the best fit for your business, consider discussing your specific financial risks with a provider who can customize a plan to meet your needs.

How do recessions change my credit limits and premiums?

During recessions, credit limits often shrink because businesses and insurers adopt a more cautious approach, anticipating higher risks of defaults and bankruptcies. At the same time, the cost of credit insurance tends to rise as insurers adjust premiums to account for the increased chances of claims. These measures are designed to safeguard cash flow and reduce the risk of bad debts. However, they can also make credit more expensive and harder to obtain, which may temporarily slow down growth opportunities.

What warning signs suggest a customer may default soon?

Delayed invoice payments, frequent requests to change payment terms, partial payments instead of full amounts, and reports of late payments to other businesses are all red flags. These patterns often suggest financial trouble and an increased risk of default.