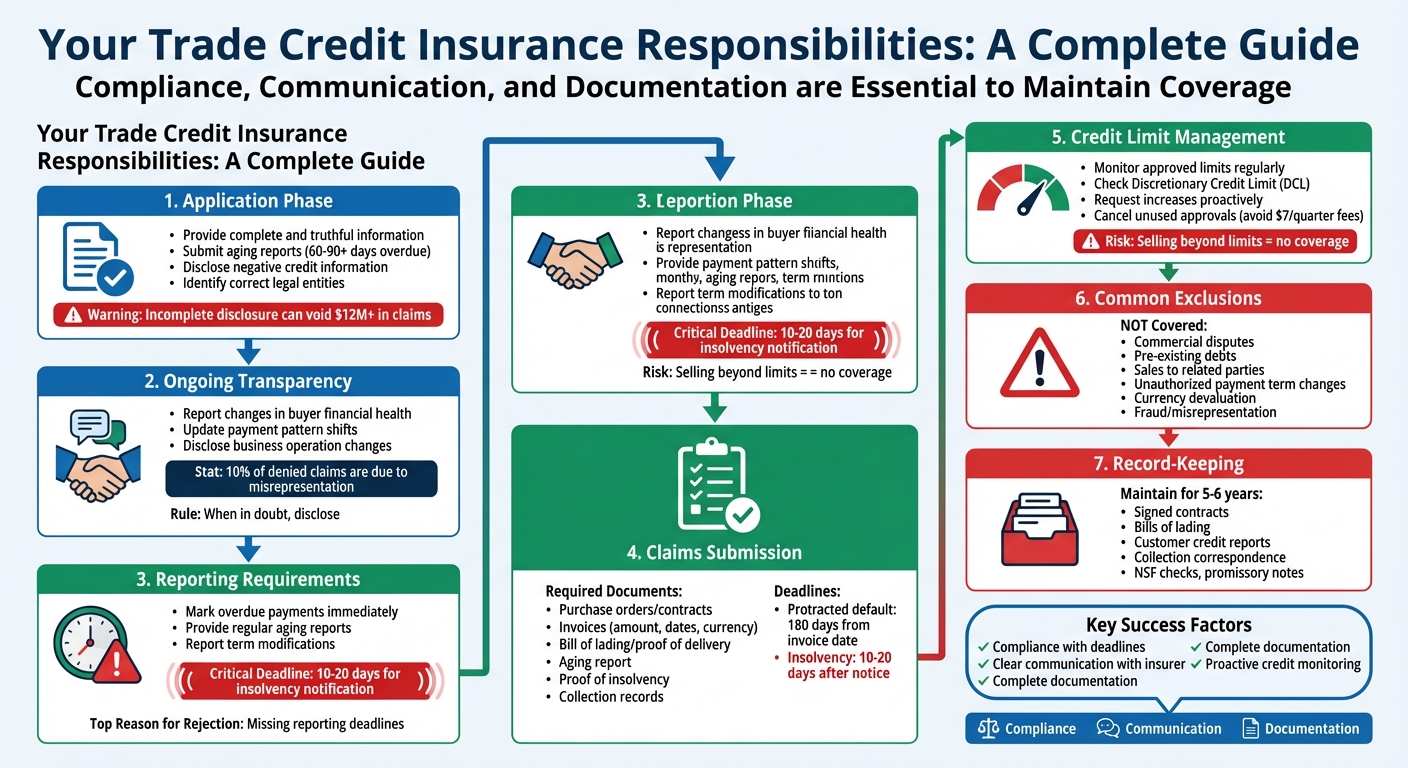

Trade credit insurance protects your business from unpaid invoices, but it comes with clear responsibilities. Failing to meet these obligations can lead to claim denials or policy invalidation. Here’s what you need to know:

- Accurate Applications: Provide complete and truthful information about your sales, customers, and receivables. Misrepresentation can void your policy.

- Ongoing Transparency: Update your insurer about changes in buyer financial health or payment patterns. When in doubt, disclose.

- Timely Reporting: Notify your insurer of overdue payments or buyer insolvency immediately – deadlines are strict (often 10-20 days).

- Proper Claims Submission: Submit claims with all required documents, like invoices, proof of delivery, and collection records, within specified timeframes.

- Credit Limit Management: Monitor buyer credit limits and request increases as needed. Selling beyond approved limits means you’re unprotected.

- Policy Exclusions: Be aware of exclusions like pre-existing debts, disputes over goods, or unauthorized changes to payment terms.

Key Takeaway: Compliance, communication, and documentation are essential to maintain coverage and ensure claims are paid. Missteps – like missing deadlines or incomplete disclosures – are the most common reasons for claim rejection. Treat your insurer as a partner and stay proactive to protect your business.

Trade Credit Insurance Policyholder Responsibilities and Compliance Checklist

PODCAST: Moving forward with Credit Insurance: Mitigating Risk in Trade Finance (S1E18)

sbb-itb-b840488

Basic Duties of the Insured Party

Your responsibilities as a policyholder begin the moment you submit your application. The accuracy of the information you provide can determine whether your policy will protect you when you need it – or leave you exposed to financial risk.

Providing Accurate Information During Application

When applying for insurance, transparency is non-negotiable. You must provide a complete picture of your receivables portfolio, customer base, and business operations. This includes clarifying whether your policy covers domestic sales, export sales, or both, as well as detailing your total sales volume and maximum credit terms.

You’ll also need to submit aging reports to identify customers with debts 60 or 90+ days overdue. Any negative credit information must be disclosed, along with details about the legal entities responsible for debts. For instance, a parent company isn’t automatically liable for the debts of its subsidiaries unless explicitly stated.

A real-world example highlights the risks of incomplete disclosure. In August 2024, a U.S. District Court invalidated over $12 million in claims against Magna Tyres USA, LLC because the company failed to disclose overdue customer debts.

"Policyholders must disclose any information that could affect the insurer’s decision to provide coverage or impact the risk being insured. Omissions can void the policy."

– Chip Merlin, President, Merlin Law Group

Once you sign your application, you are legally bound by its accuracy. Double-check every detail before submission, and ensure your invoice terms align precisely with what’s outlined in your application. Even minor inconsistencies could result in claim denials.

Providing accurate information at the outset is just the first step. Ongoing transparency is equally critical.

Maintaining Transparency with the Insurer

Your responsibility to keep your insurer informed doesn’t end once your policy is approved. Misrepresentation – whether intentional or accidental – accounts for about 10% of denied insurance claims annually. To avoid this, you must maintain open communication and share any updates that could affect your risk profile.

This means informing your insurer of changes in your customers’ financial health, shifts in payment patterns, or significant adjustments to your business operations. These updates allow insurers to adjust credit limits and monitor coverage effectively.

"A misrepresentation may be a false statement or a failure to disclose where a duty to disclose exists."

– Peter A. Halprin and Vivian Costandy Michael, Attorneys, Anderson Kill

To safeguard yourself, follow the principle of “when in doubt, disclose.” Document all material facts in writing to create a clear record of your communications. In some jurisdictions, failing to disclose material information could result in the insurer not only denying your claim but also keeping your premium. The consequences of withholding information are simply too severe to take any chances.

Reporting and Claim Management Responsibilities

Accurate reporting and timely claim submissions are essential for maintaining your trade credit insurance benefits. Once your policy is active, it’s crucial to report buyer payment issues and follow claim procedures carefully. Missing these steps is the leading cause of claim rejection. Here’s how consistent reporting and proper claim submissions help safeguard your coverage.

Regular Reporting of Buyer Information

If a buyer fails to pay within the agreed terms, you must notify your insurer. This involves officially marking the overdue status as a claim through your insurer’s digital platform. Additionally, you’ll need to provide aging reports regularly – these reports outline all overdue accounts and the length of payment delays.

Changes to your original terms of sale must also be reported. For example, modifying payment terms without notifying your insurer could result in a policy breach. The same applies to repayment plans – get written approval from your insurer before agreeing to any new terms to avoid invalidating your claim.

In cases of buyer insolvency, immediate action is required. If a customer files for Chapter 11 or declares bankruptcy, you generally have only 10 to 20 days to notify your insurer and file a claim. Missing this deadline will likely result in automatic claim denial, even if the debt is legitimate.

"Probably the most common reason for the rejection of a claim, is the failure to adhere to the maximum reporting period."

– Credit Guarantee

If a buyer exceeds the policy’s grace period, stop shipments immediately to maintain your coverage.

Once buyer issues are reported promptly, the next step is ensuring claims are submitted correctly.

Submitting Claims Correctly

Claims are divided into two main types: protracted default (when a buyer cannot pay but hasn’t filed for bankruptcy) and insolvency (legal bankruptcy or liquidation). Each type has specific documentation requirements and filing deadlines.

For protracted default claims, you must file within 180 days of the invoice date (e.g., 150 days for invoices with 30-day terms). Insolvency claims, however, come with tighter deadlines – typically 10 to 20 days after receiving notice of the buyer’s filing.

Before filing, confirm that non-payment meets the terms of your policy and that the required waiting period has passed. Then, gather the necessary documentation:

| Required Documentation | Purpose |

|---|---|

| Purchase Orders / Contracts | Verifies the buyer ordered the goods or services |

| Invoices | Details the amount owed, due dates, tax, and currency |

| Bill of Lading / Proof of Delivery | Confirms that goods were shipped and received |

| Aging Report | Shows the debt is overdue and aligns with policy timelines |

| Proof of Insolvency | Required for bankruptcy claims (e.g., Schedule F) |

| Collection Records | Demonstrates your efforts to recover the debt before filing |

Pay special attention to the legal entity listed in your claim. Filing against a parent company instead of the specific subsidiary responsible for the debt is a common mistake that can lead to immediate rejection. Always cross-check your policy schedules with your invoice headers for accuracy.

If there are disputes about the quality of goods or services, or delivery issues, resolve these before filing your claim. Insurers won’t intervene in these disputes, so you may need to pursue legal action if necessary.

"One of the non-negotiables for the insurer is late filing a claim (missing the window to file the claim)."

– Kirk Elken, Co-founder, Securitas Global Risk Solutions

Once your claim is approved and settled, you’ll assign the rights to the receivables to your insurer. This allows them to pursue further recovery from the debtor. Trade credit insurance typically covers up to 90% of the debt, and this process helps insurers recover their payout.

Credit Limit Management for Insured Parties

Keeping a close eye on approved credit limits is as important as ensuring accurate reporting and claims submission. Every buyer is assigned a specific credit limit by your insurer, and exceeding that limit or selling to a buyer who has been declined means you’re taking on the credit risk yourself – without insurance coverage. If that buyer fails to pay, the loss is entirely yours. Managing these limits carefully is a critical part of protecting your policy.

Monitoring Approved Credit Limits

Your insurer’s digital platform is an essential tool for staying on top of credit limits. Make it a habit to regularly check that each buyer’s approved limit is sufficient to cover their outstanding balance. Insurers can adjust or cancel limits at any time, so staying vigilant is key .

If your policy includes a Discretionary Credit Limit (DCL), take the time to review your Coverage Certificate. This will tell you the maximum amount you can approve on your own without needing the insurer’s input. Keep in mind that buyers under a DCL may not automatically appear in your online portfolio, so you might need to add them manually to ensure they’re covered for any future claims.

If you’re managing multiple policies – like separate ones for export and domestic coverage – organize approvals by policy number (e.g., "E" for export and "D" for domestic) to avoid mix-ups. Pay particular attention to temporary credit approvals, which come with expiration dates rather than remaining active indefinitely. Letting unused approvals linger can lead to fees (around $7 per approval per quarter). To avoid unnecessary charges, cancel limits for buyers you no longer work with.

Requesting Credit Limit Adjustments

Once you’re actively monitoring limits, it’s important to act quickly when adjustments are needed. If a buyer is nearing their approved limit, request an increase immediately through your insurer’s digital platform. Head to the "Manage Limit" menu, select the buyer, and choose the option to request a higher limit. Be sure to use the buyer’s legal company name and address as listed on purchase orders to avoid delays.

To speed up the approval process, attach relevant documents like recent financial statements or credit reports . If your request isn’t approved right away, it may go into a pending status while the underwriter evaluates the buyer’s creditworthiness or asks for more information.

Before submitting a request, calculate your maximum exposure. For example, if you deliver goods every 30 days with 90-day payment terms, your credit limit should cover at least three months of shipments. Seasonal businesses should also plan ahead by requesting temporary increases during peak times, like the holiday season when order volumes spike. And if a customer asks for payment terms that differ from those outlined in your policy – such as longer repayment periods – you’ll need to get an Approved Limit from your insurer instead of relying on your DCL.

Compliance and Exclusions in Trade Credit Insurance

Understanding what your trade credit insurance covers is crucial, but knowing what it doesn’t cover is just as important. While the policy shields you against risks like buyer insolvency and prolonged non-payment, it’s not an all-encompassing safety net. Certain exclusions can leave you exposed if overlooked.

Understanding Policy Exclusions

One of the most common reasons claims are denied is commercial disputes. Insurers won’t intervene until disputes over goods or services are legally resolved. As Jason Benson, Global Head of Structured Working Capital at J.P. Morgan, puts it:

"If there’s a receivable for 100 products, and the buyer says only 80 were delivered, the insurer’s payment obligation may only be on the undisputed amount".

Other standard exclusions include pre-existing debts – amounts already overdue before your policy began – and sales to related parties, such as subsidiaries or affiliates. Extending payment terms to a buyer without your insurer’s approval or continuing to ship goods to a defaulting buyer can also void your coverage entirely.

Additional exclusions often include:

- Currency devaluation losses

- Failure to obtain necessary export or import licenses

- Losses from contracts that aren’t legally valid or enforceable

- Natural disasters like earthquakes or floods

- War or civil unrest (though optional riders may cover these)

- Fraud or misrepresentation, such as inflating claims or providing false buyer credit data

| Covered Reasons (Typical) | Common Exclusions |

|---|---|

| Buyer Insolvency/Bankruptcy | Disputes over goods or service quality |

| Protracted Default (Non-payment) | Pre-existing debts (prior to policy start) |

| Political Risk (if specified) | Sales to related/affiliated companies |

| Government Intervention (if specified) | Currency devaluation losses |

| Repudiation (Refusal to accept goods) | Failure to maintain valid export/import licenses |

| War or Civil Unrest (if specified) | Unauthorized extension of payment terms |

With these exclusions in mind, adhering to your policy’s requirements is non-negotiable.

Meeting Policy Conditions

Knowing what’s excluded is only half the battle – sticking to the rules laid out in your policy is just as critical. For example, reporting deadlines are strict, and policies often require you to stop shipping to buyers who are overdue. EXIM underscores this point:

"Both your policy and your Discretionary Credit Limit Endorsement require you, in certain situations, to stop shipping to buyers who are overdue on their payment".

Failing to halt shipments to a defaulting buyer can void coverage not only for future sales but for past ones as well.

Another key requirement is accurate documentation. Insurers demand third-party verification of exports – internal records won’t suffice. Bills of lading must come from unaffiliated carriers, and buyer details must match perfectly across invoices, contracts, and shipping documents. Even minor discrepancies, like a misspelled name, can lead to claim rejection. Additionally, insurers require regular sales declarations for premium calculations and proof that you’re actively pursuing unpaid invoices. As Coface explains:

"To be effective, credit insurance should be a partnership between both parties. You tell the insurer about customers’ payment behaviour and notify the insurer of overdue payments".

The reality is that administrative missteps, not the default itself, are often the root cause of denied claims . Staying organized and proactive ensures your coverage remains intact when you need it most.

Record-Keeping and Renewal Responsibilities

Keeping your records up to date is more than just a good habit – it’s essential for maintaining your coverage. Insurers depend on accurate documentation to verify claims, calculate premiums, and reassess risks when it’s time to renew. If your records are incomplete or outdated, you could face challenges with claims or even risk losing coverage altogether.

Maintaining Accurate Sales and Transaction Records

Every transaction you handle should be backed by proper documentation. This includes legally binding contracts that clearly outline buyer details, descriptions of goods or services, pricing, payment terms, and delivery schedules. These contracts must include the full legal names of both parties, along with signatures and dates.

In addition to contracts, you’ll need proof of fulfillment – such as bills of lading, waybills, or written confirmations of delivery from your customers. These documents demonstrate that you’ve met your obligations. Insurers also expect you to maintain credit management records, which should include customer credit reports and any follow-up actions you’ve taken on overdue payments. If you ever need to file a claim, having documents like NSF checks, signed drafts, promissory notes, or written acknowledgments of debt can be crucial.

| Record Category | Specific Document Examples | Purpose in Policy Management |

|---|---|---|

| Sales/Contract | Signed Purchase Orders, Sales Contracts | Confirms the existence of a legal debt |

| Logistics | Bills of Lading, Waybills, Delivery Receipts | Proves obligations were fulfilled |

| Credit/Financial | Customer Credit Reports, Financial Statements | Shows creditworthiness and due diligence |

| Collection | Correspondence Logs, Demand Letters, NSF Checks | Documents efforts to mitigate losses |

| Policy/Renewal | Updated Sales Forecasts, Risk Profiles | Helps calculate premiums and adjust coverage |

If you need to make changes – like updating contract terms or delivery schedules – get those modifications in writing from your customer to ensure your policy remains valid. Creating a standardized file for each account, including purchase orders, proof of shipment, and a record of collection efforts, can save you time and effort during the claims process. It’s worth noting that many states require insurance-related records to be kept for five to six years. Digitizing these records can help protect them from loss and make audits much easier.

Thorough documentation doesn’t just support your claims; it also lays the groundwork for accurate and smooth policy renewals.

Updating Risk Profiles During Renewal

When it’s time to renew your policy, your risk profile needs to be as current as your records. Insurers require updated details to reassess risks effectively. As Burkhard Wittgen, Global Head of Multinationals at WTW, explains:

"Programmes should be designed for certainty, not renewed on autopilot".

Insurers are moving away from one-time risk assessments and instead focusing on continuous monitoring of payment behaviors and trading conditions. This means your renewal submission must include up-to-date information about your customers’ financial health, your commercial terms, and any broader economic or political factors that might affect your business. With business bankruptcies on the rise since Q2 2022, underwriters are paying closer attention to payment patterns and risk profiles.

To strengthen your renewal submission, highlight resilience factors like your ability to adapt, financial flexibility, and how well you handle external pressures such as tariff changes or shipping delays. While traditional indicators like business longevity still matter, insurers are increasingly prioritizing these adaptability measures. For example, in 2025, global credit limit approval rates averaged 74%, with North America leading at 84%. A well-prepared renewal submission can be the difference between maintaining seamless coverage and encountering unexpected gaps.

Conclusion

Keeping up with your responsibilities throughout the policy period is crucial for getting the most out of trade credit insurance. Success in managing your coverage effectively revolves around three critical areas: compliance, communication, and documentation.

Make sure to file claims within the required deadlines to protect your recovery rights. Staying on top of follow-ups, maintaining accurate records, and securing prior approval for any changes to terms are all essential steps to ensure your coverage stays strong and reliable. As highlighted earlier, these three pillars – compliance, communication, and documentation – are the foundation of solid risk management.

Think of your insurer as more than just a policy provider – they’re a partner in managing risk. Frequent updates on shifting buyer conditions, precise reporting of overdue accounts, and proactive requests for credit limit adjustments help keep your coverage secure. Clear and consistent communication can even simplify the claims process.

Ultimately, meeting these responsibilities goes beyond avoiding denied claims. It’s about getting the most value from your policy and protecting your business against the financial strain of customer defaults.

FAQs

What counts as a “material change” I must disclose to my insurer?

A "material change" refers to any major shift in your situation that might increase the insurer’s level of risk after your policy has started. This could include things like expanding your business operations, purchasing new equipment, or changing ownership. It’s important to disclose these changes if they might have impacted the insurer’s decision when they issued your policy or if they could potentially alter your premium.

If a buyer pays late, when do I have to report it to keep coverage?

To keep your coverage active, it’s crucial to report any late payments to your insurer within the timeframe outlined in your policy. Typically, this means notifying them within 7 days of the payment becoming overdue. Be sure to review your policy terms to verify the exact reporting deadline.

What happens if I ship beyond an approved credit limit?

If you exceed an approved credit limit when shipping goods, the insurer might not cover any resulting losses. This means you could end up being responsible for the unpaid balance. Credit limits are set by the insurer as the maximum amount they will cover for each buyer. To avoid this risk, always double-check that your shipments stay within the approved limits.