When offering credit to business customers, you face risks beyond their payment habits. Economic downturns, currency fluctuations, and industry-specific challenges can turn reliable clients into liabilities, threatening cash flow and growth.

Key risks include:

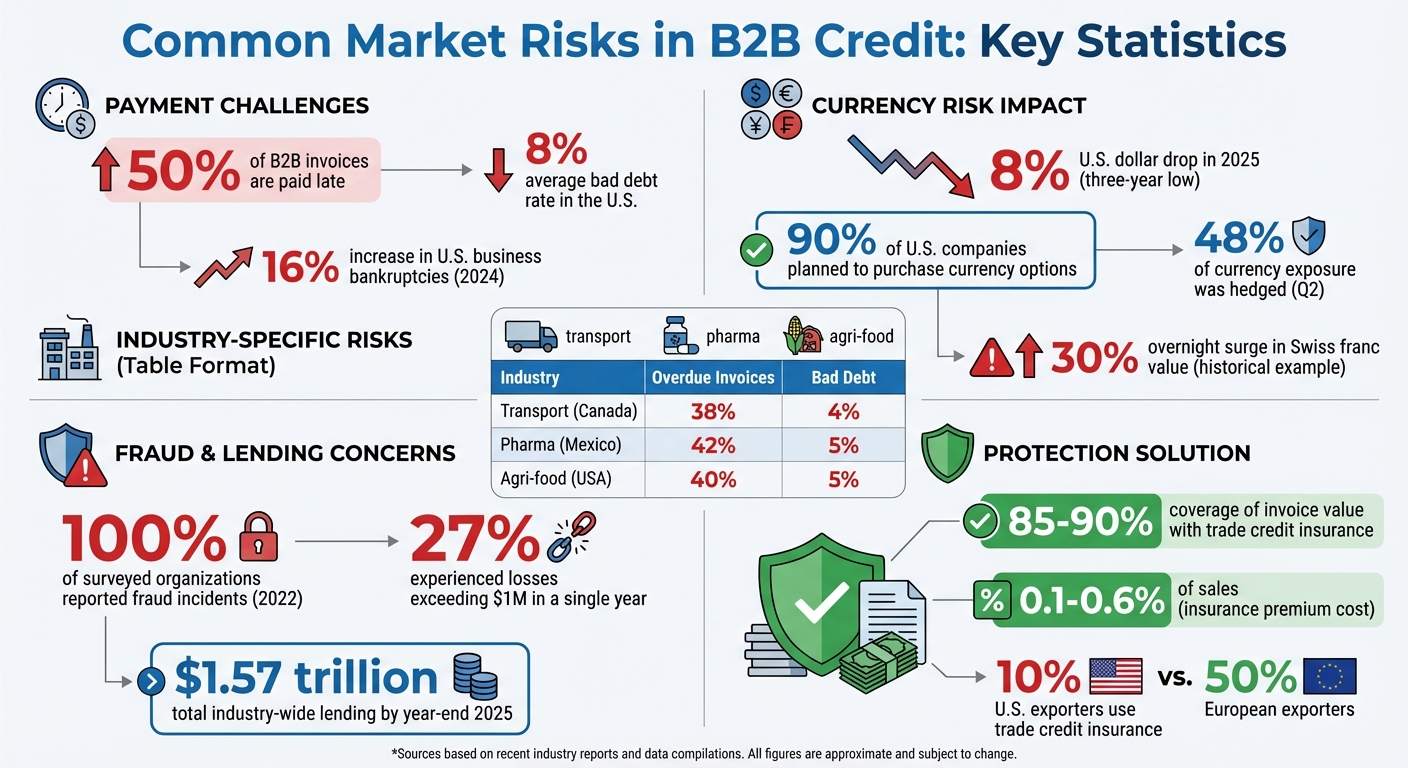

- Late Payments: Almost 50% of B2B invoices are paid late, with bad debts averaging 8% in the U.S.

- Economic Pressures: Rising interest rates and recessions have driven a 16% increase in U.S. business bankruptcies (2024 data).

- Currency Risks: Exchange rate volatility can shrink profits and push customers toward insolvency.

- Industry-Specific Risks: Sectors like chemicals, transport, and agri-food face unique payment challenges.

- Customer Concentration: Over-reliance on a few key clients amplifies financial exposure.

To manage these risks, businesses can:

- Use credit monitoring tools to track customer financial health.

- Set flexible credit limits based on real-time data.

- Protect receivables with trade credit insurance, which covers up to 90% of losses from non-payment.

These strategies help safeguard cash flow, reduce exposure, and support long-term stability in unpredictable markets.

Key B2B Credit Risk Statistics and Market Trends 2024-2025

Vendor Credit Risk Analysis: 5 C’s of Credit and How They Affect Your Business

sbb-itb-b840488

Common Market Risks in B2B Credit

Market risks affect your entire portfolio in ways that diversification can’t fully protect against. Unlike risks tied to specific companies, these challenges hit across the board, impacting everyone simultaneously. Being aware of these risks can help you anticipate disruptions that might turn reliable customers into payment liabilities. Here’s a closer look at some of the most pressing market risks.

Currency Exchange Risk

Currency fluctuations can erode revenue even when customers pay on time. A major issue here is transaction risk, which arises from the time lag between agreeing on a price and receiving payment. If the foreign currency weakens during this period, the amount you receive in U.S. dollars could fall short of expectations, eating into your profit margins. In some cases, sharp devaluation of local currencies can even push customers toward insolvency when they can’t meet their dollar-based obligations.

For example, in 2025, the U.S. dollar dropped by over 8%, hitting a three-year low due to tariff uncertainties and recession fears. Such volatility forces businesses to act. Surveys revealed that 90% of U.S. companies planned to purchase more currency options to hedge against foreign exchange (FX) risks, and 48% of currency exposure was hedged in the second quarter, up from 46% in the previous quarter.

Currency swings are often driven by factors like government monetary policies, inflation, and geopolitical instability. A striking example occurred when the Swiss National Bank unpegged the Swiss franc from the euro, causing a 30% overnight surge in the franc’s value. This highlights just how quickly currency markets can shift, leaving businesses vulnerable.

Industry Volatility Risk

Sector-specific disruptions can cripple a customer’s ability to pay, no matter how dependable they’ve been in the past. Factors like technological advancements, regulatory changes, and supply chain issues can all impact liquidity and payment capacity. Different industries and regions experience these challenges in unique ways, as the table below illustrates:

| Sector | Region | Overdue Invoices (% of Credit Sales) | Bad Debt Write-offs (%) | Primary Risk Drivers |

|---|---|---|---|---|

| Transport | Canada | 38% | 4% | Liquidity bottlenecks |

| Pharma | Mexico | 42% | 5% | Customer liquidity constraints |

| Agri-food | USA | 40% | 5% | Input cost volatility, tariffs |

Technological changes can also render entire business models obsolete. For instance, the rise of driverless vehicles is forcing insurance companies to rethink liability and risk structures. Similarly, new models like "Equipment-as-a-Service" (EaaS) are challenging traditional financing options, exposing gaps in risk management strategies. As Jamie Dimon, CEO of JPMorgan Chase, put it:

"When you see one cockroach, there are probably more".

This serves as a reminder that visible problems in one area often hint at deeper, systemic challenges.

Economic Downturn Risk

Broader economic trends, like recessions or inflation, create additional stress on payment reliability. These forces can lead to payment delays and customer bankruptcies, as seen in the 16% increase in U.S. business bankruptcies and the 50% rate of late payments discussed earlier. Macroeconomic pressures squeeze profit margins, making it harder for customers to meet their obligations.

Interest rate volatility and geopolitical events – such as the war in Ukraine – can further complicate matters. For example, bank loans to non-deposit financial institutions reached $1.14 trillion in 2025, with total industry-wide lending climbing to $1.57 trillion by year-end. This concentration of lending poses systemic risks during economic downturns.

Concentration and Global Expansion Risk

Customer concentration adds another layer of risk. Relying heavily on a few key clients amplifies the impact of any financial trouble they face. If even one major customer struggles during an economic or currency crisis, the ripple effects can severely damage your accounts receivable.

Expanding into global markets also introduces complexities. Navigating unfamiliar regulations, currency risks, and payment practices can be challenging. For instance, some currencies, like the South Korean won (KRW) or Chinese yuan (CNY), are "partially convertible", meaning government restrictions may limit capital flows. Political instability or sudden policy changes can cause abrupt devaluations, as seen in past defaults in Argentina or market volatility in Turkey. These factors directly influence credit decisions and the structuring of payment terms with international buyers.

How to Reduce Market Risks in B2B Credit

Reducing market risks in B2B credit requires a proactive approach. By combining thorough credit evaluations, flexible credit management, and strategic insurance options, businesses can better safeguard themselves against uncertainties.

Conducting Creditworthiness Checks

Regular credit assessments are essential to predict and address payment challenges. Credit insurers maintain extensive databases that track payment behaviors for millions of companies worldwide. These resources go beyond internal records, offering insights into financial health indicators like debt-to-equity ratios and cash flow, as well as external risks such as trade sanctions, currency issues, and political instability in a customer’s region.

Continuous monitoring is key. As Command Credit emphasizes:

"Credit risk management is an ongoing process that requires monitoring and regular reviews. In business, conditions can change quickly, and what was a good risk yesterday may be a bad risk today".

To stay ahead, set up automated alerts for declining credit scores or overdue payments. Request updated financial statements regularly to ensure your credit terms align with your customers’ current financial situations.

Setting Dynamic Credit Limits

In an unpredictable market, static credit limits often fall short. Dynamic limits, which adapt based on real-time data like payment history and financial health, provide a more flexible solution. Automated platforms now make it easier to customize credit limits and payment terms – whether it’s 30, 60, or 90 days – and adjust them instantly during the sales process.

The Resolve Team highlights the benefits of automation:

"Automated systems and credit management software can significantly improve the efficiency and accuracy of these processes, helping businesses quickly assess credit risk and monitor accounts receivable".

In addition to leveraging automation, diversify your credit exposure by capping the total credit allocated to individual customers or industries. Stress testing your credit portfolio can help you understand how market fluctuations might affect customers’ ability to repay. Fraud remains a pressing concern, with 100% of surveyed organizations reporting incidents in 2022, and 27% experiencing losses exceeding $1 million in a single year. These numbers underscore the importance of active credit limit management.

For added protection, trade credit insurance provides a reliable way to transfer risk.

Using Trade Credit Insurance

Trade credit insurance shifts the burden of non-payment risks to an insurer, covering both commercial risks – like customer bankruptcy or delayed payments – and political risks, such as currency restrictions or trade disruptions. If a covered customer defaults, the insurer typically reimburses 85% to 90% of the invoice value. This safeguard is especially relevant as U.S. business bankruptcy filings rose 16% in the year ending June 30, 2024, and nearly half of all B2B invoices are paid late.

This type of insurance also promotes growth by allowing businesses to confidently extend credit to new customers or operate in uncertain markets. Additionally, credit-insured receivables can be used as collateral to secure better financing terms or higher credit lines from lenders. Many modern insurance policies now include digital tools and APIs for real-time monitoring of buyer creditworthiness, providing alerts about risk changes before problems escalate.

The cost of trade credit insurance is relatively low, with premiums ranging from 0.1% to 0.6% of covered sales. Compare this to self-insurance, which requires cash reserves for bad debts while leaving businesses fully exposed to risk. Here’s a quick comparison:

| Feature | Trade Credit Insurance | Self-Insurance |

|---|---|---|

| Risk Transfer | Covers 85%–90% of risk | Retains 100% of risk |

| Cost | 0.1%–0.6% of sales | No premium; risk of high losses |

| Capital Impact | Frees up capital for growth | Ties up cash in reserves |

| Expertise Access | External credit assessments | Relies on internal resources |

| Cash Timing | Compensation after default (60–90 days) | No reimbursement |

Interestingly, only 10% of U.S. exporters use trade credit insurance, compared to 50% of their European counterparts. This disparity highlights a significant opportunity for American businesses to better protect themselves and explore new markets with confidence.

Protection and Growth with CreditInsurance.com

CreditInsurance.com is designed to simplify the often-complicated world of B2B credit risk management. It provides businesses with straightforward guides on credit insurance, explaining covered risks and how to choose the right protection. Whether you’re working with domestic clients or expanding into international markets, the platform offers insights on safeguarding your accounts receivable against non-payment, insolvency, and political unrest. This knowledge lays the groundwork for exploring customized solutions that reduce risk while supporting business growth.

But the platform isn’t just about education – it also offers tailored credit insurance solutions to match your business’s specific needs. These solutions protect against commercial risks, like customer bankruptcy, and political risks, such as currency restrictions. Premiums are calculated based on factors like your industry, the makeup of your debtor pool, and the features you want in a policy. This ensures businesses get the right coverage for their risk profile without paying for unnecessary extras.

Credit insurance also opens doors to growth opportunities. By making your receivables more appealing to banks, it can help secure better financing terms. This, in turn, enables you to take on larger deals and explore new markets with confidence.

To support businesses further, CreditInsurance.com offers a resource center packed with practical tools and information. From FAQs and case studies to a detailed glossary, these resources tackle common misunderstandings and provide clear, actionable insights. For instance, they explain the drawbacks of self-insuring, such as tying up capital and leaving yourself fully exposed, compared to transferring risk to an insurer. With the B2B marketplace projected to grow at a 20% compound annual growth rate through 2028 and already surpassing $17 trillion in transaction volume as of 2023, having a solid risk protection strategy is more important than ever.

For companies frustrated by slow, manual credit checks, CreditInsurance.com highlights modern tools that streamline the process. These solutions integrate automated risk assessments into your workflow, letting you quickly verify creditworthiness, set flexible payment terms during sales discussions, and continuously monitor your customers’ financial health – all while safeguarding your cash flow.

Conclusion

The B2B credit market comes with its fair share of challenges – currency shifts, industry instability, economic slumps, and over-reliance on a few customers can all disrupt even the most stable businesses. On top of that, poor cash flow management and late payments, as highlighted earlier, remain pressing concerns.

Staying ahead of these risks requires a proactive approach. By leveraging continuous credit monitoring and setting flexible exposure limits, you can spot early warning signs when a previously dependable customer starts to pose a risk. But when internal strategies fall short, external solutions become a necessity.

This is where trade credit insurance steps in. For as little as 0.1% to 0.6% of covered sales, it offers a safety net against major financial losses while allowing you to maintain strong customer relationships. It also supports the flexible payment terms that 85% of B2B buyers prefer and bolsters your balance sheet, making it easier to secure financing.

At CreditInsurance.com, the focus is on making protection accessible. They offer educational tools, fast credit checks, and tailored solutions to meet your specific needs. In today’s fast-changing business environment, having a robust protection plan isn’t a luxury – it’s a necessity for long-term success.

FAQs

How can I tell if a customer is becoming a higher credit risk?

Keep an eye out for warning signs such as late payments, a noticeable drop in financial stability, or unfavorable updates on credit reports. These red flags might suggest a higher chance of default or financial trouble. By staying alert to these patterns, you can take steps early to address and manage potential risks effectively.

What’s the best way to set credit limits when markets change fast?

Navigating rapidly shifting markets requires a smart approach to credit limits. Enter dynamic risk management – a strategy that keeps you ahead of the curve. Here’s how you can do it:

- Regular Reviews: Keep credit limits aligned with the latest data. This means analyzing real-time market shifts, customer financial stability, and broader economic trends regularly.

- Automation: Leverage tools that track risk signals automatically. These systems can help you make quicker, data-driven credit decisions without sacrificing accuracy.

- Flexible Policies: Build adaptability into your credit policies. Flexibility ensures you’re prepared to respond quickly to market changes.

- Proactive Communication: Periodically check in with your customers. By staying in touch, you can spot and address potential risks before they escalate.

Dynamic risk management isn’t just about reacting – it’s about staying a step ahead.

When does trade credit insurance make sense for my business?

Trade credit insurance provides a safety net for businesses that extend net terms to their customers. By protecting against the risk of non-payment due to customer insolvency or payment delays, it helps maintain steady cash flow and minimizes financial uncertainty. This type of coverage can be particularly useful for businesses aiming to shield themselves from potential losses tied to unpaid invoices.