Credit insurance helps tech companies protect themselves from unpaid invoices, client bankruptcies, and delayed payments. It ensures cash flow stability, supports growth, and reduces financial risks, especially in B2B transactions where extended payment cycles and high-value deals are common. Here’s how it works:

- Risk Protection: Covers losses from customer insolvency, payment delays, and political disruptions in global trade.

- Cash Flow Stability: Helps companies manage payroll, R&D, and operational costs even when payments are delayed.

- Growth Support: Enables businesses to offer flexible credit terms, expand globally, and take on high-risk clients like startups.

- Industry Applications: SaaS providers safeguard subscription revenue, hardware manufacturers manage supply chain risks, and fintech firms secure better financing terms.

Credit Insurance as a Risk Mitigation Tool for International Trade

sbb-itb-b840488

Why Tech Companies Use Credit Insurance

Tech companies operate under unique financial pressures, including long payment cycles, high-value deals, and a customer base often filled with volatile startups. These factors can put a serious strain on cash flow. If a major client defaults or delays payment, the effects can ripple through the company – delaying payroll, disrupting subscription payments, and piling up operational costs.

The risks grow even more severe when intellectual property (IP) is involved or when a company relies heavily on a small number of large customers. A client default during an IP dispute or the collapse of a key customer can leave a tech firm scrambling for funds to keep essential operations running. These challenges highlight why tailored credit protection is so critical for B2B transactions in the tech sector.

Managing Payment Risks in B2B Transactions

Credit insurance acts as a safety net, protecting tech firms from unpaid invoices and reducing the impact of bad debt. This is especially important in B2B tech sales, where payment terms often stretch 60, 90, or even more days. During these long payment cycles, companies still need to cover their operating costs while waiting for payments to come in.

Insurers provide access to powerful databases filled with business information, helping tech firms evaluate the creditworthiness of potential and existing customers. This allows them to chase high-reward opportunities without jeopardizing their financial stability. And for companies operating internationally, the challenges – and the need for protection – are even greater.

Supporting Global Expansion

Expanding into international markets brings an entirely new set of risks. From unfamiliar legal systems to varying business practices and political instability, these factors can disrupt trade. Credit insurance helps manage these uncertainties by safeguarding against customer insolvencies in foreign markets. Insurers bring valuable local expertise and insights, aligning with a tech company’s global presence. This support allows businesses to confidently enter new markets while extending flexible payment terms to customers.

Enabling Business Growth

One of the biggest strategic advantages of credit insurance is how it helps tech companies balance growth with risk. By offering more flexible credit terms, companies can boost sales and improve customer loyalty without exposing themselves to unnecessary financial risks. Credit insurance also plays a pivotal role in supporting major business moves. For example, Ingram Micro’s strong credit management system – backed by insurance – was a key factor in its successful acquisition of BrightPoint Inc., a distributor of mobile technologies.

Case Studies: Tech Companies Using Credit Insurance

SaaS Providers Protecting Subscription Revenue

SaaS companies often struggle to maintain consistent revenue streams, especially when clients operate on extended payment terms. Credit insurance steps in as a safeguard, protecting these businesses when customers fail to meet their financial obligations during a contract.

This type of insurance covers unpaid invoices and legal expenses, which can be critical for SaaS providers defending intellectual property claims in cases of customer default. With this safety net, SaaS companies are more willing to work with high-growth startups, even those that come with a higher risk of failure. By using credit insurance as a financial buffer, they can confidently offer services to clients with substantial revenue potential.

Other tech sectors, like hardware manufacturing, also use credit insurance to address the challenges of long payment cycles.

Hardware Manufacturers Reducing Supply Chain Risks

Hardware manufacturers often face lengthy payment cycles, averaging about 47 days. For companies with extended production timelines, these delays can create serious financial challenges.

Take CEL Aerospace Test Equipment Ltd., for example. In September 2024, the company introduced a tailored "Outstanding Amount Policy" to address these issues. CEL, which produces gas turbine test systems with project timelines that can last up to 14 months, needed credit insurance to meet its bank’s requirements for financing. Under the guidance of Joel Pouliot, Vice President of Finance, the company secured insurance that covered not only final invoices but also development costs and project milestones. This approach helped CEL maintain crucial bank financing during a period of rapid growth, all while keeping insurance costs lower than those associated with standard accounts receivable policies.

"The lengthy project time lines were a concern to our bank and the reason why it insisted CEL have credit insurance coverage to protect their receivables and project development costs."

- Joel Pouliot, Vice President of Finance, CEL Aerospace Test Equipment Ltd.

Fintech Firms Improving Lending Capacity

Fintech companies also benefit significantly from credit insurance, using it to secure better financing terms and maintain the liquidity needed to scale their operations. Banks are more willing to extend credit lines when receivables are insured, as these accounts are seen as lower-risk collateral.

This protection is especially useful when fintech firms work with startup clients. Credit insurance acts as a safety net, allowing these companies to take on higher-risk opportunities without jeopardizing their financial health. Additionally, having insured receivables boosts investor confidence, as it helps fintech firms maintain strong credit scores. This, in turn, makes it easier to attract the capital needed for growth and expansion.

Credit Insurance Policy Features for Tech Companies

Multibuyer vs Single-Buyer Credit Insurance Policies for Tech Companies

Tech-Specific Policy Features

Tech companies gain a lot from credit insurance policies tailored to their unique needs. One standout feature is non-cancelable limits, which ensure stable credit lines essential for receivables-based lending. This is especially helpful for tech firms that rely heavily on just one or two major clients, as it provides a safety net against high concentration risk.

Another critical feature is political risk coverage, which shields companies from non-payment caused by government actions, currency issues, or political unrest. Considering that default rates in emerging markets can be up to three times higher than in advanced economies, this kind of protection is invaluable for tech businesses expanding internationally.

Modern policies also include real-time digital monitoring, which integrates with ERP systems to send instant alerts about premium payments or limit breaches. On top of that, high indemnity levels – covering 90% to 95% of receivables – help protect against defaults on major B2B transactions. This is crucial for tech companies, as long payment cycles can strain cash flow, impacting key areas like payroll and R&D.

These features allow tech firms to better manage cash flow and confidently handle high-risk transactions. But alongside these specialized options, the type of policy a company chooses can also greatly influence how risks are managed.

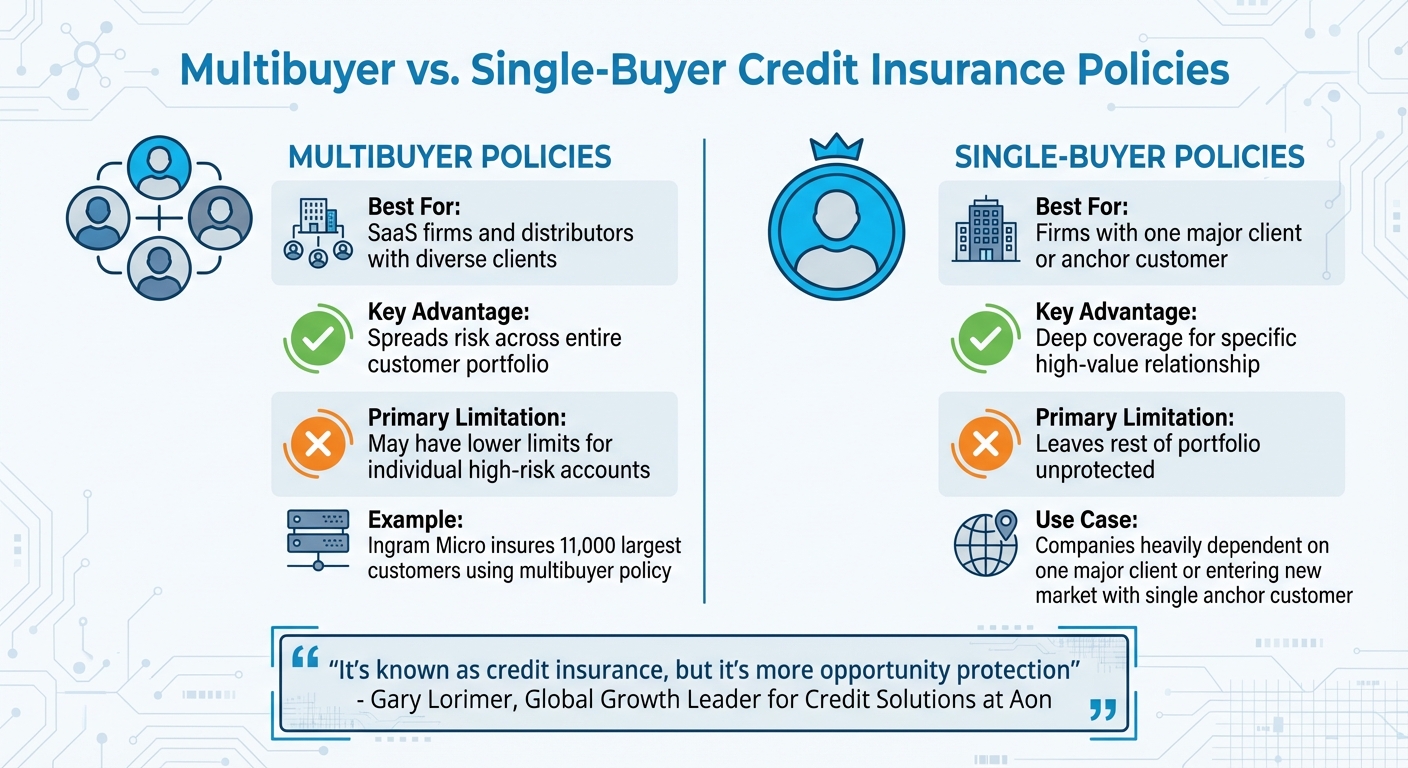

Multibuyer vs. Single-Buyer Policies

When it comes to structuring credit insurance, tech firms typically decide between multibuyer and single-buyer policies. Each has its strengths, depending on the company’s client base and risk exposure.

Multibuyer policies cover an entire portfolio of customers, making them ideal for SaaS companies or distributors with a wide range of clients. A great example is Ingram Micro, the world’s largest tech distributor. In January 2022, the company used a multibuyer policy to insure 11,000 of its largest customers while managing 69,000 smaller accounts through business intelligence feeds from its insurance partner.

"Within our business, credit management sits at the fulcrum of a ‘business balance’ with sales on one side and risk on the other."

- Frederic Wittemans, Director of Credit for Europe, Ingram Micro

On the other hand, single-buyer policies provide deep coverage for specific high-value accounts. These are perfect for companies heavily dependent on one major client or entering a new market with a single anchor customer. The downside? While these policies offer robust protection for key accounts, they leave the rest of the portfolio uncovered. In contrast, multibuyer policies spread risk across the entire ledger but may offer lower limits for particularly high-risk accounts.

| Policy Type | Best For | Key Advantage | Primary Limitation |

|---|---|---|---|

| Multibuyer | SaaS firms and distributors with diverse clients | Spreads risk across an entire customer portfolio | May have lower limits for individual high-risk accounts |

| Single-Buyer | Firms with one major client or anchor customer | Deep coverage for a specific high-value relationship | Leaves the rest of the portfolio unprotected |

Gary Lorimer, Global Growth Leader for Credit Solutions at Aon, sums it up well:

"It’s known as credit insurance, but it’s more opportunity protection".

This highlights how tech companies are increasingly using credit insurance not just to manage risks, but also to unlock financing options and pursue growth opportunities that might otherwise feel too risky.

Research Data: Benefits and Best Practices

Financial Stability and Risk Reduction

Credit insurance plays a crucial role in balancing sales opportunities with potential risks. Frederic Wittemans, Director of Credit for Europe at Ingram Micro, highlights how this balance is essential for tech companies aiming to grow aggressively without exposing themselves to significant financial setbacks. By safeguarding cash flow, credit insurance ensures businesses can meet essential operational needs like payroll, rent, taxes, and subscription costs. It also provides the liquidity needed to handle unexpected expenses, such as legal fees in intellectual property disputes. This financial cushion allows companies to invest in long-term research and development, absorbing minor setbacks without threatening the overall stability of the business.

In short, credit insurance doesn’t just protect – it empowers companies to use credit strategically to fuel growth.

Growth Through Expanded Credit Lines

For tech companies, credit insurance is a vital tool for navigating volatile markets. It helps maintain revenue streams that could otherwise be lost due to risk-aversion or debt write-offs. Ingram Micro’s partnership with its insurer, which began in 2007, is a great example of how this works in practice. The company leverages its insurer’s extensive database and expertise to set credit levels for approximately 69,000 smaller accounts that aren’t directly covered by insurance policies.

"If we’re too protective and risk averse, then we will lose revenue and sales opportunities, yet too much focus on sales will inevitably result in increased trading risk and the potential for losses." – Frederic Wittemans, Director of Credit for Europe, Ingram Micro

This data-driven strategy enables tech companies to establish credit limits across their entire customer base, ensuring steady growth while managing risks effectively. By acting as an extension of the credit department, the insurer provides valuable business intelligence, simplifying decision-making and breaking down communication barriers.

While expanding credit lines is essential, efficient claims handling is equally important for managing risks over time.

Claims Processing and Monitoring

The effectiveness of claims processing improves significantly when the credit insurer operates as a partner rather than a detached service provider. At Ingram Micro, the insurer participates in management meetings, offering insights and an external perspective on credit management processes. This collaboration ensures a smooth flow of information and quicker credit decisions.

"The role that Atradius plays in our credit management processes cannot be underestimated. They have become almost an extension of our own business with no barriers to communication, decision-making or information." – Frederic Wittemans, Director of Credit for Europe, Ingram Micro

To maximize the benefits, tech companies should maintain open communication between their credit management teams, brokers, and insurers. By tapping into the combined expertise and databases of both parties, businesses can make well-informed decisions about credit levels, even for accounts that fall outside standard policy coverage.

Conclusion

The examples and insights shared above highlight how credit insurance plays a key role in maintaining stability and driving growth within the tech industry.

For tech companies navigating B2B risks, global markets, and rapid expansion, credit insurance serves as a safeguard against challenges like unpaid invoices and client bankruptcies. It ensures that critical expenses – like payroll, rent, taxes, and subscriptions – can still be met, even when payments are delayed.

Credit insurance also helps tech firms strike a balance between growth and risk. As Frederic Wittemans, Director of Credit for Europe at Ingram Micro, aptly put it:

"Within our business, credit management sits at the fulcrum of a ‘business balance’ with sales on one side and risk on the other."

This balance is essential. It prevents companies from missing opportunities due to excessive caution while avoiding losses from taking on too much risk.

Beyond just protection, credit insurance enables growth by providing financial stability. This stability supports key areas like research and development, intellectual property protection, and strategic acquisitions. Ingram Micro’s partnership with Atradius and broker Marsh is a great example of how credit insurance can support both strategic growth initiatives and effective risk management across a large customer base.

For tech companies expanding globally, entering new markets, or working with emerging startups, credit insurance offers more than just financial protection – it provides access to valuable business intelligence. Leveraging an insurer’s data and expertise allows companies to make smarter credit decisions across their entire customer portfolio, effectively enhancing their internal credit management capabilities.

Whether it’s securing cash flow during global expansion or increasing credit lines for fast-growing sectors, credit insurance is a vital tool in the financial playbook of tech companies. It not only protects revenue streams during uncertain times but also empowers businesses to take strategic risks, fueling innovation and growth in the ever-evolving tech landscape.

FAQs

What does credit insurance cover for tech invoices?

Credit insurance for tech invoices safeguards businesses against the risk of unpaid commercial debts. It generally provides coverage for situations like client insolvency or payment defaults, helping to minimize financial risks and maintain a steadier cash flow.

How does credit insurance help tech companies get better financing?

Credit insurance plays a crucial role in helping tech companies access better financing options. By boosting lender confidence in a company’s receivables and overall financial stability, it opens doors to higher credit limits and improved loan terms. This added layer of assurance not only helps businesses manage potential risks but also provides the financial flexibility needed to support growth initiatives.

Should a tech company choose multibuyer or single-buyer coverage?

A tech company deciding between multibuyer or single-buyer credit insurance should evaluate its customer base and overall risk strategy.

- Multibuyer coverage offers protection against payment defaults across a broad portfolio of customers, helping to distribute risk more evenly.

- Single-buyer coverage, on the other hand, is designed to secure revenue tied to a small number of critical clients.

The choice ultimately hinges on how concentrated the company’s customer base is and how this aligns with its broader credit risk management objectives.