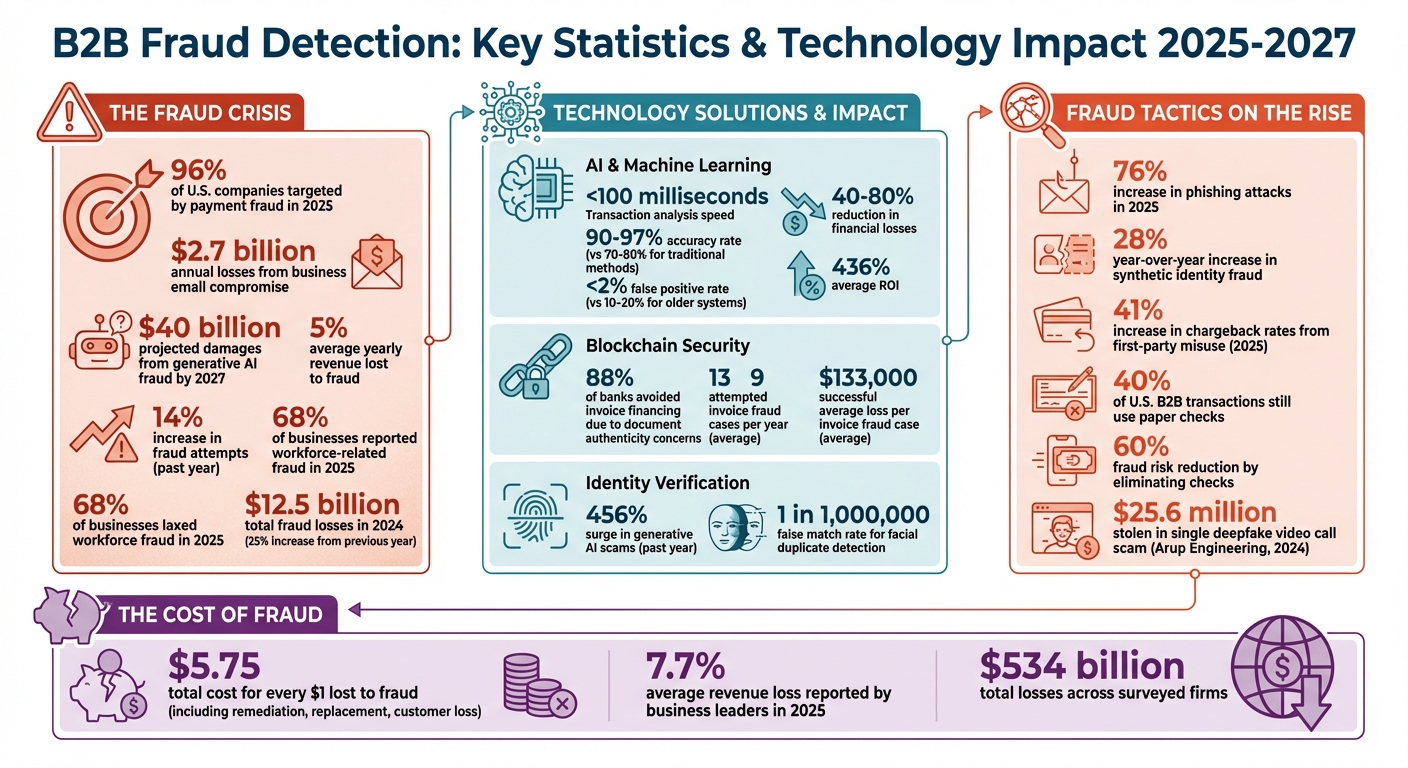

Fraud in B2B transactions is rising fast, with 96% of U.S. companies targeted by payment fraud in 2025. Losses from scams like business email compromise reached $2.7 billion annually, and generative AI fraud is projected to cause $40 billion in damages by 2027. Advanced fraud tactics, such as AI-driven schemes, deepfakes, and synthetic identity fraud, are becoming harder to detect.

Key takeaways:

- AI and machine learning now analyze transactions in under 100 milliseconds, reducing fraud by up to 80%.

- Blockchain improves data integrity, preventing invoice tampering and duplication.

- Identity verification systems combat deepfake scams and synthetic fraud with biometric checks and risk-based authentication.

- Fraud prevention requires multi-layered approaches, including employee training, dual approvals, and automated security tools.

Businesses must invest in real-time fraud detection, stronger internal controls, and collaborative efforts across industries to manage these threats effectively.

B2B Fraud Detection Statistics and Technology Impact 2025-2027

Fraud Prevention in Online B2B Transactions

sbb-itb-b840488

Fraud Detection Technologies in 2025

As fraud becomes more sophisticated, businesses are turning to advanced technologies to protect B2B transactions. Tools like AI, blockchain, and modern identity verification systems are reshaping how fraud is detected and prevented.

AI and Machine Learning for Real-Time Detection

AI-powered systems now evaluate B2B transactions and assign risk scores in less than 100 milliseconds, ensuring fraud is intercepted before payments are processed. This speed is critical since fraudsters operate in real time, exploiting even the smallest delays.

Behavioral AI plays a key role by analyzing spending habits, device fingerprints, and typing patterns to spot irregularities. For example, if a payment request comes from an unexpected location or a vendor suddenly updates their banking details, the system flags it immediately. Graph Neural Networks (GNNs) take this a step further by mapping relationships between accounts, IPs, and devices, exposing coordinated fraud rings and money laundering schemes that traditional methods often miss. Additionally, cross-system intelligence connects data from emails, ERP systems, procurement platforms, and financial tools to detect complex fraud methods like Business Email Compromise.

"AI has moved fraud detection from static defense to dynamic intelligence. It is no longer about reacting to fraud but anticipating it." – Krishna Kandi, Senior Software Engineer, Convoke

AI systems outperform traditional fraud detection, achieving 90-97% accuracy, compared to 70-80% for older rule-based methods. They also reduce false positives to under 2%, a significant improvement over the 10-20% rate of older systems. Financial losses from fraud can drop by 40-80% with AI, delivering an average ROI of 436%.

A newer approach, federated learning, allows businesses to train AI models on their own sensitive data while sharing anonymized updates with a central model. This method enhances collective learning without compromising privacy. Before fully implementing AI, companies can use a "shadow mode" to silently test the system’s accuracy and speed alongside existing rules. Risk-based friction is another strategy: low-risk transactions are approved automatically, while higher-risk ones trigger additional verification steps like Multi-Factor Authentication.

While AI handles real-time detection, blockchain technology ensures the integrity of transaction data.

Blockchain for Secure Transactions

Blockchain addresses a major trust issue in B2B transactions: 88% of banks have avoided invoice financing due to concerns about document authenticity. By creating an immutable ledger, blockchain ensures that invoices and transaction records cannot be altered, deleted, or duplicated once they’re recorded.

Each transaction is timestamped and assigned a unique digital fingerprint, making it easy to detect any attempts to tamper with or resubmit documents. This transparency eliminates the blind spots fraudsters often exploit. On average, finance teams face 13 attempted and 9 successful invoice fraud cases annually, with losses averaging $133,000 per case.

In January 2026, InvoiceMate demonstrated the power of combining blockchain and AI to secure invoice management. The platform, led by CEO Muhammad Salman Anjum, records every invoice on a blockchain ledger with unique digital fingerprints and timestamps. This approach gives financiers real-time visibility into an invoice’s journey and even enables tokenizing verified invoices into assets for secure financing.

"Blockchain enhances invoice security primarily through immutability, decentralization, and cryptography, which prevent fraud, ensure data integrity, and provide a transparent, unalterable audit trail of all transactions." – Muhammad Salman Anjum, CEO and Co-Founder, InvoiceMate

The trend for 2025 is clear: businesses are combining blockchain’s data integrity with AI’s real-time risk scoring to create more secure systems. Many are adopting "Know Your Invoice" (KYI) protocols, where blockchain verifies transaction details before approval. By integrating blockchain with encryption, multi-factor authentication, and automated monitoring tools, companies can build a robust security framework that flags irregularities for immediate review.

While blockchain secures data, advanced identity verification systems tackle fraud at the human level.

Authentication and Identity Verification Systems

Identity verification systems are now combating a 456% surge in generative AI scams over the past year. Machine learning tools can identify deepfakes and synthetic camera feeds during verification processes.

Facial duplicate detection is one such tool, cataloging faces to spot repeat fraudsters or mule accounts, even when IDs are tampered with. This system boasts a false match rate of just 1 in 1,000,000. Biometric age estimation further enhances security by flagging discrepancies between a person’s appearance, stated age, and ID during live verification.

"New generative AI models now pop up almost every week, and even unsophisticated fraudsters use them to generate convincing ID verification sessions at scale." – Danica Kleint, Product Marketing Manager, Plaid

Biometric and behavioral checks complement transaction risk scores to verify user identity. Risk-based authentication adjusts the verification process dynamically: trusted users face minimal friction, while high-risk cases undergo additional scrutiny. Selfie re-authentication adds another layer of protection by comparing a fresh selfie to previously stored data, ensuring returning users are legitimate, especially during account recovery or high-risk logins.

Behavioral biometrics and device fingerprinting further distinguish legitimate users from bots or fraudsters by analyzing IP addresses, browser details, device IDs, and behavioral patterns. Automated vendor account validation replaces manual callbacks by cross-checking company IDs, bank accounts, and ownership details to prevent impersonation and reduce errors.

To strengthen fraud prevention, businesses are deploying multi-layered MFA systems that include biometrics, device fingerprinting, and behavioral authentication. Automated tools now verify banking detail changes, replacing outdated manual procedures. Businesses can also set automated spending limits, flag unusual transaction volumes, and conduct regular penetration testing to evaluate defenses against social engineering and deepfake attacks. Together, these measures secure the human element in B2B transactions and bolster fraud prevention efforts.

New Fraud Tactics and Prevention Methods

Fraud is an expensive problem. On average, companies lose 5% of their yearly revenue to it, with fraud attempts climbing 14% in the past year alone. Understanding these evolving tactics – and how to counter them – is crucial for safeguarding B2B transactions. The methods explored here highlight the importance of leveraging advanced tools and strategies.

Synthetic Identity Fraud

This type of fraud is particularly tricky to detect. Fraudsters blend real Social Security Numbers (SSNs) with fake details to create identities that appear legitimate over time. Once they’ve built credible credit histories, they max out credit lines and disappear – a process known as a "bust-out". A newer twist involves "expat identity packages", where fraudsters buy the identities of former legal immigrants who have left the U.S. These packages, sold on international Telegram channels, include SSNs, tax forms, and even credit reports.

To combat this, businesses can use behavioral analytics and link analysis to track connections between accounts, devices, and IP addresses. Regularly updating credit reports for existing B2B partners can help spot red flags like sudden spikes in credit usage or plummeting credit scores. Automated decision-making tools can also block applications with fake trade references or mismatched identity details before they even enter your system.

Business Email Compromise and Social Engineering

Business Email Compromise (BEC) schemes have become more sophisticated, moving beyond simple email spoofing to include AI-powered tools like voice cloning and deepfakes. In early 2024, an employee at Arup Engineering’s Hong Kong office fell victim to a deepfake video call featuring AI-generated versions of senior executives. Following the fake instructions, they authorized $25.6 million in transfers across five bank accounts.

Phishing has also surged, with attacks increasing by 76% in 2025. Generative AI now enables attackers to craft highly convincing emails that bypass traditional defenses. AI voice cloning, which can mimic someone’s voice with just 3 seconds of audio, has also been used in schemes originating on consumer apps like WhatsApp, which often lack corporate IT oversight. For example, in 2024, a scammer used an AI-generated voice to impersonate Ferrari’s CEO, requesting transfers that were only stopped after a verification process revealed inconsistencies.

"AI-enhanced BEC attacks succeed when organizations trust identity signals from a single channel. Reliable defense comes from process controls: out-of-band verification, dual approval gates, and strict exception governance."

– Nandor Katai, Valydex

To counter these threats, businesses should implement robust process controls. For instance, callback protocols can require employees to confirm requests using a pre-approved phone number rather than relying on contact details provided in suspicious messages. Dual authorization – where one person initiates a transfer and another independently approves it – adds another layer of security. Moving financial approvals to corporate-controlled platforms like Microsoft Teams or Slack allows IT teams to enforce multi-factor authentication and keep audit logs. Employee training is also essential. In one instance involving LastPass in 2024, an employee recognized "artificial urgency" and the unusual use of WhatsApp in AI-generated voicemails impersonating CEO Karim Toubba, preventing a scam. Regular simulations can help employees practice spotting and responding to these tactics.

Insider Threats and Collusion

Not all threats come from outside the organization. Internal vulnerabilities are just as dangerous. In 2025, 68% of businesses reported workforce-related fraud, with employee impersonation being the most common issue. With generative AI, fraudsters can now create fake employees, payroll entries, and receipts. They also use autonomous AI agents to analyze social media data and build psychological profiles of targets, enabling highly tailored social engineering attacks without direct human involvement.

To address these risks, companies need strong internal controls. Segregating duties ensures no single employee has full control over financial transactions. Regular audits of user access rights and transaction logs can catch irregularities. Monitoring payroll changes and cross-checking vendor addresses against employee records can uncover potential collusion. Additionally, lifestyle changes among employees with financial access – like sudden, unexplained wealth – may signal fraudulent activity.

Even traditional payment methods like paper checks pose risks. Despite the shift to digital payments, checks still account for 40% of U.S. B2B transactions. Eliminating checks could cut a company’s fraud risk by as much as 60%. Switching to ACH or real-time payments reduces vulnerabilities tied to physical mail and manual processing.

"A lot of fraud is in the checks. If you cut out checks, you cut 60% of fraud right there."

– Ernest Rolfson, Founder and CEO, Finexio

Regulations and Industry Collaboration

Regulatory Requirements for Fraud Prevention

In 2025, the regulatory framework took a sharp turn, introducing new obligations to combat fraud. One major change came in March 2025 when FinCEN adjusted the Corporate Transparency Act (CTA), narrowing the scope of Beneficial Ownership Information (BOI) reporting. Domestic companies were exempted from filing these reports, while foreign-owned entities remained obligated – targeting international money laundering risks more directly. This shift prioritizes enforcement on high-risk foreign entities.

By January 1, 2026, SEC-registered investment advisers must implement comprehensive anti-money laundering (AML) and counter-terrorist financing (CFT) programs, along with filing Suspicious Activity Reports (SARs). Meanwhile, the Office of Foreign Assets Control (OFAC) now mandates a 10-year record retention policy for sanctions-related documents. OFAC has made it clear: "Lack of familiarity with sanctions is no defense". To stay compliant, businesses are encouraged to check OFAC’s "Recent Actions" page daily, as geopolitical sanctions continue to evolve.

Enforcement actions in recent years highlight the seriousness of non-compliance. In October 2024, FinCEN fined TD Bank $1.3 billion, the Federal Reserve penalized Silvergate Bank $43 million, and the Office of the Comptroller of the Currency issued a cease-and-desist order against Bank of America. Fraud also took a heavy toll on businesses, with leaders reporting an average revenue loss of 7.7% in 2025 – adding up to $534 billion across surveyed firms.

The GENIUS Act, passed in July 2025, introduced strict oversight for stablecoin issuers, requiring 1:1 reserves and compliance with the Bank Secrecy Act to address money laundering and enhance consumer protections. Additionally, two executive orders reshaped federal payment systems: EO 14249 requires Treasury approval for all federal disbursements, and EO 14247 mandates a shift away from paper-based payments to curb fraud and waste. FinCEN also introduced new requirements for money services businesses along the southwest U.S. border, demanding reporting and record retention for transactions between $200 and $10,000.

These regulatory updates have laid the groundwork for stronger collaboration across industries.

Partnerships Between Financial Institutions and Businesses

Regulatory changes have been matched by a surge in industry partnerships aimed at tackling fraud. In February 2026, the SBA Inspector General and USDA Inspector General formalized a data-sharing agreement to improve fraud detection in federal programs. William W. Kirk, Inspector General at the SBA, explained:

"Fraud schemes move quickly, and our oversight approach has to move faster. This agreement strengthens our ability to share information, identify fraud indicators earlier, and support the law enforcement partners who are holding bad actors accountable".

Real-time data-sharing platforms are now a cornerstone of these efforts. These systems allow financial institutions to verify invoices and trade documents instantly, reducing the risk of duplicate financing. This is especially critical as 89% of invoice factoring professionals reported a rise in fraudulent activity during 2024–2025. Privacy-preserving technologies, such as confidential computing and secure cloud infrastructures, ensure data can be shared securely without compromising customer confidentiality.

Standardization initiatives, like the International Chamber of Commerce‘s Digital Standards Initiative, further streamline these efforts by enabling quick cross-referencing of data across financial systems. Jialing Chia, Managing Director at MonetaGo, underscores the importance of this approach:

"A unified approach is not merely desirable, but essential for sustained integrity, resilience, and growth of the invoice factoring market and trade globally".

Shared databases containing negative-file information also help identify synthetic identities and unusual patterns that individual organizations might miss. These tools are proving vital for fraud detection in B2B payments.

In January 2026, the Division for National Fraud Enforcement was established to centralize efforts in investigating fraud affecting both public and private sectors. This division enhances coordination between government agencies and private businesses, emphasizing collective intelligence. Steve D’Antuono, a Partner at KPMG, highlights the necessity of this shift:

"Fragmented efforts are no longer sufficient in a world where fraud evolves faster than policy".

With fraud losses reaching $12.5 billion in 2024 – a 25% increase from the previous year – and projections suggesting generative AI could drive losses up to $40 billion in the U.S. by 2027, collaboration has moved from being a helpful strategy to an absolute necessity for combating fraud effectively.

Conclusion: Improving Fraud Detection in B2B Transactions

Action Steps for Businesses

To tackle fraud effectively, businesses need to embrace smarter tools and strategies. Automated fraud detection is no longer optional. By 2025, industry leaders reduced manual review rates to just 2.7%, showing that AI-driven decision-making is essential to stay ahead of emerging threats. Multi-layer authentication – using biometric verification, device fingerprinting, and behavioral analytics – should be standard for high-value transactions. Additionally, setting transaction thresholds that require secondary approvals through out-of-band verification can add another layer of security.

Data hygiene plays a huge role in fraud prevention. Keeping internal records clean and integrating data across departments like sales, finance, and cybersecurity can close gaps that fraudsters might exploit. With 96% of U.S. companies reporting payment fraud attempts and business email scams causing over $2.7 billion in annual corporate losses, fragmented systems are a risk businesses can’t afford. Real-time risk scoring systems are also critical, as instant payment systems leave little to no time for manual checks.

Vendor verification is another area that demands attention. Before bringing on new suppliers, businesses should cross-check credit reports, verify Tax IDs, and confirm physical addresses to avoid falling victim to business identity theft. Bill James, Director of Enterprise Sales and Strategy at Creditsafe, highlights the urgency of staying vigilant:

"Unfortunately, as our capabilities and technology evolve, so does theirs. With things like AI, they can upload a script into a website and do a lot of damage very quickly".

Regular security audits and employee training are essential to combat deepfakes and social engineering attacks. Combining AI, blockchain technology, and multi-layer authentication can create a robust fraud prevention framework that keeps businesses one step ahead.

While these measures address today’s challenges, the future will demand even more innovative approaches.

The Future of B2B Fraud Detection

The fight against fraud is only going to get tougher. By 2027, generative AI is expected to drive $40 billion in fraud losses. Synthetic identity fraud has already seen a 28% year-over-year increase, and first-party misuse pushed chargeback rates up by 41% in 2025. For U.S. financial services firms, every $1 lost to fraud results in a total cost of $5.75 when factoring in remediation, replacement, and customer loss.

Future defenses will rely heavily on AI to counter increasingly sophisticated scams. As fraudsters leverage machine learning to mimic legitimate behaviors, businesses must deploy advanced detection tools to outmatch them. Blockchain analytics will likely become standard for tracking cryptocurrency transactions and spotting suspicious wallets in real time. Shared intelligence networks – where businesses collaborate to identify bad actors and fraudulent patterns – will move from being a competitive advantage to an essential survival tool. Paul Tucker, Chief Information Security and Privacy Officer at BOK Financial, underscores the stakes:

"One of the biggest challenges in our industry is that, while we’re implementing AI into our systems to better protect them, scammers are using the same tools to defraud businesses, making it critical to understand what we’re up against".

To stay ahead, businesses must invest in adaptive, integrated protection strategies. A combination of automation, real-time monitoring, thorough employee training, and collaborative efforts across industries will be key to countering fraudsters’ evolving tactics in an increasingly complex threat landscape.

FAQs

What should we implement first to reduce B2B payment fraud fast?

To cut down on B2B payment fraud quickly, focus on integrating AI-driven fraud detection tools and real-time transaction monitoring into your processes. These technologies excel at spotting unusual activity and stopping fraudulent transactions before they cause damage.

How can we stop fake vendor bank-detail change requests (BEC scams)?

To guard against fake vendor bank detail change requests and business email compromise (BEC) scams, it’s crucial to implement a multi-layered verification process. For example, whenever you receive unexpected payment requests or notifications about changes to a vendor’s bank account, confirm them using a trusted communication method. A good practice is to call the vendor directly using pre-established contact information, not details provided in the suspicious request.

Additionally, keep a close eye on vendor credentials and payment instructions. Regularly monitoring for unusual activity or inconsistencies can help you spot red flags early. Taking these precautionary steps can go a long way in minimizing the chances of falling victim to these scams.

How does credit insurance help when fraud still causes non-payment?

Credit insurance helps shield businesses from the financial blow of non-payment caused by fraud. If a customer defaults or becomes insolvent, this coverage steps in to absorb the loss. By providing this safety net, businesses can recover funds and keep their cash flow steady, even when fraud catches them off guard.