B2B credit scoring models help businesses assess the payment reliability of their customers. These models use data like payment history, financial statements, and public records to calculate risk and set appropriate credit terms. By blending internal and external data, adjusting scoring parameters for different customer types, and leveraging tiered systems, businesses can make informed credit decisions and reduce financial risks. Advanced tools like machine learning and behavioral metrics further refine these models, improving accuracy and efficiency. Pairing credit scoring with trade credit insurance adds an extra layer of protection, helping businesses safeguard cash flow while extending credit responsibly.

Key takeaways:

- Combine internal data (e.g., payment history) and external sources (e.g., credit reports) for precise scoring.

- Adjust parameters for new vs. existing customers and industry-specific needs.

- Use tiered scoring systems to streamline credit decisions.

- Incorporate machine learning for better predictive accuracy.

- Enhance risk management with trade credit insurance to protect against major losses.

These practices ensure consistent, data-driven credit decisions while minimizing exposure to financial risks.

Essential Components of B2B Credit Scoring Models

How to build credit scoring models?

sbb-itb-b840488

Core Elements of B2B Credit Scoring Models

Managing financial risk effectively hinges on having a solid credit scoring system. Here’s a closer look at the essential components that drive successful B2B credit scoring models.

Combining Internal and External Data

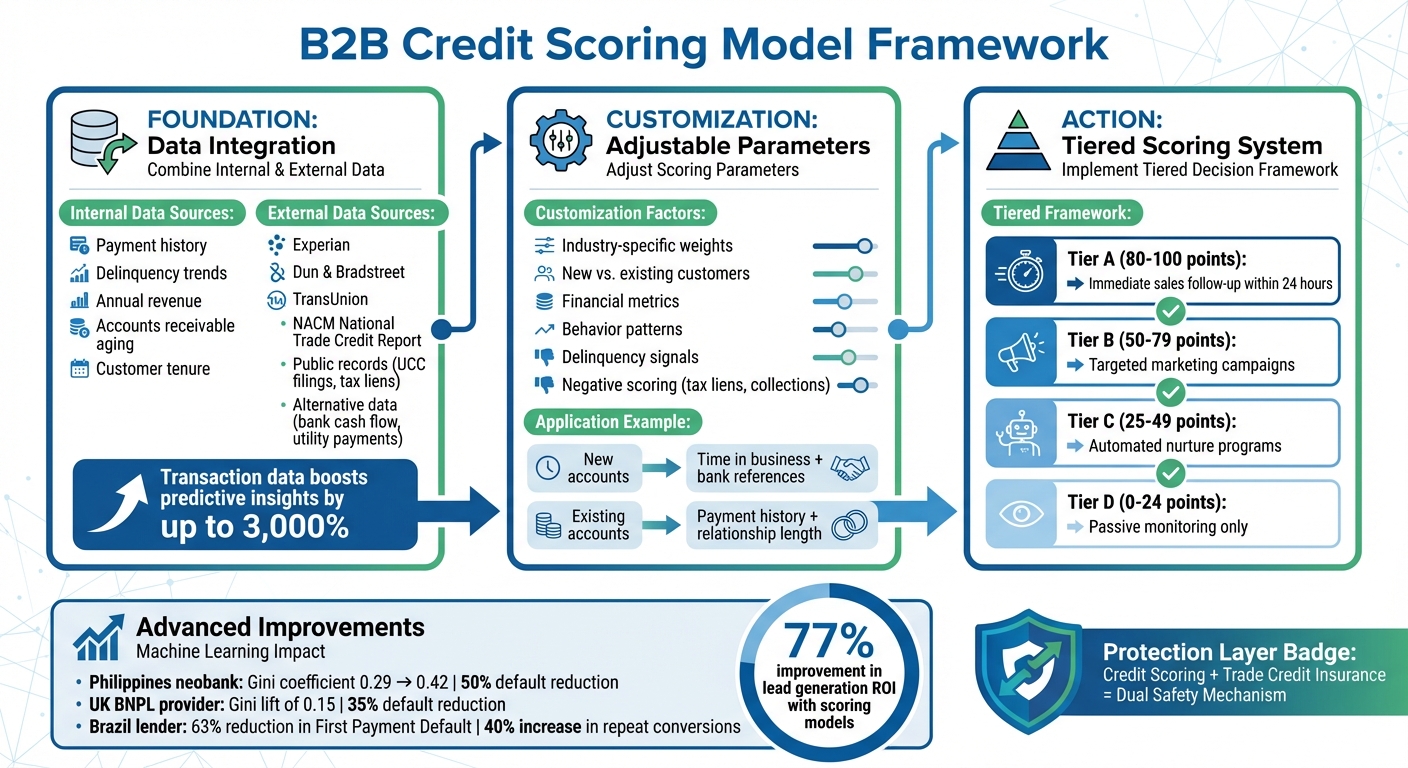

A reliable B2B credit scoring model blends internal data (like payment history, delinquency trends, annual revenue, accounts receivable aging, and customer tenure) with external sources such as Experian, Dun & Bradstreet, TransUnion, NACM’s National Trade Credit Report, and public records (e.g., UCC filings and tax liens). It can even include alternative data like bank cash flow and utility payment records.

Why does this matter? Because transaction data can boost predictive insights by up to 3,000%. Traditional credit bureau data works well for businesses with established credit histories. However, startups and companies with limited records – so-called "thin-file" applicants – require alternative data to paint a more complete picture of their creditworthiness. For these businesses, alternative sources are critical to making accurate risk assessments.

But gathering data is just the first step. Customizing and fine-tuning the scoring process is just as important.

Adjustable Scoring Parameters

Credit scoring isn’t one-size-fits-all – it needs to reflect the nuances of different industries and customer types. Adjusting weights for financial metrics, behavior patterns, and delinquency signals based on your specific needs ensures a more accurate risk profile. Nate Yagle, VP of Credit at Premier Companies, highlights how his firm tweaks these parameters for different divisions:

"In our heat division, we view that as a very transactional type of account, so we rarely use internal credit scoring systems… For the agronomy side of business… many trade lines are not reported to the bureaus… so it makes it hard to have an accurate score for the farm itself and causes us to rely on additional metrics and resources to make our decision".

Flexibility is especially critical when handling new versus existing customers. For new accounts, factors like time in business and bank references might take precedence. On the other hand, existing customers are often evaluated based on internal payment history and the length of the relationship. Additionally, negative scoring can help flag risks by subtracting points for issues like tax liens or recent collections.

Once parameters are set, organizing accounts into tiers simplifies decision-making even further.

Using Tiered Scoring Systems

Tiered scoring systems – commonly grouped into A/B/C/D categories – help streamline operations by defining clear actions for each group. For example:

- Tier A (80-100): Immediate sales follow-up within 24 hours.

- Tier B (50-79): Targeted marketing campaigns.

- Tier C (25-49): Automated nurture programs.

- Tier D (0-24): Passive monitoring only.

This approach ensures consistency across teams and prioritizes resources effectively. Kristin Caswell, Director of Credit at Dakota Supply Group, underscores this point:

"If a neutral and consistent credit limit setting is important to you, the credit scoring helps guide you down that path".

To keep this system effective, it’s crucial to regularly review and adjust score thresholds. For instance, if 70% of accounts fall into Tier A, your criteria might be too lenient and require tightening. Integrating these thresholds with your CRM can also automate task creation when accounts move between tiers, keeping your processes efficient and responsive.

How to Improve Credit Scoring Model Performance

Building a credit scoring model is just the beginning – keeping it accurate and effective over time is where the real challenge lies. The difference between a static model and one that stays sharp often comes down to three strategies: using advanced technology, identifying your best customers, and turning scores into actionable business rules.

Use Machine Learning and Real-Time Data

Traditional credit scoring relies on fixed rules and historical patterns, which can miss important details. Machine learning (ML) takes things to the next level by uncovering complex, nonlinear relationships that traditional methods can’t detect. These models can process vast amounts of data, from device metadata to behavioral signals, to identify hidden risk factors.

For example, in April 2025, a neobank in the Philippines added ML-driven behavioral insights to its credit model. The result? Its predictive power, measured by the Gini coefficient, jumped from 0.29 to 0.42, cutting default rates by 50%. A Buy Now, Pay Later provider in the UK saw a Gini lift of 0.15 by incorporating alternative data, reducing defaults by 35%. Meanwhile, a lender in Brazil used mobile SDKs to gather behavioral metadata, slashing First Payment Default rates by 63% over seven months and increasing repeat customer conversions by 40%.

However, ML models aren’t a "set it and forget it" solution. Economic changes and evolving consumer behavior can lead to prediction decay. To stay ahead, monitor metrics like the Population Stability Index (PSI) and retrain your models regularly with fresh data. Businesses already using lead and account scoring models report a 77% improvement in lead generation ROI compared to those that don’t.

With these advanced tools in place, the next step is to pinpoint the right customers to target.

Define Your Ideal Customer Profile and Behavioral Metrics

Using ML insights, you can refine your risk predictions by clearly defining your Ideal Customer Profile (ICP).

"Scoring accounts without a well-defined ICP is like trying to hit a target with your eyes closed." – Team Factors

Your ICP lays the groundwork for effective scoring. Start by analyzing your top 20 revenue-generating accounts: What industries are they in? How large are their companies? Who are the key decision-makers? These patterns reveal the customers most likely to pay on time and build strong relationships with your business.

A good model combines firmographic data (such as industry, revenue, and location), technographic data (like tech stack compatibility), and behavioral engagement (e.g., website visits, demo requests, or content downloads) [1,7]. To keep your model up-to-date, implement score decay rules that reduce points for inactive accounts, ensuring the data reflects current engagement levels [1,8].

Once your ICP is defined, assign weights to each attribute based on its impact on successful outcomes. For instance, firmographics might account for 30–40% of the score, while behavioral intent could contribute 15–20%. Late-stage actions, like viewing pricing pages, should carry more weight than early-stage activities, such as reading blog posts. Recalibrate your model quarterly by comparing predicted scores with actual performance data, ensuring it remains aligned with real-world results [1,7].

Set Clear Credit Policies

Credit scores are only useful if they lead to consistent and actionable decisions. Clear policies help turn refined scores into specific credit actions, improving how the model performs overall. For example, accounts scoring 80–100 might be approved with Net 60 terms, while those scoring 25–49 may require restricted credit or personal guarantees.

A delegation of authority matrix can further streamline the process. This document outlines who can approve specific credit limits – credit analysts might handle requests up to $25,000, while managers handle amounts up to $100,000. This approach prevents "approval shopping" and ensures consistency across your team.

Switch from calendar-based reviews to event-driven monitoring. Instead of reviewing accounts on a fixed schedule, set up triggers for events like a drop in third-party credit scores, a sudden rise in Days Sales Outstanding (DSO), or legal actions. These triggers can integrate with your CRM or ERP system to automate actions, such as placing orders on hold or granting approvals. With 47% of professionals reporting that up to 10 sales deals are rejected monthly by finance, automation based on clear policies can cut down on conflicts and speed up decisions.

Combining Credit Scoring with Trade Credit Insurance

Pairing robust credit scoring practices with trade credit insurance creates a solid safety net against major financial setbacks. While credit scoring models help identify potential default risks, trade credit insurance works to reduce the financial blow when those risks materialize. Think of your credit scoring system as the first layer of protection – your early warning system. Trade credit insurance, on the other hand, steps in to shield your business from catastrophic losses that could disrupt operations, breach bank covenants, or even threaten access to credit lines. Together, these tools strengthen your credit management strategy and provide a more secure foundation for your business.

"Pursue credit insurance to help insulate the pain of a very large loss. You may not ever expect Large Public Customer X to be a bad debt risk, but if they are, make sure they don’t take your company down with them if they go." – Scott Simpson, SVP Capital One Trade Credit

This combined approach allows you to extend higher credit limits to key customers while keeping your business protected. Your credit scoring model sets clear boundaries and flags potential risks, while modern underwriting techniques – like AI-driven sentiment analysis – offer an added layer of foresight. These technologies can detect early warning signs of credit issues up to six to eight months in advance. This gives you and your insurer time to adjust coverage and prepare, rather than reacting to a sudden default.

Behavioral scoring can also be used to trigger collection alerts and activate insurance protocols. At the same time, setting maximum credit lines for each customer ensures you limit your exposure to risk. Platforms like CreditInsurance.com provide resources to help businesses integrate credit insurance into their risk management strategies. They guide companies in choosing the right coverage and show how insured receivables can improve access to financing.

If an insurer decides to withdraw coverage, it’s crucial to reduce credit limits gradually. A sudden reduction could trigger liquidity issues for your buyer, creating bigger problems for both parties. Work closely with your insurer to phase out coverage in a way that minimizes disruption. As Simpson wisely points out, "the real measure of credit risk protection is taken under economic duress, not in good times".

Conclusion

We’ve delved into strategies like data integration, adaptable scoring parameters, and risk management through trade credit insurance – key elements of a strong B2B credit scoring model. Such models are essential for safeguarding cash flow and making smarter credit decisions. In fact, data reveals that scoring models can increase lead generation ROI by 77%. Beyond the numbers, these tools help businesses avoid significant losses that could threaten their operations. As Scott Simpson from Capital One Trade Credit explains:

"The gold standard is to have credit risk models that successfully score an applicant based upon variables that are statistically significant predictors of severe delinquency or charge offs".

By combining predictive scoring with behavioral monitoring, businesses can achieve instant approvals and streamline processes. Integrating trade credit insurance into this system adds another layer of protection: scoring models flag risks early, while insurance shields against major losses that could disrupt banking relationships or credit lines.

Together, credit scoring and trade credit insurance act as a dual safety mechanism. Scoring identifies potential risks upfront, while insurance provides a fallback for worst-case scenarios. This combination allows businesses to extend credit to valuable accounts without exposing themselves to undue risk. Platforms like CreditInsurance.com offer guidance on how insured receivables can improve financing opportunities and provide the security needed to grow confidently.

As Simpson wisely points out:

"The real measure of credit risk protection is taken under economic duress, not in good times".

To stay ahead, set firm credit limits, update your scoring models quarterly, and use insurance to limit exposure. These practices turn credit management into a strategic advantage, enabling you to manage risk effectively while pursuing growth with confidence.

FAQs

How do I score “thin-file” business customers?

To assess "thin-file" business customers – those with limited credit history – it’s essential to look beyond traditional credit reports. Instead, consider alternative data sources such as:

- Sanctions lists

- Bankruptcy filings

- Business liens

- Litigation history

- Negative press coverage

These additional insights provide a more complete picture of a business’s financial health. By tapping into this broader range of information, you can better evaluate their stability and mitigate the risks that come with minimal credit activity.

How often should I retrain and recalibrate my model?

To keep models accurate and aligned with changing data and risk conditions, it’s important to retrain and recalibrate them on a regular basis. This often happens monthly or quarterly, depending on how fast your data changes and the specific needs of your use case.

When should I add trade credit insurance to my scoring process?

Trade credit insurance can play a key role in your credit risk evaluation process. By integrating it into your scoring system, you can better protect your business against potential losses due to non-payment or insolvency. This approach not only adds an extra layer of protection but also strengthens your overall financial risk management strategy.