Credit insurance protects businesses from the risk of unpaid invoices when selling on credit terms. If a key customer defaults, declares bankruptcy, or faces political disruptions, credit insurance reimburses up to 90%-95% of the invoice value. This makes it a critical tool for managing cash flow, reducing financial risks, and enabling growth in new markets.

Here’s a quick breakdown of how it works:

- Coverage: Protects against insolvency, late payments, and political risks.

- Cost: Typically under 1% of insured sales volume.

- Application: Requires buyer credit checks and approval of credit limits.

- Claims: Must be filed within specific timeframes with detailed documentation.

- Benefits: Stabilizes cash flow, supports financing, and facilitates expansion.

For businesses engaged in B2B sales, credit insurance not only safeguards against losses but also provides confidence to extend credit terms to new or international customers. With insurers handling credit checks and debt recovery, it’s a practical way to manage risk while focusing on growth.

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

sbb-itb-b840488

How Credit Insurance Works

How Credit Insurance Works: 3-Step Process for B2B Businesses

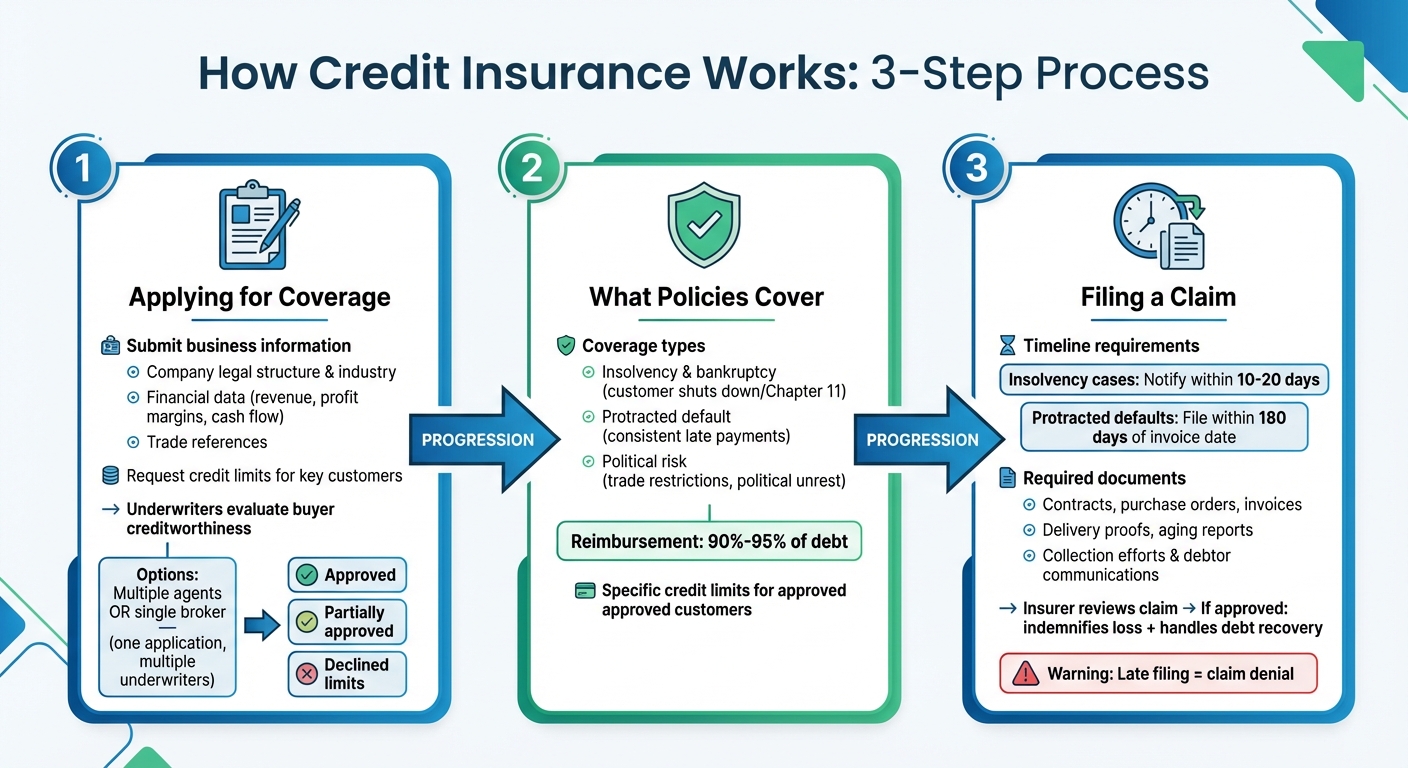

Understanding how credit insurance operates can help you decide if it aligns with your business needs. The process involves three main steps: applying for coverage, understanding what policies cover, and filing claims.

Applying for Coverage

The first step is submitting detailed information about your business and customers. This includes your company’s legal structure, industry, years in operation, financial data (like annual revenue, profit margins, and cash flow), and trade references. You’ll also need to request specific credit limits for key customers.

Underwriters will evaluate these buyers’ financial stability and creditworthiness to decide whether to approve, partially approve, or decline your requested limits. As Kirk Elken, Co-founder of Securitas Global Risk Solutions, explains:

"One market may fully approve the credit limit request, while another will only partially approve or even decline often due to lack of updated information."

You have two options for submitting applications: either work with multiple insurance agents, each applying to different carriers like Allianz Trade, Atradius, or Coface, or simplify the process by using a single broker. A broker can submit one application to access multiple underwriters, serving as your single point of contact at no extra cost.

Once your application is reviewed, it’s important to understand the types of risks your policy will cover.

What Policies Cover

Credit insurance shields your business from several payment risks. For example, insolvency and bankruptcy coverage kicks in when a customer shuts down or files for Chapter 11, leaving unpaid invoices. Protracted default coverage helps when a customer consistently delays payments – such as paying 60 days late on 30-day terms – causing disruptions to your cash flow.

If you’re a B2B exporter, political risk coverage can protect you from losses due to geopolitical challenges like trade restrictions, political unrest, or frozen payments. Most policies reimburse 90%–95% of the debt, meaning you’ll still bear a small portion of the loss.

Each policy includes specific credit limits for approved customers, and losses are covered up to these limits if a customer fails to pay. If non-payment occurs, the claims process comes into play.

Filing a Claim

If a customer doesn’t pay, act fast. Notify your insurer within 10–20 days for insolvency-related cases and file claims for protracted defaults within 180 days of the invoice date (or 150 days past due on 30-day terms).

Your claim should include key documents like contracts, purchase orders, invoices, delivery proofs, aging reports, collection efforts, and any communications with the debtor. As Kirk Elken highlights:

"One of the non-negotiables for the insurer is late filing a claim (missing the window to file the claim)."

After you’ve submitted your claim, the insurer will review it to ensure it meets the policy terms. If approved, they’ll indemnify the loss and take over the debt recovery process. However, insurers typically won’t pay out if the customer disputes the invoice until the dispute is legally resolved – they don’t mediate disagreements.

This structured approach makes credit insurance a reliable way to reduce credit risk in B2B dealings.

Key Features of Credit Insurance Policies

Coverage Limits and Premium Calculations

Credit insurance policies hinge on assessing the financial health of your buyers. Insurers determine credit limits for each buyer by evaluating their financial statements, payment history, and the stability of their industry. When you request coverage for a customer, this process includes reviewing public records and trade databases to gauge creditworthiness. For export-related transactions, additional factors like the buyer’s location and country-specific risks come into play.

Many policies offer a flexible limit feature, allowing you to independently approve smaller accounts as long as they meet the insurer’s pre-set criteria. This streamlines low-value transactions, while higher-value accounts remain under the insurer’s direct oversight.

Premium costs for credit insurance are typically less than 1% of your annual sales, often ranging from 0.05% to 0.6%. These rates depend on factors such as the risk level of your industry, the composition of your customer portfolio, and your claims history. For instance, a company generating $20 million in annual sales would likely pay under $50,000 for coverage. Most premiums are calculated based on total sales turnover, but some insurers offer pricing options tailored to specific high-value accounts.

These elements provide the framework for understanding how credit insurance policies operate over their term and renewal cycles.

Policy Duration and Renewal Process

Credit insurance policies generally last for 12 months, ensuring continuous coverage throughout the term. During this period, insurers actively monitor the financial health of your buyers and make necessary adjustments to credit limits. At the end of the term, the renewal process incorporates updated data on your sales and any claims history, ensuring the policy aligns with your current business needs.

Plan Types Compared

Credit insurance policies are designed to address a variety of business models and risk profiles. Here’s a comparison of common plan types and their features:

| Plan Type | Pricing Method | Coverage Scope | Best For |

|---|---|---|---|

| Whole Turnover | Based on a percentage of total sales | Covers all buyers meeting criteria | Businesses with high sales volume and many customers |

| Partial Turnover | Percentage of a specific sales segment | Covers a selected portion of sales | Companies focusing on key customer segments |

| Single-Buyer | Individual buyer’s credit limit | Covers one high-risk or essential buyer | Businesses with critical or new accounts |

| Top-Up Policy | Additional premium for extra coverage | Extends coverage beyond standard limits | Filling gaps in primary coverage limits |

The International Credit Insurance & Surety Association explains:

"The granted credit limit… is the maximum insured cover for a specific buyer and the policyholders can trade on an insured basis within the approved credit limit throughout the policy period."

This means that once a credit limit is approved, you can confidently conduct transactions up to that amount without needing to reapply for coverage on each sale.

Using Credit Insurance in Daily B2B Operations

Checking Buyer Credit Before Sales

Credit insurers take on the task of assessing buyer creditworthiness, saving you from conducting time-consuming and expensive internal investigations. When you’re considering offering credit terms to a new buyer, the insurer evaluates factors like sales volume, industry trends, repayment terms, and payment history to determine a credit limit. For instance, if a $120,000 limit is approved for a buyer, your policy will cover losses up to that amount.

Many policies also include a discretionary credit limit feature, allowing you to approve smaller accounts or transactions in certain countries without waiting for the insurer’s approval. Valarie Hardesty, Director of Credit at Elevate Textiles, Inc., uses this flexibility for international sales. She relies on these limits based on the risk profile of the buyer’s country. For larger or riskier accounts, she applies for a Special Buyer’s Credit Limit (SBCL), submitting a credit report and two years of financial data for the customer.

Kenneth Zanolini, Director of Credit at Temperature Equipment Corp., uses credit insurance to manage high-risk, high-value accounts. In one case, his company sought $1 million in coverage for a customer. After evaluating the risk of default, the insurer approved only $500,000. Zanolini highlights the importance of understanding customer history, explaining:

"A big part of the insurance is customer history. Whether it’s a long- or short-term customer, payment patterns and average days to pay are some key factors to consider".

Automatic Invoice Coverage

Credit evaluations are further streamlined with automation, especially through whole turnover policies that automatically cover your entire customer portfolio. By integrating your ERP system with the insurer’s API, you can enable real-time data sharing of orders, invoices, and buyer details. Thanks to advancements in technology, over 70% of credit limit requests are now approved instantly without manual intervention by major trade credit insurers.

This digital integration also provides live portfolio monitoring through dashboards, giving you immediate insights into invoice coverage and the status of your order-to-cash cycle. Gabriel Prévost, Key-Accounts Team Manager at Allianz Trade France, emphasizes the importance of this process:

"A smooth order-to-cash cycle helps ensure the effective management and overview of all parts of the transaction".

Additionally, businesses using trade credit insurance report collecting payments an average of 5 days sooner than those without coverage.

Claims Support and Debt Recovery

Credit insurance doesn’t just stop at coverage – it also provides robust claims and debt recovery services to protect your revenue. If a customer defaults, insurers work to recover the debt before processing your claim. Allianz Trade, for example, handles over 100,000 debt recovery cases annually in more than 160 countries, recovering 50% of debts within the first week. The insurer’s involvement often pressures debtors to pay promptly, as non-payment on insured invoices can harm their reputation with insurers and suppliers alike.

To maintain claim eligibility, it’s crucial to file within the policy’s specified claim period. Double-check that you are listing the correct legal entity responsible for the debt, especially if the buyer has a complex corporate structure. If a customer suggests a repayment plan, be sure to get approval from your insurer first. Making unauthorized changes to payment terms could violate your policy and void your claim.

Benefits of Credit Insurance for B2B Sellers

Credit insurance does more than just protect your business from financial risks – it actively supports growth and stability in key areas.

Protecting Cash Flow

Keeping your cash flow steady is essential, and credit insurance plays a big role here. It covers up to 90% of unpaid invoices when customers face insolvency or delays in payment. This means more liquidity for your business, allowing you to handle payroll, supplier payments, and other expenses without worry. Even if customers are consistently late in paying, protracted default coverage ensures you’re not left scrambling to cover gaps.

Without credit insurance, businesses often rely on self-insurance, which involves setting aside large reserves to cover potential losses. But with credit insurance, that risk is shifted to the insurer for a premium that’s usually less than 1% of your insured sales volume. To put that into perspective, if your business operates on a 10% profit margin, losing $100,000 to bad debt means you’d need to generate $1,000,000 in new sales just to recover. Credit insurance eliminates this burden, letting you focus on growth instead of damage control.

Supporting Business Expansion

Credit insurance isn’t just about protection – it’s also a tool for growth. When you’re exploring new markets or onboarding new customers, insurers assess buyer credit limits, helping you minimize risks tied to non-payment. They evaluate the financial health of potential customers, even those with limited credit history, and assign credit limits that determine your maximum covered exposure. This gives you the confidence to extend credit to high-potential accounts without taking on unnecessary risk.

This support extends to international markets as well. With pre-assessed credit limits, you can expand globally with more certainty. The growing demand for credit insurance reflects its importance: the global trade credit insurance market was valued at $9.39 billion in 2019 and is projected to reach $18.14 billion by 2027, with an annual growth rate of 8.6% through 2027. By reducing the risks of expansion, credit insurance opens doors to new opportunities and strengthens your position in competitive markets.

Better Access to Financing

Expanding internationally not only boosts your market presence but also improves your financial standing. Credit insurance transforms unsecured receivables into secure assets, which lenders view as lower-risk. This directly translates into better borrowing terms, such as higher credit lines, lower interest rates, and more favorable loan conditions.

As Atradius points out:

"Lenders often look favorably on businesses that have the added protection of trade credit insurance and may offer better terms when lending is backed by insured receivables".

Additionally, claim payments from insured receivables can often be assigned directly to lenders. This added security strengthens your case for financing, making it easier to secure the funds needed for growth. Atradius explains:

"In many cases, claim payments can be assigned to the lender. This provides added security and highlights the benefits of trade credit insurance of companies seeking stronger, more reliable funding options".

Conclusion

Credit insurance plays a vital role in reducing financial risks and supporting business growth. By covering up to 90% of unpaid invoices, it helps protect your cash flow in situations like buyer insolvency or payment delays. For a premium that’s usually less than 1% of your insured sales volume, it shifts the burden of risk away from your business.

This type of insurance also supports smarter credit decisions. Insurers evaluate the creditworthiness of your buyers and establish coverage limits, allowing you to confidently extend credit to new customers or tap into new markets. This is particularly valuable for international sales, where political risks can jeopardize receivables. Additionally, having insured receivables can enhance your financing options – serving as reliable collateral that may lead to better credit terms, lower interest rates, and improved loan conditions.

For businesses involved in B2B sales, understanding credit insurance is critical. To explore your options, CreditInsurance.com provides a wealth of resources, including educational materials, risk assessment tools, and an extensive insurance glossary. If you need personalized advice or a tailored solution, their specialists are ready to assist you at +1-800-320-7338.

FAQs

What invoices won’t credit insurance pay for?

Credit insurance typically does not protect invoices unless the customer is insolvent or facing financial trouble. Some common exclusions include disputed or fraudulent invoices, losses tied to uninsured political risks, or force majeure events that aren’t outlined in the policy. It’s essential to carefully review your policy to understand these exclusions in detail.

How do credit limits affect how much I’m covered for each buyer?

Credit limits determine the maximum amount your insurer will cover for each buyer. If a buyer’s debt exceeds this limit, the excess won’t be insured. Keeping an eye on these limits is crucial to ensure your business remains protected.

How can credit insurance improve my bank financing terms?

Credit insurance can improve your bank financing terms by lowering the risk for lenders. With this added security, you may gain access to higher borrowing limits, increased advance rates (sometimes reaching up to 90%), and even reduced interest rates or collateral demands. These advantages help present your business as a safer investment to financial institutions.