Credit underwriting is all about assessing risk – whether it’s for loans, insurance, or trade credit. Today, data drives this process, making decisions faster and more precise. Here’s what you need to know:

- What It Is: Credit underwriting evaluates a borrower or buyer’s ability to meet financial obligations using financial data, payment histories, and market trends.

- Why Data Matters: Traditional credit scores fall short. Alternative data and AI tools now offer real-time insights, improving accuracy and detecting risks months in advance.

- Key Metrics: Metrics like Debt-to-Income Ratio (DTI), Credit Utilization, and Probability of Default (PD) shape underwriting decisions.

- Data Sources: Internal records, external credit bureaus, and alternative data (e.g., cash flow, BNPL behaviors) provide a full picture of creditworthiness.

- Technology’s Role: AI models, real-time data platforms, and tools like Alloy streamline decisions and uncover risks traditional methods miss.

- Credit Insurance: Focuses on buyers’ financial health to protect businesses from defaults, with dynamic coverage limits based on real-time data.

Using diverse data sources and modern tools, lenders and insurers can better assess risk, set appropriate credit limits, and support financial growth while minimizing exposure.

Data-Driven Revolution in Underwriting: AI meets Credit

sbb-itb-b840488

Key Data Sources in Credit Underwriting

Credit underwriters rely on three primary types of data: internal records, external reports, and newer alternative sources that capture financial behaviors often overlooked by traditional credit files. Combining these categories provides a deeper, more accurate understanding of creditworthiness, empowering underwriters to create comprehensive risk profiles.

Internal Data Sources

Internal data offers insights from existing customer records, such as credit applications, payment history, and transaction data. Payment history serves as a cornerstone, revealing patterns like on-time payments, past defaults, or invoice settlement speeds – all of which help shape a customer’s risk profile. Transaction data adds another layer, uncovering spending habits such as cash-to-total spend ratios, transaction frequency, and preferred retailers. By analyzing raw transaction data instead of monthly summaries, lenders can uncover up to 30 times more predictive features.

Banks and insurers also use internal risk ratings, which blend quantitative metrics with qualitative insights for regulatory purposes. Insurers, for instance, analyze historical claims data to spot trends and risks specific to their portfolios. Many lenders rely on "behavior scorecards" to track customer risk over time, enabling them to adjust credit lines or identify cross-selling opportunities based on account performance. Notably, 99% of lenders incorporating credit risk models also use credit scores, while 49% monitor their models monthly or quarterly to ensure accuracy.

While internal data provides a strong foundation, external reports add another critical perspective.

External Data Sources

Traditional credit bureau reports remain a staple in assessing creditworthiness. However, they often miss key details. This is where alternative credit data – regulated under the Fair Credit Reporting Act (FCRA) – comes into play. FCRA-regulated data must be displayable, disputable, and correctable, ensuring transparency and fairness.

Underwriters can access external data from sources like specialized credit bureaus (e.g., Experian‘s Clarity Services for alternative financial data or RentBureau for rental history), consumer-permissioned bank account data, public records (e.g., property deeds or licenses), and third-party providers like rent collection companies. The results can be transformative. For example, in 2020, Atlas Credit partnered with Experian to develop a custom underwriting model using alternative data, which enabled them to nearly double loan approvals while reducing portfolio risk by 15% to 20%. Even integrating cash flow data alone can improve predictive accuracy by 40% compared to standard models.

"Alternative credit data, also known as expanded FCRA-regulated data, is data that can help you evaluate creditworthiness but isn’t included in traditional credit reports." – Laura Burrows, Experian Insights

Emerging Data Trends

Beyond traditional sources, emerging trends are reshaping credit evaluations. Lenders are increasingly adopting real-time assessments using consumer-permissioned financial account data. This approach gives access to live information about income, assets, and cash flow. Additionally, Buy Now Pay Later (BNPL) data is gaining traction, offering insights into short-term credit behaviors like payment and return histories that standard reports often overlook. Behavioral metadata, such as mobile device usage patterns, is also being used to score individuals without any prior credit history.

These innovations aim to improve financial inclusion. In the U.S., 28 million adults lack mainstream credit files, and another 21 million remain unscorable using traditional models. Advanced tools like Experian’s Lift Premium™ can now score 96% of U.S. adults, compared to just 81% under conventional methods. Even individuals with Individual Taxpayer Identification Numbers (ITINs) demonstrate strong credit stability, with 76.9% staying current on trades after 12 months – 15% higher than those with Social Security Numbers.

To leverage these advancements effectively, lenders should focus on automating underwriting processes to handle alternative data, conducting regular audits for compliance, and employing explainable AI to ensure transparency in credit decisions.

Next, we’ll dive into best practices for using these diverse data sources to their full potential.

Analyzing Data for Credit Risk Assessment

After collecting data from internal records, external credit bureaus, and new data sources, the next step is to transform this information into actionable insights for assessing credit risk. This requires focusing on key metrics, applying effective analysis techniques, and avoiding pitfalls that could skew results. Understanding these metrics is crucial for accurate analysis.

Key Metrics for Credit Risk Evaluation

Credit risk evaluation relies on specific metrics rooted in the 5 Cs of Credit, offering a structured way to assess a borrower’s financial standing.

- Debt-to-Income Ratio (DTI): This compares a borrower’s monthly debt payments to their gross income, providing insight into their ability to manage debt.

- Credit Utilization Ratio: This measures the percentage of available credit being used, with higher utilization often indicating financial strain.

- Debt Service Coverage Ratio (DSCR): For businesses, this ratio compares net operating income to total debt obligations, ensuring cash flow is sufficient to cover payments.

- Loan-to-Value (LTV): This assesses whether the value of collateral adequately secures the loan.

- Probability of Default (PD): This metric quantifies the likelihood of a borrower defaulting on their obligations within a specific period, typically one year.

Traditional credit scores also play a role, with five components weighted as follows: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Breaking down these scores helps pinpoint specific weaknesses, such as a short credit history, which might not be relevant for certain loan types.

Data Analysis Techniques in Underwriting

To turn raw data into actionable insights, underwriters use a mix of traditional and advanced analytical methods.

- Logistic regression is popular due to its simplicity and compliance with regulatory standards, drawing clear distinctions between low- and high-risk borrowers.

- Advanced methods like Random Forests and Gradient Boosting (XGBoost) excel at identifying complex patterns in large datasets, uncovering low-risk applicants who might otherwise be overlooked.

- Neural networks are powerful for capturing intricate relationships but often lack transparency. Tools like SHAP (SHapley Additive exPlanations) and LIME make these models more interpretable.

The impact of these techniques is substantial. For example, 62% of businesses report that AI and machine learning are transforming their operations, including underwriting. Validation metrics such as the Area Under ROC Curve (AUC) and the Kolmogorov-Smirnov (KS) statistic are used to ensure models effectively differentiate between "good" and "bad" borrowers. Preprocessing steps like Winsorization (limiting outliers) and log-transformation for skewed data ensure analysis accuracy.

"Data is the lifeblood of credit risk analytics. It enables lenders to assess the creditworthiness of potential borrowers, monitor the performance of existing loans, and make informed decisions." – FasterCapital

Despite these advanced methods, challenges like data imbalance and model drift require continuous attention.

Challenges in Data Analysis

Even with robust techniques, data analysis in credit risk assessment isn’t without hurdles.

- Data sparsity and imbalance: Defaults are often rare compared to non-defaults, making it difficult for models to identify high-risk borrowers. Techniques like SMOTE and class weighting address this issue.

- Model bias: Training data can unintentionally introduce bias, leading to discriminatory outcomes. As Julie Lee from Experian explains, "Lenders have a regulatory and moral imperative to remove biases from their lending decisions. They need to beware of how biased training data could influence their credit risk models".

- Model drift: Economic shifts or changing consumer behaviors can make older models less accurate. Regular recalibration is essential, especially when PD drift exceeds 10%, as even a 1% error in PD can lead to significant financial consequences for lenders.

- Balancing interpretability and performance: Advanced models often deliver better accuracy but lack transparency. Choosing the right model involves weighing regulatory compliance against business goals.

These challenges highlight the need for vigilance and adaptability in credit risk analysis, ensuring models remain both accurate and fair over time.

Best Practices for Data Collection and Management

Turning raw data into actionable underwriting insights hinges on effective data management. Without consistent oversight, even the most advanced models can produce unreliable results. For instance, about 2.1% of contact information becomes outdated within just one month if not maintained. This highlights the need for ongoing data quality efforts instead of treating it as a one-time task. By following these practices, underwriters can ensure their decisions are built on a solid data foundation.

Ensuring Data Accuracy and Consistency

A structured approach to quality control is key to maintaining reliable data. Organizations can follow a six-step plan: review governance, correct errors, audit data, evaluate disputes, benchmark metrics, and update policies. Regular audits help catch and fix mistakes before they impact decisions, while benchmarking against peers can uncover gaps or anomalies that internal reviews might overlook.

Another critical task is monitoring for model drift. While 49% of lenders check for drift monthly or quarterly, only 10% use automated alerts to flag when their credit models lose predictive power. This oversight can be risky since shifting economic trends or consumer behaviors can undermine a model’s effectiveness over time. Before introducing new data sources or models, backtesting against historical data ensures they perform as expected and minimizes the chances of costly errors.

Compliance with Data Privacy Regulations

Managing sensitive underwriting data also requires strict compliance with federal regulations. For example, the Fair Credit Reporting Act (FCRA) mandates that businesses supplying data to credit bureaus maintain written policies to ensure accuracy. Under the FCRA Furnisher Rule, companies have 30 days to investigate and resolve consumer disputes about data accuracy, with fines reaching $4,983 per violation starting in January 2025.

The Gramm-Leach-Bliley Act (GLBA) further requires financial institutions to provide clear, plain-language privacy notices when a customer relationship begins and annually thereafter. It also requires businesses to offer simple ways for consumers to opt out of data sharing – options like toll-free numbers or checkboxes are acceptable, but formal letters are not. Adding to the complexity, 20 states will have comprehensive data privacy laws in place by early 2025. Securely disposing of outdated information, such as shredding physical documents or destroying electronic media, is equally important. Following these regulations not only protects consumers but also strengthens the overall data management framework.

Using Technology for Data Management

Modern tools make managing data simpler and more efficient. Platforms like Alloy and HES LoanBox integrate processes like Know Your Customer (KYC), fraud detection, and credit evaluations into a single dashboard, enabling seamless automated workflows. These systems use APIs to pull real-time data from both traditional sources (like Equifax, Experian, and TransUnion) and emerging providers (such as Plaid, Argyle, and Nova Credit).

For example, in 2026, the real estate fintech Jetty partnered with Alloy, automating document verification and identity checks. This led to a 35% increase in pre-approval rates while cutting decision times to under 10 minutes. Similarly, Earnest boosted its automated approval rate by 56% by incorporating alternative data, like education and employment history, alongside traditional credit scores through Alloy.

"Alloy connects us to more data sources, which helps us increase the speed at which we’re able to give applicants a decision." – Jun Cho, Senior Product Manager at Earnest

No-code and low-code platforms like ACTICO and CloudBankin empower risk teams to tweak credit policies and models without heavy reliance on engineering resources. Additionally, real-time systems using SQL-based risk models and streaming databases (e.g., Materialize) enable instant cash flow analysis and funding decisions through API-first, modular integration setups. These technologies allow lenders to enrich their data processes step by step, enhancing both speed and accuracy.

The Role of Data in Credit Insurance Underwriting

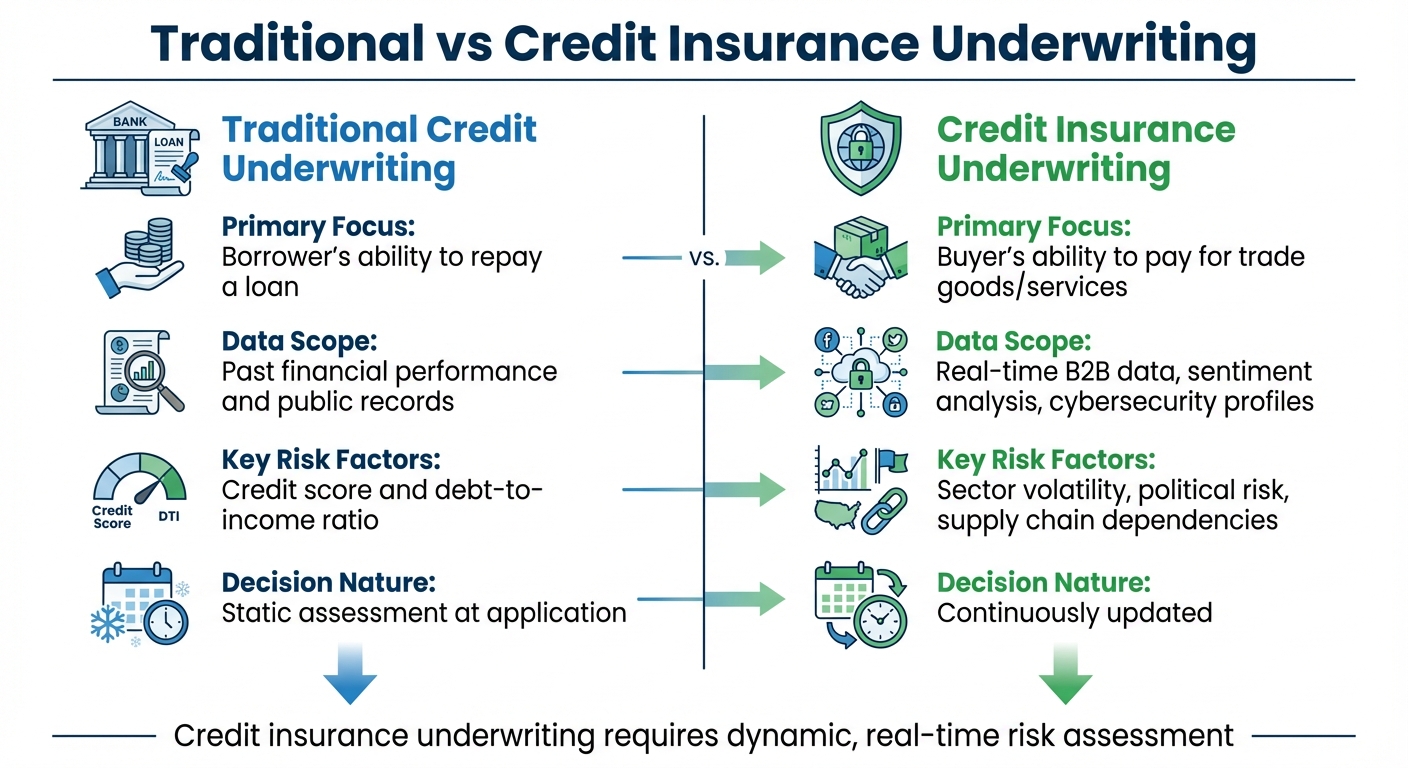

Traditional vs Credit Insurance Underwriting: Key Differences

Using data in credit insurance underwriting allows businesses to better manage risk – a recurring theme in this guide. At its core, credit insurance underwriting evaluates your customers’ creditworthiness, helping protect your cash flow from potential buyer defaults.

How Credit Insurance Underwriting Differs

The main distinction lies in the focus of evaluation. Traditional underwriting looks at your business through the lens of the "4 Cs" – Character, Capacity, Collateral, and Capital. On the other hand, credit insurance underwriting zeroes in on your buyers’ ability to pay for goods and services.

This process requires data on factors like sector volatility, geopolitical shifts, and supply chain risks. For export transactions, additional aspects such as political stability and country-specific risks play a crucial role. Unlike static assessments, credit insurance underwriting is dynamic. Credit limits are reviewed and adjusted regularly to reflect real-time changes in buyer behavior or financial health.

Another unique aspect is the complexity of coverage decisions. For instance, withdrawing coverage can unintentionally signal trouble to other suppliers, prompting them to demand advance payments, which could exacerbate the buyer’s financial strain. This makes the data analysis process more intricate than a straightforward "approve or deny" approach.

| Feature | Traditional Credit Underwriting | Credit Insurance Underwriting |

|---|---|---|

| Primary Focus | Borrower’s ability to repay a loan | Buyer’s ability to pay for trade goods/services |

| Data Scope | Past financial performance and public records | Real-time B2B data, sentiment analysis, cybersecurity profiles |

| Risk Factors | Credit score and debt-to-income ratio | Sector volatility, political risk, supply chain dependencies |

| Decision Nature | Static assessment at application | Continuously updated |

These differences highlight the tailored strategies used to set coverage terms, which will be explored further.

Using Data to Determine Coverage and Premiums

Building on these distinctions, underwriters rely on a mix of quantitative and qualitative data to shape coverage and premium strategies. They analyze financial statements, market trends, and behavioral data to paint a complete picture. This starts with core financial metrics – balance sheets, income statements, and cash flow reports – which reveal critical information like liquidity ratios, debt levels, and working capital.

Payment behavior plays a major role. Underwriters examine how buyers handle invoices by reviewing internal records, trade credit bureau reports, and supplier feedback to spot patterns of late payments or defaults. Additionally, a company’s cybersecurity measures serve as an indicator of its overall risk profile. As Moody’s explains, "a company’s cybersecurity measures – or lack thereof – serve as a barometer for its overall risk profile, influencing its likelihood of default".

AI tools add another layer of precision, identifying warning signs 6 to 8 months before significant credit events for larger firms. Behavioral signals, such as sudden spikes in order volume or reduced communication, are also monitored closely.

This thorough data analysis determines coverage limits and premiums. A credit limit represents the maximum coverage an insurer provides for a specific buyer, striking a balance between supporting business growth and managing risk. Regular updates to this data allow underwriters to adjust coverage limits as needed.

Case Study: Data-Driven Credit Insurance Success

"Underwriters are the backbone of the credit insurance process. Their primary role is to evaluate the creditworthiness of a business’s customers and determine the level of risk associated with insuring those receivables".

Christian Bürger, Senior Editor at Atradius, highlights the importance of collaboration in credit insurance. Businesses that actively engage in the data process see tangible benefits. For example, policyholders who promptly report overdue accounts not only maintain claims eligibility but also help underwriters adjust risk profiles in real time. Many insurers now offer online platforms where businesses can request credit limits, monitor decisions, and track buyer risk profiles as they evolve.

Credit insurance works best as an ongoing partnership. By aligning credit limit requests with actual receivables, sharing detailed buyer transaction histories, and using insurer-provided monitoring tools, businesses can identify and address liquidity issues before they lead to bad debt. This proactive approach turns credit insurance into more than just a safety net – it becomes a strategic tool for sustained growth, demonstrating the power of data in effective credit management.

Conclusion

Data has reshaped credit underwriting, turning it from a backward-looking process into a forward-thinking tool. By incorporating alternative data, models can now evaluate 96% of U.S. adults, a notable increase from the 81% covered by traditional methods. In the realm of credit insurance, AI-powered tools are proving invaluable, detecting warning signs an average of 6 to 8 months before significant credit events occur. This early detection allows businesses to adjust coverage and safeguard receivables more effectively.

The key to success lies in combining diverse data sources – such as financial statements, payment behaviors, cybersecurity measures, and real-time transaction data – rather than depending on a single type of information. As previously mentioned, custom models and integrated data platforms have made a tangible difference, improving approval rates while mitigating risk. These advancements highlight how integrating multiple data layers is transforming credit insurance underwriting.

"The trade credit insurance industry is at a crossroads, with the path forward being paved by technological innovation and a deeper, more comprehensive approach to risk assessment." – Moody’s

This perspective emphasizes the growing importance of dynamic risk assessment. With the shift to real-time evaluations, credit limits no longer need to be static. Regular monitoring and automated credit checks help identify changes in buyer risk profiles early, enabling businesses to act proactively. This approach elevates credit insurance beyond its traditional role as a safety net, positioning it as a tool for growth. It empowers companies to extend credit to new customers confidently while maintaining financial security.

FAQs

What alternative data is most useful for credit insurance decisions?

Alternative data offers a fresh perspective for making credit insurance decisions by tapping into non-traditional sources that reveal a borrower’s financial standing in greater detail. For instance, factors like a company’s web presence, social media activity, press mentions, transaction behaviors, and relevant industry news can paint a more nuanced picture. These insights can uncover potential risks, such as fraud or financial instability, that conventional credit reports might overlook, ultimately refining the precision and reliability of credit underwriting processes.

How do underwriters keep models accurate as the economy changes?

Underwriters rely on advanced data analysis techniques, including alternative data and machine learning, to maintain the accuracy of their models. These tools allow for real-time insights and adjust to economic changes by continuously learning from new data, which enhances predictive precision.

In trade credit insurance, underwriting focuses heavily on forward-thinking analysis. Instead of depending solely on historical trends, this method helps underwriters identify potential economic changes and emerging risks. This proactive approach ensures models remain relevant and effective in dynamic markets.

How is a buyer’s credit limit adjusted in real time?

When it comes to a buyer’s credit limit, lenders rely on real-time financial data to make adjustments. This means a buyer’s credit limit isn’t static – it changes instantly based on factors like current cash flow, recent payment behavior, and other evolving financial indicators. By continuously updating this information, lenders can ensure their credit decisions align with the buyer’s latest financial status.