Managing overdue invoices can be a major challenge for businesses. Late payments disrupt cash flow, threaten operations, and increase the risk of bad debt. Credit insurance offers a solution by protecting businesses from financial losses when customers fail to pay. It covers two key risks: insolvency (bankruptcy) and protracted default (persistent late payments). Policies typically reimburse 80–95% of unpaid invoices, helping businesses stabilize cash flow and reduce write-offs.

Key takeaways:

- Receivables aging: Tracks unpaid invoices by time overdue (e.g., 0–30 days, 31–60 days). Aging reports highlight high-risk accounts and cash flow issues.

- Credit insurance benefits: Covers unpaid invoices, reduces bad debt reserves, and ensures financial stability. Insured receivables also improve borrowing terms.

- Proactive management: Use aging reports to identify risky accounts and align insurance policies with customer payment habits.

This approach not only protects your business but also supports growth by enabling confident credit decisions and better financial planning.

Trade Credit Insurance Explained: Safeguard Your Business from Payment Risks

sbb-itb-b840488

Receivables Aging and Its Challenges

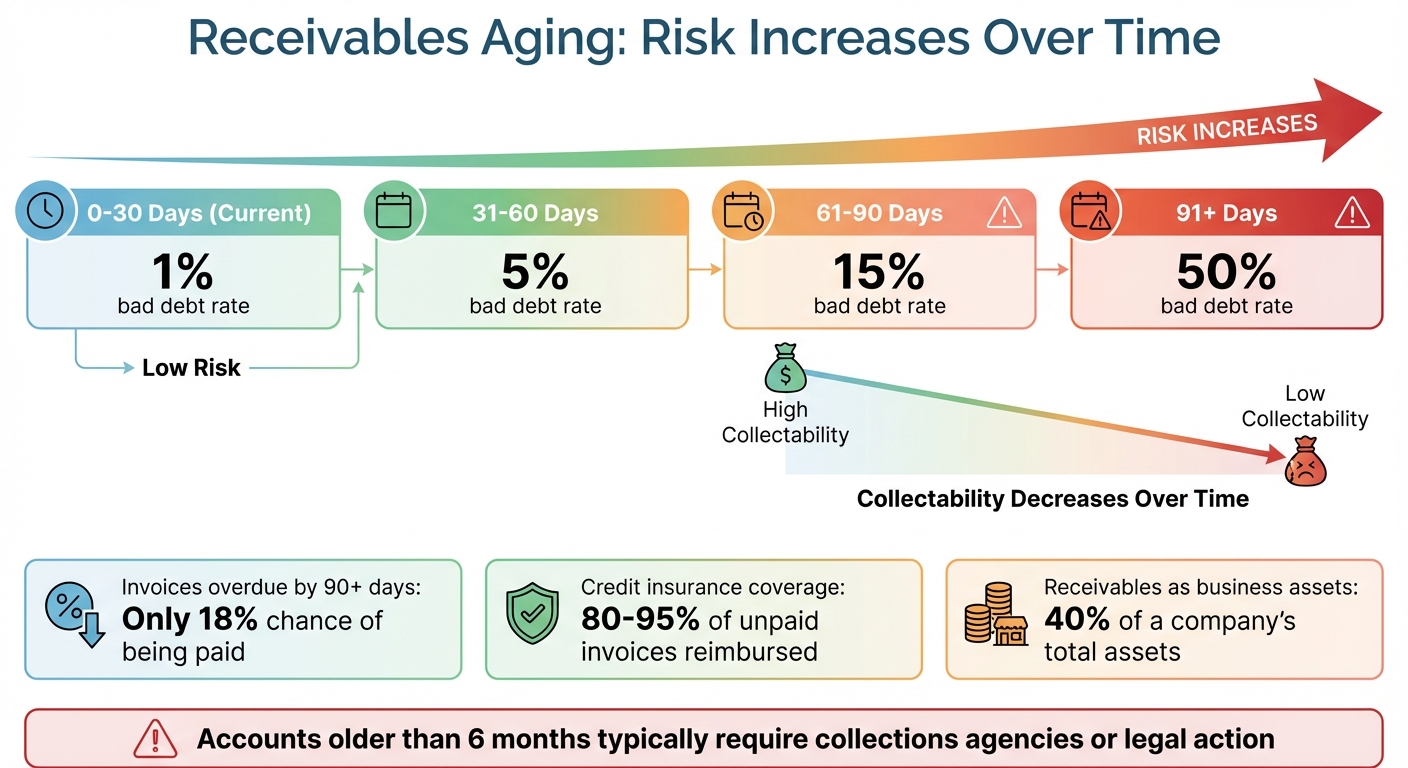

Receivables Aging Buckets and Default Risk Rates

What Is Receivables Aging?

Receivables aging is a report that organizes a company’s unpaid invoices by the length of time they’ve been outstanding. It breaks down unpaid invoices into 30-day intervals, often referred to as "buckets": 0–30 days (current), 31–60 days, 61–90 days, and over 90 days. This system makes it easy to spot which customers are paying on time and which are falling behind. It also helps businesses estimate their "allowance for doubtful accounts", ensuring their financial statements reflect potential losses from unpaid debts.

Risks in Receivables Aging

The longer invoices remain unpaid, the harder they are to collect. Overdue invoices are a growing risk, and accounts older than six months are often only recoverable through collections agencies or legal action. To prepare for these risks, companies assign default probabilities to each aging bucket – for instance, a 1% bad debt rate for invoices 0–30 days old, but 15% for those overdue by 61 days or more.

Beyond collection risks, overdue invoices can disrupt cash flow, making it harder to cover payroll, replenish inventory, or fund daily operations. Persistent overdue balances may even signal that a customer is experiencing severe financial trouble, which can indicate deeper risks.

Key Metrics in Receivables Aging

Two key metrics help businesses monitor and manage receivables aging:

- Days Sales Outstanding (DSO): This measures the average time it takes to collect payment after a sale. A high DSO could mean it’s time to tighten credit terms or improve collection strategies.

- Collection Effectiveness Index (CEI): This metric shows how well a company is collecting payments compared to the total owed.

As Jamilex Gotay, Senior Editorial Associate at NACM, explains, aging buckets "serve as a tool for risk mitigation. They reveal where cash flow is slowing, pressure is building or risk is emerging".

How Credit Insurance Works With Receivables Aging

Protection Against Non-Payment and Insolvency

Credit insurance acts as a safety net when customers fail to pay their invoices. It primarily covers two scenarios: customer insolvency (when a customer declares bankruptcy) and protracted default (when a customer consistently delays payments beyond agreed terms). For instance, if a customer repeatedly misses deadlines, this could activate your coverage.

When you file a claim, insurers typically reimburse between 80% and 90% of the unpaid invoice amount. For example, if a $50,000 invoice remains unpaid because of a customer’s bankruptcy, you could recover $40,000 to $45,000, depending on your policy. This ensures that the financial burden doesn’t fall entirely on your business and helps maintain your balance sheet. With this protection in place, aging reports become a valuable tool for identifying high-risk accounts.

Finding High-Risk Accounts Through Aging Reports

Aging reports provide a snapshot of overdue accounts, helping you identify which ones require insurance coverage the most. If your monthly report shows invoices accumulating in the 61–90 day or over 90-day categories, it’s a clear sign of potential payment problems. Insurers rely on this data to evaluate creditworthiness and set appropriate credit limits. Persistent warning signs in these reports often lead to adjustments in coverage limits to better manage risk.

As Allianz Trade explains, "Trade credit insurance complements the insights gained from the aging report and enhancing overall credit risk management".

This proactive approach doesn’t just highlight risks – it also helps reduce financial losses.

Reducing Write-Offs and Improving Financial Stability

Credit insurance significantly reduces the need to set aside large reserves for doubtful accounts. By covering 80% to 90% of unpaid invoices, it ensures more stable cash flow and protects your working capital. This is especially crucial since invoices overdue by more than 90 days have only an 18% chance of being paid. Recovering a portion of these aging invoices through insurance minimizes the impact of write-offs, strengthens your financial stability, and can even improve your borrowing terms. These benefits make credit insurance an essential part of a well-rounded receivables aging strategy.

Steps to Integrate Credit Insurance With Receivables Aging

Determining Coverage Needs Using Aging Data

Aging reports are a goldmine for pinpointing where your insurance coverage should focus. Take a close look at which accounts regularly land in the 61–90 day and 91+ day buckets, as these represent the highest risk. Applying standard uncollectible rates – 1% (<30 days), 5% (31–60 days), 15% (61–90 days), and 50% (91+ days) – can help you calculate the insurance limit needed to safeguard your balance sheet.

Be particularly mindful of concentration risk. If a significant share of your receivables is tied to just a few customers or a single industry, and these balances often end up in late-payment categories, consider requesting "named buyer" coverage for those specific accounts.

Michelle Kelly, Senior Credit Manager at Mansfield Energy, explains: "Aging buckets, in conjunction with other ways in reviewing the aging, will capture the higher risk accounts quicker to mitigate the exposure".

By focusing on these high-risk accounts, you can address the elevated default rates revealed in your aging reports. Once you’ve identified your coverage needs, the next step is to align policy terms with your credit conditions.

Matching Insurance Policies With Credit Terms

With your exposure mapped out, it’s time to ensure your insurance policy aligns with your customers’ payment habits. For example, if your aging reports show that customers in industries like construction often pay within 45–65 days, your policy’s maximum extension period should reflect this instead of defaulting to a standard 30-day window. Set aging intervals (0-30, 31-60, 61-90, and 91+ days) that are in sync with your payment terms, whether those are Net 30 or Net 45.

If you notice that more than 10–15% of your invoices are overdue by 60 days or more, tighten your credit policies before insuring the remaining balance.

Aaron Dyer, Business Banking Regional Manager at City National Bank, highlights: "The financials and accounts receivable aging report are an important piece of weekly management for the business".

Customizing your policy terms in this way helps streamline monitoring and ensures timely claims processing.

Monitoring and Filing Claims on Insured Receivables

Weekly tracking of aging reports is crucial for spotting accounts nearing the 150-day past-due mark. This is important because most insurers require claims for protracted default to be filed within 180 days of the invoice date. For insolvency situations, such as Chapter 11 filings, the window is even tighter – typically just 10 to 20 days after notification.

Keep all essential documents in a centralized repository to avoid scrambling when filing claims.

Kirk Elken, Co-founder of Securitas Global Risk Solutions, cautions: "One of the non-negotiables for the insurer is late filing a claim (missing the window to file the claim)".

Make sure to document all collection efforts in the notes section of your aging report, as insurers often require proof that you’ve exhausted internal collection methods before approving a claim for protracted default. If a debtor is making partial payments but your claim deadline is approaching, request a filing extension from your insurer. This preserves your rights while giving the debtor more time to resolve the balance.

Benefits of Credit Insurance for Receivables Aging

Credit insurance offers a range of benefits that not only safeguard your business but also create opportunities for growth and financial stability.

Better Risk Management

One of the key advantages of credit insurance is its ability to protect your business from the financial strain caused by overdue invoices. By covering a large percentage of unpaid balances – whether due to insolvency or prolonged delays – it helps maintain your cash flow, even in challenging situations. For instance, if a customer consistently pays 60 days late on Net 30 terms, this insurance ensures your operations remain unaffected by such delays.

Additionally, credit insurance minimizes the need to set aside excessive reserves for bad debt. This frees up capital that would otherwise be tied to high-risk receivables. For businesses involved in international trade, the coverage extends to risks beyond the buyer’s control, such as currency fluctuations, political instability, trade sanctions, or embargoes. These factors, which could otherwise disrupt payments and inflate aging receivables, are effectively managed under the protection of credit insurance.

More Confident Credit Decisions

Credit insurance also supports better credit decision-making by providing external credit assessments. This allows you to onboard buyers with limited credit histories while offering extended payment terms without the usual concerns about non-payment. For example, your insurer can evaluate a buyer’s financial health and assign a credit limit, giving you the confidence to proceed with new business opportunities.

With this added protection, you can offer more attractive terms to your customers, such as extending payment schedules from Net 30 to Net 45 or even Net 60. These extended terms can encourage buyers to place larger orders, helping you reduce inventory costs and strengthen your position with suppliers. And the cost? Typically, it’s a small fraction of your sales volume, making it a cost-effective way to grow your customer base.

Supporting Business Growth and Financing

Credit insurance also enhances your ability to secure financing. Lenders view insured receivables as high-quality collateral, which can lead to better borrowing terms and higher credit limits. This improved access to working capital is especially valuable when scaling operations or entering new markets.

"By protecting your own company’s interests with a comprehensive credit insurance policy, you are guaranteeing the ability of your business to continue high levels of production, sales and profitability despite your customers’ difficulties", says 1st Commercial Credit.

This layer of security also opens doors to market expansion. Whether you’re exploring regions with economic instability or industries known for cyclical downturns, credit insurance provides the safety net needed to take calculated risks. By enabling growth into previously untapped markets and strengthening relationships with lenders, credit insurance helps establish a solid financial foundation that supports long-term success.

Conclusion

Managing receivables aging effectively is a key step in safeguarding your cash flow against non-payment risks. By pairing this process with credit insurance, businesses can transform aging reports into proactive tools for risk management. For instance, when an invoice shifts from the 61-90 day bracket to the critical 90+ day category – where the likelihood of collection drops to just 18% – credit insurance ensures that your cash flow remains secure, even in the face of defaults. This method aligns seamlessly with earlier strategies aimed at reducing receivables risk.

The numbers speak for themselves. Receivables often account for 40% of a company’s assets, making their protection crucial for financial stability. In a business with a 5% profit margin, a $100,000 loss due to unpaid invoices would require $2 million in new sales to recover the lost profit. This is why focusing on prevention through credit insurance is far more effective than attempting to recover losses after the fact.

Industry leaders emphasize how this integration strengthens risk management practices.

"Trade credit insurance… provides a safety net for receivables that are overdue or at risk of non-payment, thereby complementing the insights gained from the aging report and enhancing overall credit risk management", says Allianz Trade.

FAQs

When should I insure a customer based on aging buckets?

When a customer’s receivables start falling into aging buckets – like 31–60 days or over 60 days – it’s a good time to consider insurance. This becomes even more crucial if the customer has a track record of late payments or delinquency. Credit insurance can safeguard your business by protecting against non-payment, helping to reduce credit risk and maintain your financial stability.

What triggers a claim for protracted default vs insolvency?

When a customer does not pay an undisputed invoice within the agreed timeframe but hasn’t declared insolvency, it’s referred to as a protracted default claim. On the other hand, an insolvency claim comes into play when a customer enters formal legal proceedings, like bankruptcy. Both types of claims are designed to shield businesses from the financial strain of unpaid receivables.

How does credit insurance help me get better borrowing terms?

Credit insurance can make borrowing more accessible and affordable by reducing the risk for lenders. With this added security, lenders may feel more confident offering you better terms, such as increased borrowing limits, reduced collateral demands, or even lower interest rates. By safeguarding your receivables, credit insurance strengthens your financial profile, giving lenders greater trust in your ability to manage obligations.