Credit insurance is a tool that protects manufacturers from financial losses when customers fail to pay. Despite its benefits, misunderstandings often prevent businesses from using it effectively. Let’s address some myths:

- Cost Concerns: Premiums range from 0.05% to 0.75% of insured sales, making it affordable compared to the potential loss from a major customer default.

- Size Relevance: Small and medium-sized manufacturers face higher risks from customer defaults; tailored policies help mitigate these risks.

- Coverage Limits: It’s not just about bankruptcy. Credit insurance also covers late payments, political risks, and even pre-shipment losses.

- Growth Restrictions: Instead of limiting growth, credit insurance enables manufacturers to extend credit safely, expand into new markets, and secure better financing terms.

- Self-Insurance Fallacy: Setting aside cash reserves is inefficient and lacks the expertise and global resources insurers provide.

- Claims Complexity: Modern systems simplify claims, with insurers offering tools and support for quick payouts.

Credit insurance isn’t just about risk protection; it supports growth, enhances financial stability, and provides peace of mind. For manufacturers, it’s a smart way to safeguard against uncertainties while pursuing new opportunities.

Credit Insurance – The Silent Growth Engine | NextGen 10X Growth Conference | AIPMA

sbb-itb-b840488

Myth #1: Credit Insurance Costs Too Much for Manufacturers

It’s a common misconception that credit insurance is an expensive add-on for manufacturers. But the truth is, premiums typically range between 0.05% and 0.75% of insured sales. For a manufacturer generating $2 million in annual sales, that’s just $1,000 to $15,000 per year – an amount far smaller than the financial hit from a single major customer default.

How Risk-Based Pricing Works

Credit insurance isn’t priced the same for everyone. Premiums are influenced by factors like your annual sales volume, the stability of your industry, the creditworthiness of your customers, and the regions where your buyers are located. Selling to financially solid customers in steady markets means lower premiums, while working with buyers in riskier or more unstable areas may result in higher costs.

For smaller manufacturers, modular policies can help manage expenses. Atradius explains this flexibility:

Modula allows for varying levels of risk and need between customers to be clearly identified and differentiated… so you don’t have to pay for something you won’t need.

This means you can choose coverage that focuses on specific customer groups or markets rather than opting for blanket protection. For example, smaller companies engaged in domestic trade can benefit from specialized products like Atradius GO, which offers protection for receivables up to $200,000 at a fixed, manageable price.

This tailored approach ensures you’re only paying for the protection you truly need, keeping costs in check.

Comparing Costs to Potential Losses

Let’s break it down: shipping $300,000 worth of goods on 90-day terms is essentially like giving out an unsecured loan. If that customer goes bankrupt, you could lose the entire $300,000. However, with a 0.75% premium, insuring that shipment costs just $2,250. And if your policy covers 90% of the invoice, you’d recover $270,000 in a claim – a net benefit of $267,750.

Marc D. Wagman, Managing Partner at Aequus Trade Credit, sums it up well:

Would your shareholders, lenders, employees and vendors all agree with the assessment that ‘credit insurance is too expensive’ in the event that your company suffer a large payment default which could have been credit insured?

On top of that, credit insurance premiums are tax-deductible, unlike bad debt reserves, which many manufacturers maintain but cannot deduct. In some cases, credit insurance can even pay for itself by allowing you to confidently expand into new markets or work with customers you might otherwise avoid due to credit risks.

Myth #2: Only Large Manufacturers Need Credit Insurance

Small and medium-sized manufacturers often face greater risks from buyer defaults compared to larger companies. As Securitas Global Risk Solutions explains, "Losing one large buyer can be catastrophic".

Challenges for Small Manufacturers

For smaller manufacturers, the stakes are high when it comes to customer concentration. If 30%–50% of their revenue depends on just a few key buyers, a single default could severely impact their operations. Tight profit margins further complicate matters, leaving little room to absorb the blow of unpaid invoices. Extended payment terms can also stretch cash flow to its limits, making it harder to stay afloat.

Another hurdle is the lack of credit transparency. Smaller manufacturers often deal with private companies that don’t share financial data, making it harder to gauge a buyer’s creditworthiness. These challenges highlight the need for tailored credit insurance solutions.

Tailored Coverage for Smaller Manufacturers

Fortunately, there are specialized insurance products designed with small and medium-sized manufacturers in mind. For example:

- Single Customer or Named Customer coverage: This option focuses on protecting against the failure of a manufacturer’s largest accounts.

- EXIM‘s Multi-Buyer Small Business Insurance: Specifically created for SBA-defined businesses, this policy has no minimum premiums or first-loss deductibles and covers 95% of both commercial and political risks.

- EZ Cover: Offers instant credit decisions through online platforms, streamlining the administrative process.

Heather Smart Johnson, a Credit Insurance Specialist, emphasizes the growing need for credit insurance: "Business insolvency is predicted to increase due to global events". In response, many middle-market manufacturers are adopting credit insurance as both a defensive tool and a growth strategy.

Credit insurance doesn’t just shield against risks – it also opens doors for growth. For instance, insured receivables can serve as collateral for loans, improving liquidity and securing better borrowing terms. This is a game-changer for small manufacturers aiming to expand.

Myth #3: Credit Insurance Only Protects Against Insolvency

Many manufacturers mistakenly believe that credit insurance solely covers bankruptcy. In reality, it also shields businesses from payment delays, political events, and risks tied to production before shipment.

What Risks Are Covered

Credit insurance goes beyond insolvency to address protracted defaults, where buyers consistently fail to meet payment deadlines. For example, if a customer is 60 days late on a 30-day payment term, credit insurance can help smooth over the cash flow issues this creates.

Political risks are another major area of protection, especially for manufacturers selling internationally. These risks include government actions that disrupt payments, such as revoked export or import licenses, restrictions on currency transfers, asset expropriation, or even war and insurrection.

For manufacturers dealing with custom or made-to-order products, pre-shipment endorsements are invaluable. This coverage protects the costs of work-in-process and finished goods that haven’t yet been shipped, offering peace of mind for businesses managing long production cycles.

| Risk Category | Description | Manufacturing Impact |

|---|---|---|

| Protracted Default | Extended payment delays beyond agreed terms | Strains cash flow needed for raw materials and payroll. |

| Currency Transfer Risk | Inability to convert local currency into U.S. dollars | Blocks payment even if the buyer has the funds. |

| Pre-Shipment Risk | Political events affecting goods before shipment | Safeguards investments in work-in-process and custom inventory. |

| Trade Restrictions | Sudden bans or cancellations of import licenses | Leaves goods stranded or unusable in other markets. |

These protections are not just theoretical – they address real-world challenges manufacturers face.

Manufacturing Example: Export Disruptions

Imagine a U.S. manufacturer shipping industrial equipment overseas. Even if the buyer has the funds and intends to pay, currency transfer risk could prevent them from converting their local currency into U.S. dollars. Similarly, unexpected government actions, like canceling an import license or imposing trade restrictions while goods are in transit, could result in significant losses.

EXIM provides support for businesses in over 170 countries, and claims related to political risks are typically processed within 60 days. If goods are disrupted while in transit, manufacturers can often work with their insurer to redirect shipments to alternative buyers, minimizing financial damage.

For manufacturers producing custom products with long lead times, a pre-shipment endorsement offers an added layer of security. This coverage not only reimburses costs but may also include a small profit margin if an export is canceled before shipment. However, exporters must ensure that buyers are legally authorized to import the goods at the time of shipment to maintain their coverage.

Myth #4: Credit Insurance Restricts Sales Growth

Some manufacturers worry that credit insurance might limit their ability to grow by restricting customer reach. However, the truth is quite the opposite – credit insurance can open doors to new opportunities that might otherwise seem too risky, especially when exploring new markets or working with unfamiliar buyers.

How Credit Insurance Fuels Sales Growth

Credit insurance empowers manufacturers to offer competitive open account terms to buyers they might have hesitated to work with. Without this coverage, manufacturers often have to impose strict payment terms, limiting their flexibility. But with credit insurance in place, they can confidently extend credit, knowing they’re protected if a customer fails to pay. This is particularly beneficial for export sales, where buyers often expect flexible payment terms. As Alexis Bascombe, Business Development Specialist at EXIM, points out:

Lenders are more willing to lend against insured receivables, support flexible open account terms, and expand into riskier markets.

Additionally, insurers provide independent credit assessments, helping manufacturers make better decisions about which customers to pursue. They can flag potential issues with buyers – especially private companies or foreign customers with limited transparency – before any shipments are made. This extra layer of insight allows manufacturers to expand into new markets more securely. Kirk Elken, Co-founder of Securitas Global Risk Solutions, explains:

Trade credit insurance allows manufacturers to extend credit – fueling safer growth.

For export sales, the advantages are even more pronounced. Export credit insurance policies typically cover 90% to 100% of the invoice amount if a foreign buyer defaults. With premiums as low as $0.55 per $100 of invoice value – just $55 on a $10,000 shipment – manufacturers can confidently pursue international contracts that might otherwise seem too risky. In 2024, around 86% of EXIM’s transactions supported small businesses, proving that credit insurance isn’t just for large corporations.

This ability to extend credit not only boosts sales but also enhances a manufacturer’s financial position, making it easier to secure better financing options.

Turning Insured Receivables into Financing Opportunities

By reducing risk, credit insurance doesn’t just encourage growth – it also strengthens a company’s financial foundation. Insured receivables become "bankable assets" that lenders view as reliable. With credit insurance, banks often raise advance rates from 75% to 85-90%, while also offering lower interest rates and fewer restrictions. As Atradius explains:

Banks recognize insured receivables as secure collateral, and companies with trade credit insurance are viewed as having more predictable cash flow.

This financing edge becomes even more valuable when addressing customer concentration risk. Lenders often exclude receivables from a single large customer or foreign accounts from their borrowing base. Credit insurance changes this, making those accounts eligible and expanding access to capital. According to Marc D. Wagman, the additional revenue generated through better financing can often cover the cost of insurance premiums, which typically range from 0.05% to 0.75% of insured sales. In short, the growth enabled by credit insurance often pays for itself.

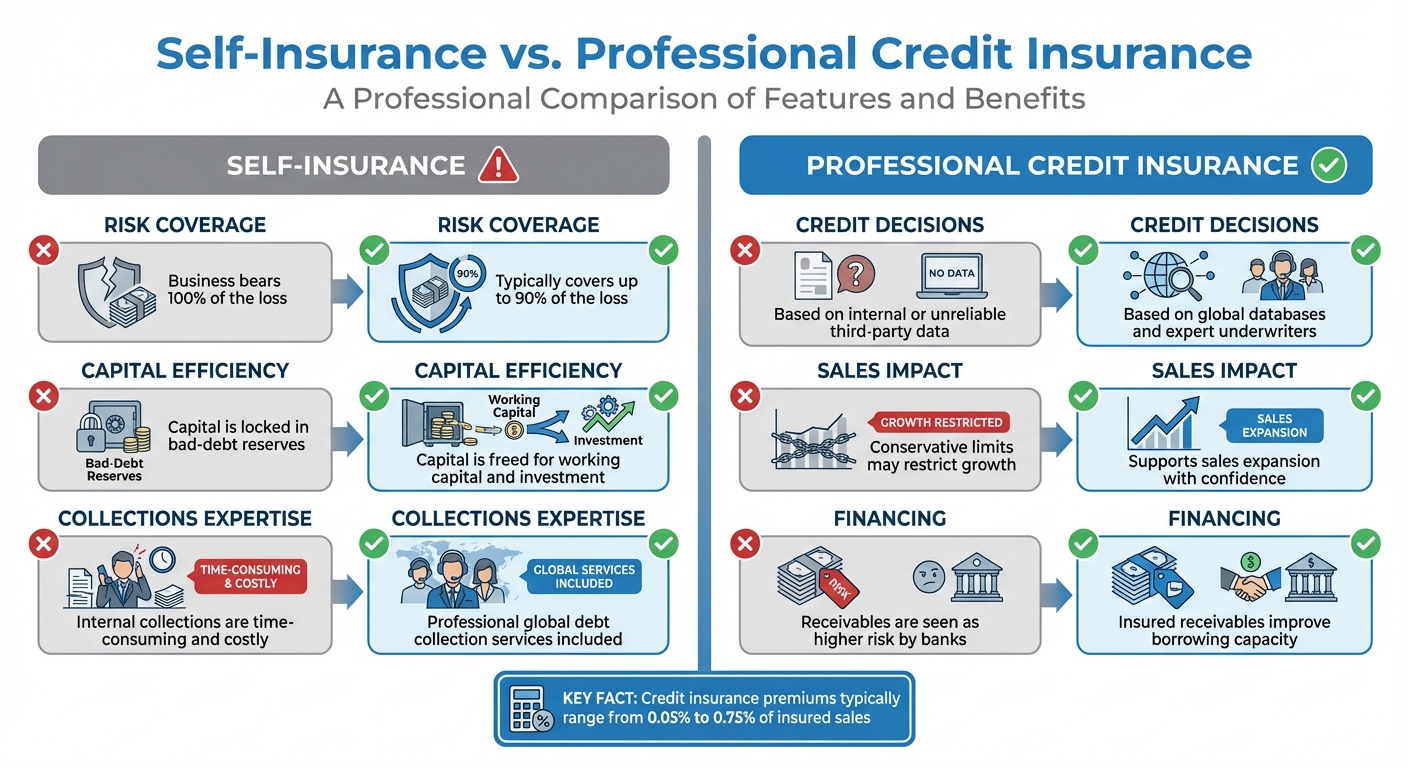

Myth #5: Self-Insurance Provides Adequate Protection

Self-Insurance vs Professional Credit Insurance: Key Differences for Manufacturers

Some manufacturers think they can manage credit risk by setting aside cash reserves for bad debts. While this might seem like a cost-saving move, it often leads to more challenges than benefits. Self-insurance not only ties up funds that could fuel growth but also lacks the expertise and resources provided by a formal credit insurance policy.

Problems with Self-Insurance

Credit insurance is specifically designed to handle risk in manufacturing, but relying on self-insurance exposes businesses to critical weaknesses.

One major issue is capital inefficiency. To self-insure, manufacturers have to lock away significant amounts of cash in bad-debt reserves – funds that could otherwise be used for upgrading equipment, investing in research, or expanding into new markets. Allianz Trade highlights this drawback:

Self insurance requires companies to tie up important sources of capital in large bad-debt reserves and credit insurance does not.

Another problem is the full burden of losses. When a major client files for bankruptcy, the unpaid invoices directly hit the company’s bottom line. Coface warns about the risks:

Self insurance funds can quickly dry up and, suddenly, the cost of a premium is a small fraction to the overall impact to your business.

Self-insured manufacturers also face challenges in making credit decisions. Without access to comprehensive global databases – like those professional insurers use – they often rely on limited internal information or less reliable third-party sources. This leads to conservative credit limits that can stifle growth opportunities. And if customers fail to pay, self-insured companies are left to handle collections on their own, a process that eats into time and resources. Atradius emphasizes this point:

Without credit insurance, you are left to handle all aspects of debt collection on your own. This can be a time-consuming and costly process, taking resources away from core business activities.

Self-Insurance vs. Credit Insurance Comparison

To illustrate the differences, here’s a side-by-side comparison of self-insurance and professional credit insurance:

| Feature | Self-Insurance | Professional Credit Insurance |

|---|---|---|

| Risk Coverage | Business bears 100% of the loss | Typically covers up to 90% of the loss |

| Capital Efficiency | Capital is locked in bad-debt reserves | Capital is freed for working capital and investment |

| Collections Expertise | Internal collections are time-consuming and costly | Professional global debt collection services included |

| Credit Decisions | Based on internal or unreliable third-party data | Based on global databases and expert underwriters |

| Sales Impact | Conservative limits may restrict growth | Supports sales expansion with confidence |

| Financing | Receivables are seen as higher risk by banks | Insured receivables improve borrowing capacity |

Credit insurance premiums typically range from 0.05% to 0.75% of insured sales, a relatively small investment compared to the financial blow of a major customer default. Marc D. Wagman, Managing Partner at Aequus Trade Credit, puts it plainly:

Given that accounts receivable are often a company’s largest and most liquid balance sheet asset, why should that remain uninsured?

For manufacturers, the choice is clear. Professional credit insurance not only provides stronger protection but also frees up resources and supports business growth – advantages that self-insurance simply cannot deliver. This makes it the smarter option for managing risk and driving success.

Myth #6: Filing Claims Is Too Difficult for Manufacturers

Some manufacturers shy away from credit insurance, thinking the claims process is too complex or time-consuming. However, modern systems have simplified the process, even for industry-specific scenarios. With clear documentation requirements and expert guidance, manufacturers can secure compensation quickly when a customer fails to pay.

How Claims Work for Manufacturers

The claims process is designed to keep your cash flow steady – a critical factor for manufacturers juggling tight production schedules. When a covered loss occurs, the first step is to notify your insurer and submit the necessary documents. These typically include invoices, credit agreements, delivery receipts, and, for export sales, a bill of lading to confirm the debt.

Insurers have embraced technology to make this process smoother. Many now offer digital submission portals and checklists to simplify filing. For example, the Export-Import Bank of the United States (EXIM), which insured around 110,000 shipments under multi-buyer policies in a single year, provides an online system for submitting proof-of-loss forms. Claims for protracted defaults are typically filed after 150 days past due, while insolvency claims must be submitted within 10 to 20 days of filing.

Once approved, the insurer pays a percentage of the loss based on your policy’s indemnity level and takes over the responsibility of recovering the debt from the defaulting customer. This quick compensation lets you focus on production rather than chasing unpaid invoices. As eoxs.com puts it:

The claims process is designed to facilitate timely compensation for insured losses, supporting businesses in maintaining cash flow and mitigating financial risks.

To avoid complications, manufacturers should take certain precautions. For example, ensure all entity details are accurate – listing the wrong subsidiary or parent company can result in a denied claim. Ken Click, Business Development Specialist, and Amy Davis, Claim Officer at EXIM, stress this point:

Insured exporters should confirm the buyer’s name and address in their home country is consistent throughout when submitting buyer obligation documents to EXIM in the event of a claim.

Additionally, any repayment plans must be pre-approved by your insurer. Agreeing to an unapproved plan could void your right to file a claim later. For export sales, always use third-party logistics documents; internal shipping records won’t meet proof-of-export requirements.

This streamlined process ensures manufacturers can maintain cash flow, supporting both day-to-day operations and future growth.

Getting Help from CreditInsurance.com

Specialized resources are available to make the claims process even easier.

CreditInsurance.com provides tools like calculators, credit reports, and directories tailored for manufacturers. They also connect businesses with experienced credit insurance specialists who can advocate on their behalf during the claims process. Heather Smart Johnson, a writer for CreditInsurance.com, explains:

A trade credit insurance broker is an advocate for you when dealing with the credit insurance company. Let us help you find someone who will be a true partner and help you get paid.

These specialists are well-versed in the unique challenges manufacturers face, such as distinguishing between "insolvency" and "protracted default." They can guide you through disputes and ensure your claim is handled efficiently. With expert assistance and clear documentation requirements, filing a claim becomes a straightforward step in safeguarding your business.

Conclusion

Credit insurance is a valuable tool for manufacturers of all sizes, offering protection for cash flow while supporting growth strategies. It goes beyond simply guarding against bankruptcy – it also shields businesses from issues like habitual late payments, political upheavals, and the everyday challenges of extending credit to customers.

The adoption of credit insurance by American companies has grown significantly, rising from just 1 in 50 in the early 1990s to nearly 1 in 10 today. This shift shows how businesses are recognizing the advantages of insured receivables, such as improved financing terms. By helping determine credit limits and turning receivables into dependable short-term financing, credit insurance becomes a key enabler for expansion. Considering that 80% of businesses face unpaid debts and 25% of unpaid invoices contribute to bankruptcies, having strong protection in place is no longer optional. With global business insolvencies expected to rise due to ongoing geopolitical and economic uncertainties, taking proactive steps now can help manufacturers avoid future disruptions.

At CreditInsurance.com, you’ll find experienced brokers who compare multiple quotes, tailor coverage to your needs, and advocate for you during claims. Their educational tools, such as calculators, credit reports, and risk assessments, empower you to understand your risks before committing to a policy.

It’s important to view credit insurance as a complement to your existing credit practices, not a substitute for solid business fundamentals. Whether you’re looking to protect domestic sales, international portfolios, or high-value accounts, credit insurance provides a way to safeguard your assets while giving you the confidence to grow in today’s unpredictable markets.

FAQs

What isn’t covered by a credit insurance policy?

Credit insurance policies do not address payment disputes that arise between buyers and sellers. These disputes could involve disagreements over the amount due or issues with the quality of goods or services delivered.

How do insurers set credit limits for my customers?

Insurers set credit limits by evaluating several factors tied to your customers’ financial situation. They look at financial health, payment history, industry-specific risks, and management practices. This process includes reviewing applications, performing risk assessments, and analyzing financial documents. Based on these findings, they decide whether to fully approve, partially approve, or deny the requested credit limits.

Can credit insurance help me get a larger credit line from my bank?

Yes, credit insurance can help you qualify for a larger credit line. By safeguarding lenders against risks like non-payment and customer insolvency, it lowers their exposure. This added protection often leads to higher advance rates on receivables, giving you more borrowing power.