When deciding whether to extend credit to a business, understanding credit data and trade data is critical. Here’s the key takeaway:

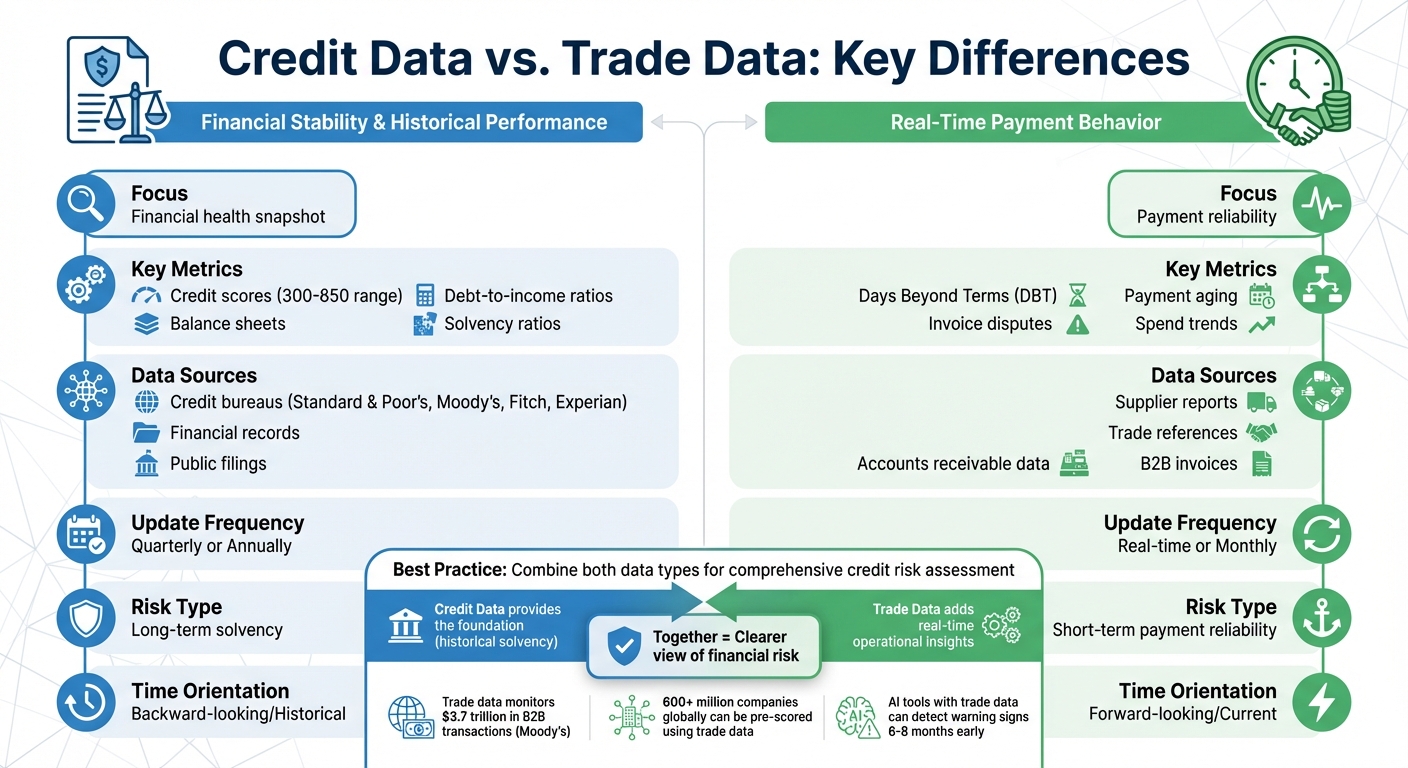

- Credit data focuses on a company’s financial health, using metrics like credit scores (300–850), balance sheets, and debt-to-income ratios. It’s historical and formal, offering a high-level picture of financial stability.

- Trade data looks at real-time payment behavior, such as whether invoices are paid on time or disputes arise. It’s behavior-driven and shows how a business manages financial obligations daily.

Both types of data are essential for assessing credit risk. Credit data provides a foundation by analyzing a company’s long-term solvency, while trade data adds real-time insights into payment reliability. Together, they create a clearer view of financial risk.

Quick Comparison:

| Feature | Credit Data | Trade Data |

|---|---|---|

| Focus | Financial stability | Payment behavior |

| Key Metrics | Credit scores, solvency ratios | Days Beyond Terms (DBT), payment aging |

| Source | Credit bureaus, financial records | Supplier reports, trade references |

| Update Frequency | Quarterly or annually | Real-time or monthly |

| Risk Type | Long-term solvency | Short-term payment reliability |

Understanding these differences ensures smarter credit decisions, whether you’re dealing with large corporations or smaller businesses.

Credit Data vs Trade Data: Key Differences Comparison Chart

Definitions and Sources

What Is Credit Data?

Credit data provides a snapshot of a borrower’s financial history, offering lenders a way to evaluate creditworthiness. It includes details like repayment habits, outstanding debts, and overall financial stability. Think of it as a formal "report card" for a company’s financial standing, covering both assets and liabilities.

The main sources for this information are credit reporting agencies such as Standard & Poor’s, Moody’s, Fitch, and Experian. These organizations gather data from banks, public records, and audited financial statements. Typical metrics include net worth, net current assets, and profitability. Additionally, credit reports feature "trade lines", which are records of business credit accounts provided by vendors and suppliers.

As Aidan Applegarth, a consultant and trade finance expert, notes: "Traditional credit analysis falls back on the quality of a borrower’s balance sheet".

This method leans heavily on historical financial data to estimate a company’s ability to manage future debt. For credit managers, this information provides concrete facts to guide lending decisions.

Next, we’ll examine trade data, which offers a more immediate look at payment behavior.

What Is Trade Data?

Trade data, also known as trade payment data, focuses on the specifics of how a business handles its financial obligations to suppliers and creditors. While credit data gives a broad financial overview, trade data zeroes in on payment habits: the duration of business relationships, payment terms like Net 30 or Net 60, and whether payments are timely or disputed.

This information comes directly from trade references – reports submitted by a company’s current suppliers and partners. Business credit agencies also gather data from third-party creditors, allowing them to compare a company’s payment behavior against industry norms. Key details include credit line amounts, payment methods, and the frequency of invoice disputes. These insights from suppliers provide a real-time view of a company’s operational behavior.

Eric Kider, Senior Vice President and General Manager of Data & Credit Solutions at Data Axle, highlights the value of this data: "Trade payment data is one of the best predictive indicators as to whether a company is likely to pay on time".

While credit data reflects financial capacity based on past performance, trade data sheds light on current reliability in day-to-day transactions. Together, these two types of data create a more comprehensive framework for assessing risk.

sbb-itb-b840488

Trade Credit I Managing Credit Data I Explainer Video

Key Differences

Let’s dig into how credit data and trade data differ in their scope, content, timeliness, and accuracy – factors that play a pivotal role in assessing credit risk.

Scope and Content

Credit data offers a broad view of a company’s financial and legal status. It includes details like firmographics, corporate hierarchy, ownership structures, legal events (such as bankruptcies or tax liens), and standardized financial ratios. These insights are gathered from sources like public filings, banks, and legal registries.

On the other hand, trade data zooms in on the granular details of daily business transactions. It tracks specific B2B interactions and accounts receivable performance through indicators such as payment aging, Days Beyond Terms (DBT), and year-over-year spending trends. Instead of assessing overall solvency, trade data focuses on "payment signals" derived from anonymized accounts receivable data.

Trade data also has the capacity to monitor large-scale B2B activity. Advanced trade risk tools can provide credit insights on over 600 million pre-scored companies globally. These systems analyze over $1.7 trillion in annual B2B transactions to flag changes that could impact revenue.

Amanda Slusarczyk, National Credit Manager at Flocor, shares: "Nine out of 10 times Moody’s has the information I am looking for on my customers and it saves us lots of money from pulling costly reports with other agencies".

The differences between these data types extend beyond content to how often they’re updated and their accuracy.

Timeliness and Accuracy

Credit data updates less frequently, typically quarterly or annually, based on financial statements and audited results from prior years. While this provides solid historical insights, it often results in a delayed picture of a company’s health.

Trade data, by contrast, operates on a much faster timeline, capturing real-time or monthly transactional performance. Delivered through APIs and connectors, it integrates directly with ERP and CRM systems, offering a forward-looking perspective that emphasizes current transactions and future receivables.

Past financial crises have shown the dangers of relying solely on backward-looking data. Delayed financial reporting can mask deteriorating conditions in volatile markets.

Aidan Applegarth, a consultant and trade finance expert, underscores this point: "A financially good looking balance sheet at the end of 2008 was justification for continued lending through the first half of 2009, even though the value of those components were beginning to collapse".

| Feature | Credit Data | Trade Data |

|---|---|---|

| Primary Focus | Financial stability and legal standing | Transactional behavior and payment patterns |

| Key Metrics | Solvency ratios, bankruptcy filings, ownership | Days Beyond Terms (DBT), payment aging, spend trends |

| Data Source | Public filings, banks, legal registries | Contributed accounts receivable and B2B invoices |

| Update Frequency | Quarterly or annual | Real-time or monthly |

| Risk Type | Structural and legal risk | Operational and liquidity risk |

Strengths and Limitations

Strengths of Credit Data

Credit data provides a standardized way to evaluate creditworthiness across industries. Agencies like Standard & Poor’s, Moody’s, and Fitch use consistent frameworks to assess financial history, including factors like debt repayment habits and formal financial statements. Thanks to its structured nature, credit data allows businesses to quickly assess legal and financial standings, such as bankruptcy filings or ownership structures. This makes it an essential tool for high-level risk assessments and setting baseline credit policies. On the other hand, trade data focuses more on real-time operational behaviors.

Strengths of Trade Data

Trade data dives into real-world payment behaviors in B2B transactions. Its granular details reveal industry-specific patterns, such as differences in credit terms (e.g., Net 30 vs. Net 60), invoice disputes, and the length of creditor relationships – factors that are vital for daily business operations. In the U.S., trade credit accounts for 17% of current assets for small businesses, highlighting its importance in evaluating operational health. Suppliers, through direct trade relationships, can access detailed customer information to assess creditworthiness, as noted by the Review of Quantitative Finance and Accounting.

Limitations of Both Data Types

While credit data offers a standardized approach, it often misses trade-specific nuances and might not be available for newer businesses without an established credit history. This makes it less effective in capturing the detailed, industry-specific payment behaviors that can signal operational risks.

Trade data, on the other hand, focuses on payment behaviors but lacks the broader financial perspective, such as total liabilities or bank debt levels, which are critical for a complete risk assessment. Extending trade credit can also introduce risks for sellers, like bad debt, delayed revenue, and strain on the balance sheet. Additionally, trade data can sometimes be tricky to interpret. For example, short credit terms like Net 10 might indicate a new relationship rather than a high-risk account, and credit card payments on short terms could mask cash flow problems.

Globally, between 80% and 90% of trade relies on some form of trade finance. However, the trade finance gap reached approximately $6.5 trillion in 2021. This gap highlights the difficulties many businesses – especially SMEs – face in accessing comprehensive credit information and financing. Small and medium-sized enterprises also often struggle to secure trade credit insurance due to a lack of formal records or because they fall below the typical minimum sales threshold of about $1 million. Recognizing these strengths and limitations is essential for improving credit risk scoring models.

Applications in Credit Risk Scoring Models

How Credit Data Contributes

Credit data is the backbone of most risk scoring models, offering a starting point for assessing creditworthiness. Lenders rely on the Five Cs – Character, Capacity, Capital, Collateral, and Conditions – to evaluate borrowers’ profiles. For instance, Character reflects a company’s reputation and dependability, often determined by payment histories from agencies like Experian, TransUnion, and Equifax. Meanwhile, Capacity examines cash flow strength, utilizing metrics such as debt-to-income ratios.

Traditional credit scores, like FICO and VantageScore (ranging from 300 to 850), remain the primary quantitative tools for this purpose. However, these scores have their flaws. For example, negative records, such as bankruptcies, can linger on credit reports for up to a decade, potentially misrepresenting a borrower’s current financial state. While credit data provides a historical lens, it often lacks the real-time insights needed to paint a complete picture. That’s where trade data steps in to enhance these models.

How Trade Data Refines Scoring Models

Trade data builds on the historical foundation of credit data by offering real-time insights into a company’s operational health. It captures up-to-date payment behaviors, such as Days Beyond Terms (DBT) and receivables aging, which help refine the baseline credit data provides. For example, Moody’s trade credit database tracks approximately $3.7 trillion in B2B transactions every two years. This scale allows lenders to monitor payment trends across various industries, improving the accuracy of predictive models.

The combination of credit and trade data significantly boosts predictive capabilities. AI-powered credit sentiment tools that incorporate trade data can detect warning signs 6 to 8 months before major credit events occur for high-profile companies. This early detection allows lenders to make proactive adjustments, reducing their dependence on outdated credit reports. Trade data is particularly useful for evaluating private companies and small-to-medium enterprises (SMEs), which often lack detailed public financial records. By filling these gaps, trade data addresses critical blind spots that credit bureaus alone cannot cover.

"Moody’s Pulse turns anonymized, contributed accounts receivable data into forward-looking payment risk insight so credit teams can spot critical changes to their customer’s financial health in time to act with confidence."

This integration represents a shift from reactive risk management to a proactive strategy. By combining the reliability of historical credit data with the immediacy of trade data, lenders can better anticipate and respond to financial risks.

Choosing the Right Data for Credit Risk Assessment

When it comes to credit risk assessment, the type of data you rely on should align with the profile of the business being evaluated. Both credit data and trade data offer distinct advantages, but their usefulness depends on the specific circumstances and insights you’re seeking.

For large, investment-grade corporations, credit data is a reliable tool. These companies typically have strong balance sheets, audited financials, and established credit histories. This makes backward-looking analysis effective for evaluating long-term solvency and debt capacity. Credit data provides a clear picture of their ability to manage debt and maintain financial stability over time.

On the other hand, smaller or sub-investment-grade businesses often require a different approach. These companies may lack substantial tangible assets, making it harder to assess their creditworthiness through traditional metrics alone. In such cases, trade data becomes essential. Trade data offers a forward-looking perspective, capturing real-time operational behaviors and identifying risks that credit reports might overlook. For example, in August 2022, Blue Water Industries utilized Moody’s Pulse to monitor its accounts receivable. Carl Davidson, Director of Credit and Collections, used the tool to catch critical credit alerts, avoiding a $30,000 charge-off by adjusting credit lines before a payment issue arose. This highlights how trade data can be a game-changer for spotting risks early.

The best strategy combines both datasets. Credit data lays the groundwork by evaluating a borrower’s historical performance, focusing on their Character and Capacity. Trade data, meanwhile, adds depth by providing real-time insights into operational behavior. A great example comes from May 2022, when Flocor’s National Credit Manager, Amanda Slusarczyk, shared how automated trade data monitoring saved her credit team over 450 hours each year. It also delivered crucial early warnings for accounts at risk.

The choice of data should also depend on the time horizon of your assessment. Credit data is ideal for determining whether a company can service its debt based on factors like net worth and profitability. Meanwhile, trade data focuses on the likelihood of timely payments, offering insights into transaction-level risks, such as performance, logistics, and settlement issues. For businesses managing trade credit or accounts receivable, integrating internal AR data with external credit data can fill in gaps and enable proactive risk management.

"Traditional credit analysis falls back on the quality of a borrower’s balance sheet… for sub-investment grade corporates and SMEs who are typically light on fixed and net current assets, balance sheet lending rarely justifies the sort of funding needs these firms require." – Aidan Applegarth, Consultant

FAQs

When should I rely more on trade data than credit data?

When trying to predict a company’s future payment behavior, trade data can be incredibly helpful. By examining payment histories and references, you gain a clearer picture of how a company has managed its financial obligations with other creditors. This type of information highlights patterns of financial responsibility and punctuality, offering a more behavior-focused perspective. Unlike credit data, trade data dives deeper into the company’s direct interactions with creditors, providing valuable insights into its payment habits.

How can I use trade data to spot payment risk earlier?

Analyzing trade data, such as a company’s payment history and behavior, can help spot potential payment risks early. By reviewing third-party trade payment data, you can compare a company’s payment patterns to industry averages, giving you a clearer picture of its likelihood to pay on time. Trade references from creditors also add valuable context, offering details about payment history, credit terms, and financial reliability. These insights are crucial for assessing risks before deciding to extend credit.

What should I do if a business has little or no credit history?

If a business lacks a solid credit history, there are other ways to evaluate its creditworthiness. One option is to look at trade data, which examines the company’s transaction history with suppliers and customers. This can reveal patterns in financial behavior and payment reliability.

Additionally, fostering strong trade relationships and keeping a close eye on trade credit performance over time can reduce risks and help the business build a credible credit profile. These steps not only provide alternative insights but also support the development of a more reliable financial track record.