Ultimate Guide to Underwriter-Broker Collaboration

How brokers and underwriters collaborate to protect receivables, set credit limits, manage claims, and improve financing with clear communication and data tools.

How brokers and underwriters collaborate to protect receivables, set credit limits, manage claims, and improve financing with clear communication and data tools.

Predictive analytics uses internal and external data to spot defaults up to 12 months early, cut bad debt, and tailor credit insurance.

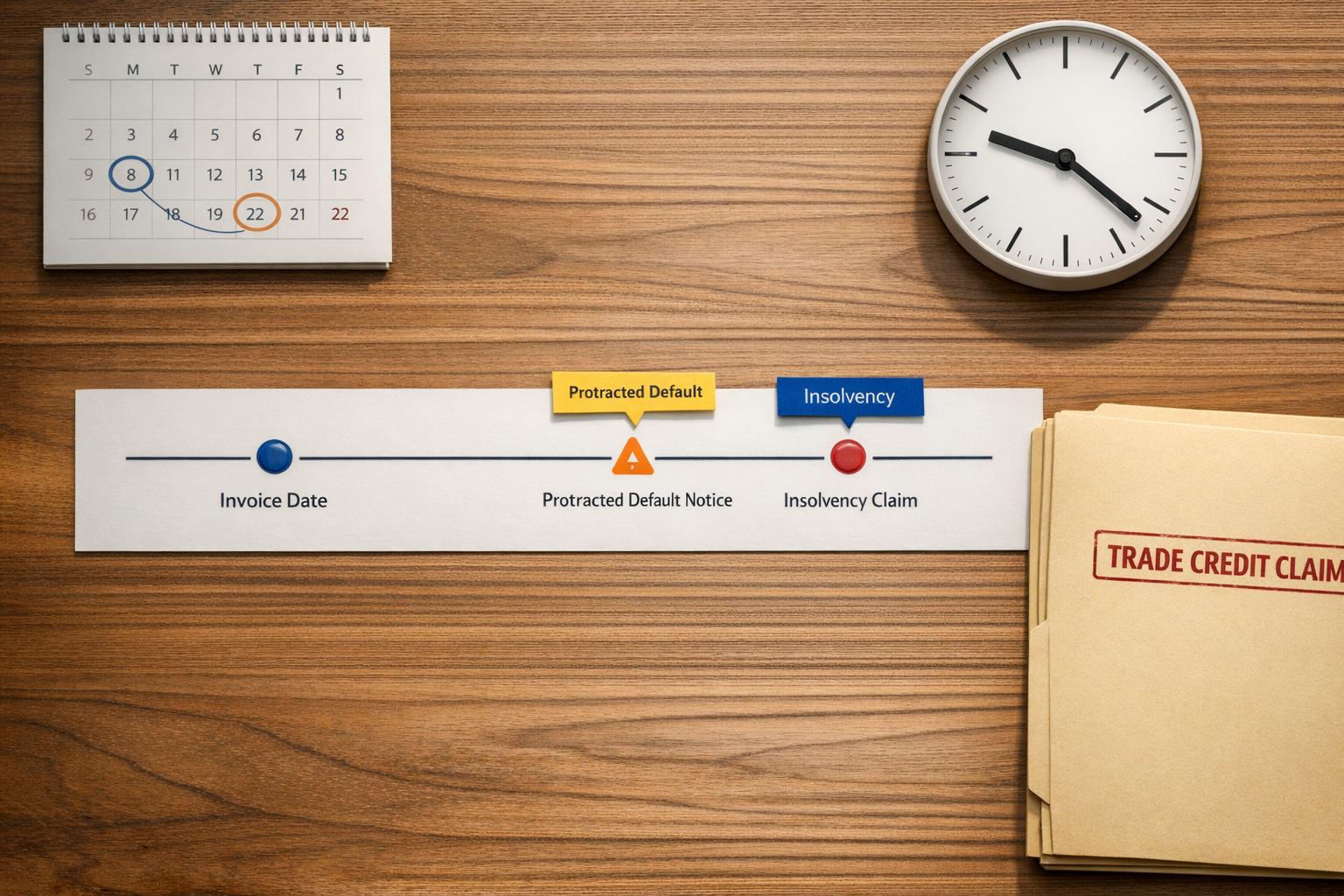

When to notify insurers of trade credit claims: deadlines by claim type (insolvency, protracted default), required documents, and steps to avoid denials.

Undiversified credit portfolios magnify borrower, sector, and regional shocks; diversification and credit insurance cut tail losses and ease capital pressure.

How to build fair, transparent credit models: bias testing, explainable AI, data privacy (machine unlearning), audits, and regulatory compliance for lenders.

Protect B2B sellers from unpaid invoices—credit insurance covers insolvency, defaults and political risks, reimbursing up to 90–95% while stabilizing cash flow.