Businesses often misunderstand key terms in trade credit insurance policies, leading to denied claims, financial losses, and operational issues. Here’s what you need to know:

- Insolvency: It’s not just bankruptcy. It includes a customer’s inability to pay, even without formal proceedings. Misinterpreting this can delay claims and reduce recovery chances.

- Policy Coverage: Trade credit insurance protects against more than bankruptcies, including slow payments and political risks. Policies can reimburse up to 90% of invoice value.

- Selective vs. Full Turnover Policies: Full turnover covers all accounts receivable, while selective policies focus on specific customers or invoices. Each has different costs and management requirements.

- Credit Limit Reductions: These are early warnings of buyer risk, not penalties. Use this notice to reassess relationships and reduce exposure.

Misunderstandings can lead to financial setbacks, like unpaid invoices or voided coverage. To avoid these pitfalls, businesses should:

- Assign a dedicated policy manager.

- Train teams on policy terms.

- Work with brokers or specialists for tailored advice.

- Use educational tools to clarify complex terms.

Understanding and managing your policy effectively can help protect your business from risks and improve financial stability.

Master our Common Trade Credit Insurance (TCI) Terms

sbb-itb-b840488

Most Commonly Confused Policy Terms

Full Turnover vs Selective Trade Credit Insurance Policies Comparison

Trade credit insurance often involves technical terms that can confuse business owners, delaying claims and putting cash flow at risk. Misunderstandings about insolvency, coverage details, turnover options, and credit limit reductions can lead to costly mistakes. Knowing what these terms mean is key to getting the most out of your policy.

What ‘Insolvency’ Actually Covers

One common misconception is that ‘insolvency’ only applies when a customer officially declares bankruptcy. This misunderstanding can cause delays in filing claims and recovering funds.

Insolvency, however, refers to a debtor’s inability to meet payment obligations, even without formal bankruptcy proceedings. It’s distinct from protracted default, which occurs when a payment remains overdue for more than 180 days without legal insolvency. Waiting for formal bankruptcy proceedings to file a claim could mean losing the opportunity to claim under protracted default provisions. Policies often cover scenarios like reorganization or extended non-payment well before a formal bankruptcy is declared.

What Policies Actually Cover

Trade credit insurance isn’t just about protecting against customer bankruptcies. These policies can also cover slow payments, political risks, and various forms of insolvency, including reorganization. In many cases, they reimburse up to 90% of the invoice value. Understanding these details is critical when deciding between selective and full turnover policies.

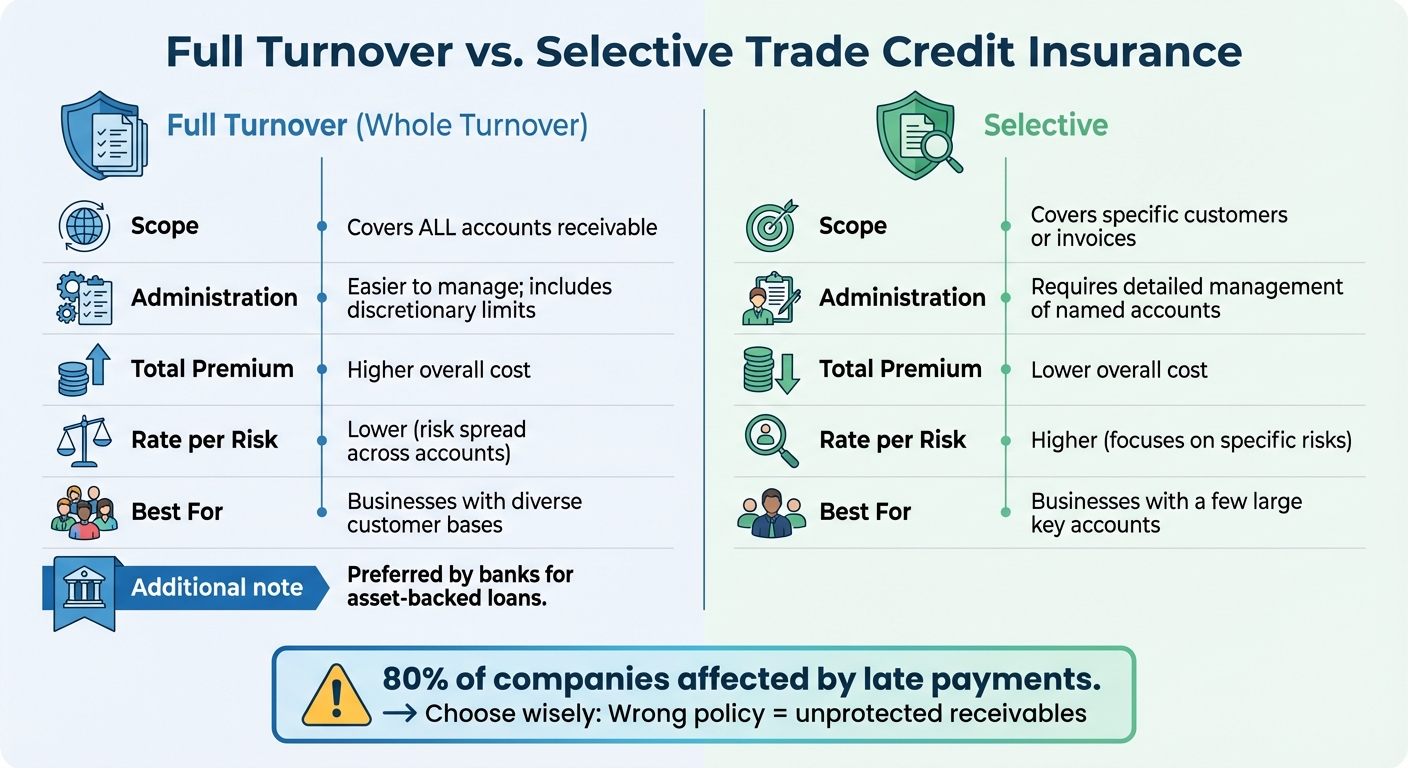

Selective vs. Full Turnover Policies

Your choice between selective and full turnover policies depends on the level of coverage you need. These two approaches differ in their scope and how they’re managed.

Full turnover policies – sometimes called "whole turnover" or "comprehensive" policies – cover your entire accounts receivable portfolio. This means protection against non-payment from all customers. Selective policies, on the other hand, focus on specific high-value invoices, key accounts, or transactions in regions with higher risks.

While selective policies might seem simpler due to their limited focus, they require more hands-on management. Each account or transaction must be individually underwritten. Full turnover policies, by contrast, offer broad coverage and often include discretionary limits for smaller accounts.

Here’s a quick comparison:

| Feature | Full Turnover (Whole Turnover) | Selective |

|---|---|---|

| Scope | Covers all accounts receivable | Covers specific customers or invoices |

| Administration | Easier to manage; includes discretionary limits | Requires detailed management of named accounts |

| Total Premium | Higher overall cost | Lower overall cost |

| Rate per Risk | Lower, as risk is spread across accounts | Higher, since it focuses on specific risks |

| Best For | Businesses with diverse customer bases | Businesses with a few large key accounts |

With late payments affecting 80% of companies – and unpaid invoices often leading to bankruptcies – choosing the wrong policy could leave a significant portion of receivables unprotected. Additionally, banks often prefer full turnover policies when businesses seek asset-backed loans, as these policies secure the entire receivables portfolio.

What Credit Limit Reductions Mean

Credit limit reductions are often misunderstood as penalties, but they’re more like early warnings about potential buyer risks. When an insurer lowers a credit limit, it’s usually based on updated negative information about the buyer’s financial health – often insights that aren’t yet publicly available. These changes only apply to future transactions, and businesses typically receive 30 to 60 days’ notice before the new limits take effect.

"Businesses often view this not as a problem but as a useful alert to changes in their risk exposure, acting as an ‘early warning system’ that can help them avoid bad debt or at least prevent increasing their exposure at the wrong time." – Lockton

Instead of immediately disputing a credit limit reduction, businesses should use the notice period to investigate the reasons behind the change. This is an opportunity to reassess the buyer relationship and take steps to reduce exposure. If the reduction seems unjustified, businesses can challenge it by providing updated financial data or a record of the buyer’s strong payment history. With insurance payouts for unpaid invoices rising by 23% in the first half of 2023, these early warnings are more valuable than ever.

How Misunderstandings Affect Businesses

Misinterpreting policy terms can lead to more than just confusion – it can cause serious financial and operational issues that jeopardize a company’s stability. Recognizing how these misunderstandings unfold highlights the importance of clear communication and understanding.

Financial Losses and Missed Opportunities

Misunderstanding policies often results in financial setbacks. For example, shipping goods to customers who have reached a "state of default" – when the Maximum Extension Period has expired – leaves businesses exposed to full losses, as these shipments are no longer covered under insurance.

"If I ship new goods at this stage [state of default], I assume the risk of non-payment at my own expense."

– Nicolas Marchenoir, Head of Commercial Underwriting, Allianz Trade in France

Another common issue arises when businesses exceed discretionary limits, leaving the excess amount unprotected. Additionally, most policies exclude payment disputes requiring legal action. Since policies typically cover only 75% to 95% of the debt value, these gaps can create significant cash flow problems. To bridge these gaps, companies often resort to costly financing measures – a reality faced by 74% of UK small businesses dealing with overdue invoices.

The financial collapses of ISG Group (debts of $340 million) and Buckingham Group (debts over $108 million) in late 2023 and 2024 illustrate the risks. Suppliers who misunderstood their credit insurance coverage or lacked it altogether were left with unpaid invoices, while those with well-managed policies were able to recover funds efficiently.

These financial challenges are often compounded by inefficiencies that disrupt daily operations.

Operational Problems and Delays

Policy misinterpretations don’t just hurt finances – they also create operational bottlenecks. Businesses that view credit insurance as a reactive tool, useful only after a loss, miss out on its proactive benefits. Insurers often provide predictive analytics and risk assessments, which can help businesses evaluate new or unfamiliar customers. Ignoring these tools can limit market growth and the ability to offer competitive payment terms.

Another frequent oversight involves invoicing periods. Many policies specify a maximum time between delivery and invoice issuance – often 30 days. Exceeding this period renders the debt uninsurable. In France, for instance, the Modernization of the Economy Act prohibits payment terms longer than 60 days. Misunderstanding such regulations can void coverage altogether.

"If the maximum invoicing term is exceeded, the debt cannot be insured."

– Nicolas Marchenoir, Head of Commercial Underwriting, Allianz Trade in France

These delays and errors drain resources, forcing businesses to chase unpaid invoices and perform their own solvency checks – tasks that pull focus away from core operations and often cost more than expected. Properly understanding policy terms is critical not only for avoiding financial risks but also for ensuring smooth and efficient operations.

How to Better Understand Your Policy

Making sense of policy language is crucial for managing risks effectively and getting the most out of your coverage. By combining educational resources with expert advice, you can break down complex terms and navigate your policy with confidence.

Using Educational Tools

Your policy document is your go-to guide. It outlines covered risks, exclusions, claim deadlines, and settlement timelines. Start with the declarations page to identify key details like your sales basis, premium rate, insured retention (commonly around 10%), and policy limits. Pay close attention to endorsements – general ones set standard terms, while specific ones address unique needs, such as consignment coverage.

Specialized glossaries can help you align your understanding with the precise legal definitions in your policy. Terms like "insolvency", "protracted default" (which typically kicks in after 180 days of non-payment), and "aggregate limit" often vary by region and local regulations. Websites like CreditInsurance.com provide glossaries and FAQs to clear up common misconceptions. For instance, they explain the difference between business credit insurance and credit life or disability insurance. These resources also clarify distinctions like the invoicing period (the time between delivery and issuing an invoice) versus terms of payment (the credit limit period stated on the invoice). Understanding these nuances can significantly impact your coverage.

"Understanding the terminology of credit insurance is just the first step."

– CreditInsurance.com

While educational tools are a great starting point, working with professionals ensures you apply this knowledge effectively.

Working with Insurance Professionals

Partnering with a broker or trade credit insurance specialist can provide tailored advice. Brokers compare quotes from multiple carriers – a process that usually takes two to three weeks – and assist with mandatory reporting and claim submissions at no additional cost, as rates remain the same whether you go through a broker or directly to the insurer.

Professionals can help you navigate policy language, such as defining what qualifies as a "default" (full non-payment versus partial payment), or explaining technical terms like the Maximum Extension Period (MEP), which determines when new shipments lose coverage. Joseph Jean, Partner at Pillsbury Winthrop Shaw Pittman LLP, highlights the importance of simplifying terms:

"The key to transferring that risk is having the broadest coverage available, on the most simplified terms".

Additionally, experts can help refine exclusions – like those for "war" or "cyber warfare" – to ensure they don’t unintentionally block coverage for trade disputes or cyberattacks.

Staying in regular contact with your insurer is also essential. This ensures timely adjustments to credit limits and keeps your policy aligned with your needs. By combining educational tools with expert guidance, you can turn your policy into a powerful tool for managing risks and protecting your business.

Conclusion

This study highlights how crucial it is to fully understand policy terms when managing financial risks. Overlooking key details in your trade credit insurance can lead to denied claims, especially if you miss strict notice deadlines or fail to follow stop shipment protocols. These aren’t just minor oversights – they can determine whether you recover 90% of an unpaid invoice or bear the entire loss yourself.

But the impact goes beyond just claims. Lenders are more willing to offer higher advance rates – jumping from 70% on uninsured receivables to 80–85% on insured ones. On top of that, knowing your policy inside and out can reduce borrowing costs by 25 to 75 basis points. Terms like the Maximum Extension Period or the definition of "insolvency" can directly influence your financing options.

"Trade credit insurance isn’t about expecting the worst, it’s about being ready for anything." – Atradius

The good news? Most of these pitfalls can be avoided. Assigning a dedicated policy manager, training your sales team on policy limits, integrating buyer limits into your ERP system, and ensuring international invoicing complies with local laws (like France’s 60-day limit) are all practical steps.

When you truly understand and apply policy terms, trade credit insurance becomes more than a safety net – it becomes a tool for growth. You can avoid coverage gaps, secure better financing, and offer competitive payment terms. Resources like CreditInsurance.com provide helpful glossaries and FAQs, but the real advantage comes from consistently applying this knowledge across your organization.

FAQs

When should I file a claim if a customer stops paying but hasn’t declared bankruptcy?

If a customer fails to pay because of protracted default or insolvency, it’s time to file a claim. Most policies give you up to 180 days from the invoice date to do so, but it’s crucial to double-check your policy for the specific deadlines. Staying within these timelines is essential to keep everything on track.

How do I choose between a full turnover policy and a selective policy for my receivables?

When deciding between a full turnover policy and a selective policy, it’s all about aligning with your business’s risk tolerance and goals.

A full turnover policy offers coverage for all receivables. This approach provides broad protection and simplifies management since everything is covered under one umbrella. On the other hand, a selective policy focuses on specific customers or receivables. This can give you more targeted protection and may come with lower premiums.

To make the right choice, consider factors like your risk exposure, the nature of your customer base, and your operational priorities. Balancing these elements will help you find the policy that best supports your business needs.

What should I do right away after my insurer reduces a buyer’s credit limit?

When you notice a reduction, it’s important to understand why it happened. Reach out to your insurer for a detailed explanation. Once you have clarity, you might want to rethink your credit management approach. This could involve reviewing your payment terms or even expanding your customer base to reduce potential risks.