Global trade disputes can disrupt your cash flow, inflate costs, and create financial uncertainty. Insurance can help mitigate these risks, ensuring stability during international trade challenges. Here’s a quick breakdown of the key options:

- Trade Credit Insurance: Protects against customer non-payment, covering risks like insolvency or delayed payments. Costs typically less than 1% of insured sales and can recover 75%-95% of invoice value.

- Political Risk Insurance: Shields businesses from losses due to government actions, such as expropriation or trade embargoes. Average cost is about 1% of the coverage limit.

- Accounts Receivable Insurance: Safeguards cash flow by covering unpaid invoices, including risks like bankruptcy or political disruptions. Premiums range from 0.1%-0.4% of total sales.

Each option addresses specific challenges, from buyer defaults to geopolitical risks. Choosing the right mix depends on your trade regions, customer base, and risk exposure. For more tailored advice, consult an insurance expert.

Trade Insurance Options Comparison: Coverage, Costs, and Key Features

1. Trade Credit Insurance

Coverage Scope

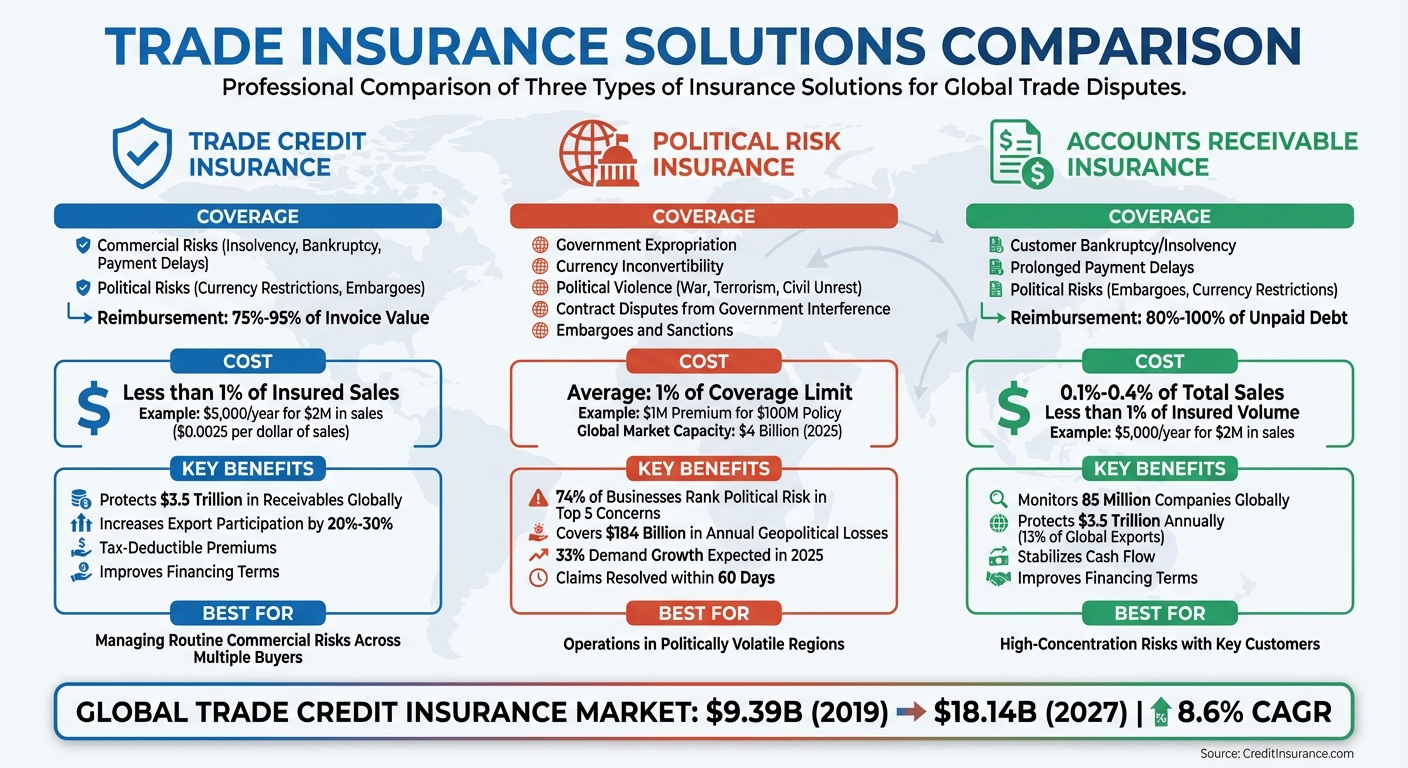

Trade credit insurance helps protect businesses from losses when buyers fail to pay, covering two primary types of risks: commercial risks (like insolvency, bankruptcy, or extended payment delays) and political risks (such as currency restrictions, government expropriation, or trade embargoes). If a covered event occurs, insurers usually reimburse between 75% and 95% of the invoice value. For instance, if a buyer defaults on a $100,000 invoice, the policyholder could recover $75,000 to $95,000. Globally, trade credit insurers protect over $3.5 trillion in receivables each year, equating to about 13% of worldwide merchandise exports.

However, it’s essential to note that trade credit insurance does not cover disputed invoices. Any disputes must be resolved before filing a claim. As Jason Benson, Global Head of Structured Working Capital at J.P. Morgan, explains:

"If there’s a receivable for 100 products, and the buyer says only 80 were delivered, the insurer’s payment obligation may only be on the undisputed amount".

Risk Mitigation Features

Trade credit insurers actively monitor buyers’ creditworthiness and adjust risk assessments as needed. Many policies also include professional debt collection services, which operate across different time zones and currencies. These services can help businesses work out payment plans with customers experiencing temporary cash flow issues, reducing exposure to trade disputes. For domestic debts, claims are typically paid within 60 days. International claims, especially those involving political risk assessments, may take longer.

Cost Efficiency

The cost of trade credit insurance is relatively low, typically less than 1% of the insured sales volume. For example, a company with $2 million in annual sales might pay approximately $5,000 per year for coverage, or about $0.0025 per dollar of sales. As the International Chamber of Commerce states:

"Credit insurance is no longer merely a contingency tool, but a strategic asset that sustains trade continuity and enables firms to pursue growth with confidence".

Premium costs vary depending on factors like a company’s debt history, customer credit profiles, and the overall health of its industry. Additionally, insured receivables can help businesses secure better financing terms from banks, potentially lowering the overall cost of capital. Studies show that access to credit insurance can increase a company’s export participation by 20% to 30%, particularly in emerging markets. Beyond the financial benefits, this insurance offers a safety net during defaults linked to trade disputes.

Applicability to Trade Disputes

When trade disputes arise, trade credit insurance helps mitigate the financial fallout from buyer defaults. While it doesn’t resolve disputes, it addresses the financial risks they create. For instance, if tariffs lead to a buyer’s insolvency, the insurance covers the resulting losses, allowing businesses to continue offering competitive open-account terms instead of requiring cash prepayments. The demand for this coverage has grown, especially following recent U.S. trade policy changes. For example, reciprocal tariffs as high as 105% on certain imports in 2025 have prompted more businesses to seek protection against buyer defaults caused by sudden price hikes.

According to ICISA:

"In the absence of trade credit insurance many trade transactions would have to be done on a pre-paid or cash basis, or not at all".

This flexibility is particularly valuable during economic downturns. The insurance acts as a financial buffer, supporting export continuity and serving as a key component of broader risk management strategies for navigating disruptions in international trade.

sbb-itb-b840488

2. Political Risk Insurance

Coverage Scope

Political Risk Insurance (PRI) helps businesses protect themselves from losses caused by unfavorable government actions or political turmoil that can disrupt international trade. It typically addresses risks like expropriation (when assets are seized or nationalized), currency inconvertibility (the inability to exchange local currency or repatriate profits), political violence (including war, terrorism, and civil unrest), and contract disputes caused by government interference. PRI also covers trade-specific challenges such as wrongful calls on performance guarantees, license cancellations, and losses due to embargoes or sanctions. Some policies even extend to "arbitral award default" and "denial of justice", which apply when governments fail to honor court rulings.

A notable example of this is the case of AerCap, the world’s largest commercial aircraft owner. In June 2025, the High Court in London ruled in its favor, awarding over $1 billion in a "war risks" insurance dispute. This case involved aircraft stranded in Russia following the Ukraine invasion, highlighting the importance of PRI in managing complex global risks.

Risk Mitigation Features

Today’s PRI policies include tailored endorsements to address evolving risks in trade. For example, Pre-Shipment endorsements cover manufacturing costs for custom goods if a government action, such as a ban or license cancellation, disrupts shipment. These endorsements typically reimburse manufacturing expenses along with a small profit margin. Claims under EXIM programs are often resolved within 60 days.

When goods are already in transit and trade disruptions arise, insurers may assist businesses in diverting shipments to alternative markets to limit financial losses. As Joseph D. Jean and Meaghan C. Murphy from Pillsbury note:

"A single embargo, port closure, regulatory sanction or cross-border conflict can trigger a chain reaction – crippling revenue and straining operations".

This proactive approach helps companies navigate unexpected challenges while maintaining operational stability.

Cost Efficiency

On average, PRI policies cost about 1% of the total coverage limit. For instance, a $100 million policy would generally require an annual premium of around $1 million. However, adding specific protections, such as Pre-Shipment endorsements or SRCC (Strikes, Riots, and Civil Commotions) coverage, can increase costs. In 2025, the global PRI market capacity reached nearly $4 billion, with private insurers contributing $2.23 billion and Lloyd’s of London providing $1.75 billion. These figures reflect the growing importance of PRI in managing trade risks during uncertain times.

Applicability to Trade Disputes

Unlike trade credit insurance, which focuses on securing receivables, PRI is designed to protect against government actions and geopolitical disruptions. With rising economic nationalism and shifting U.S. policies, political risk has become a concern across industries. A 2025 survey revealed that 74% of global businesses ranked political risk among their top five enterprise concerns, and 18% reported significant losses in 2023 that required earnings restatements. The demand for PRI is expected to grow by 33% in 2025, fueled by global instability and tariff uncertainties.

The NAIC emphasizes:

"Political risk insurance (PRI) is defined as a tool for businesses to mitigate and manage risks arising from the adverse actions – or inactions – of governments".

Geopolitical issues cost businesses an estimated $184 billion annually, underscoring the critical role PRI plays in managing trade disputes and ensuring business resilience.

3. Accounts Receivable Insurance

Coverage Scope

Accounts Receivable Insurance (ARI) is designed to protect businesses when customers fail to pay their invoices. It covers commercial risks like bankruptcy, insolvency, or prolonged delays in payment deadlines. For businesses involved in global trade, ARI also extends to political risks, such as trade embargoes, currency transfer restrictions, wars, riots, or government actions that prevent buyers from meeting their payment obligations.

Typically, these policies reimburse between 80% and 100% of the unpaid debt. For instance, businesses insured through the Export‐Import Bank of the United States can recover 85% to 95% of the invoice value if a buyer defaults. Additionally, insurers provide real-time credit insights, monitoring over 85 million companies globally. As Kirk Elken, Co-founder of Securitas Global Risk Solutions, puts it:

"Accounts receivable insurance and trade credit insurance both turn vulnerable receivables into protected assets".

Risk Mitigation Features

ARI offers more than just claim payouts. Businesses can select from various coverage options, including Whole Turnover, Key Accounts, Single Buyer, or Transactional policies.

By stabilizing cash flow, ARI enables businesses to offer competitive open account terms and reduces the need for costly litigation, thanks to built-in debt collection services. This type of insurance can also significantly boost export participation – by as much as 20% to 30% in emerging markets. These features make ARI an essential tool for navigating trade disputes and managing market fluctuations.

Cost Efficiency

One of the most appealing aspects of ARI is its affordability. Premiums typically cost less than 1% of the insured sales volume. For example, a business with $2 million in annual sales might pay a $5,000 premium – equivalent to about one-quarter of a cent per dollar of total sales. Rates generally fall between 0.1% and 0.4% of total sales.

Insured receivables are also considered lower-risk by financial institutions, making it easier for businesses to secure working capital loans or negotiate better financing terms.

Applicability to Trade Disputes

While ARI policies provide robust protection, they generally exclude coverage for invoices under dispute until those disputes are resolved. This makes it crucial for businesses to focus on mediation or dispute resolution to activate their coverage.

Despite this limitation, ARI remains a vital tool for managing risks in global trade. Trade credit accounts for roughly 80% to 85% of all short-term trade finance worldwide, and insurers collectively protect over $3.5 trillion in receivables annually – about 13% of global merchandise exports. To put it in perspective, for a business with a 5% profit margin, a $100,000 default could require an additional $2 million in sales just to recover the lost profit. This underscores ARI’s importance in mitigating financial risks tied to trade and supporting international business stability.

For more information on how accounts receivable insurance can help manage trade risks and improve financing strategies, visit CreditInsurance.com.

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

Advantages and Disadvantages

Every insurance solution comes with its own set of strengths and limitations, making it essential to understand which option aligns best with your business needs.

Trade Credit Insurance (TCI) provides protection against commercial risks like bankruptcy and insolvency. It can encourage sales growth and improve financing terms since insured receivables are often seen as lower-risk collateral by banks. Additionally, premiums for TCI are tax-deductible. However, TCI doesn’t typically cover political risks, such as government-related disruptions, unless paired with a separate Political Risk Insurance (PRI) policy. This can add extra cost and complexity.

Political Risk Insurance (PRI) focuses on risks tied to government actions, such as trade embargoes, war, expropriation, and political instability. It’s especially critical for businesses operating in regions with uncertain political climates. That said, PRI doesn’t cover commercial insolvency, and its premiums can vary significantly depending on the region, often making it a pricier option compared to TCI.

Accounts Receivable Insurance (ARI) is designed to protect liquid assets from payment defaults, helping stabilize cash flow. However, ARI coverage is often restricted to specific buyers or buyer groups. Additionally, disputed invoices aren’t covered until the dispute is resolved, which can delay claims.

Here’s a quick comparison of the strengths and weaknesses of these solutions:

| Insurance Type | Key Strengths | Main Weaknesses |

|---|---|---|

| Trade Credit Insurance | Cost-efficient (typically <1% of sales); supports sales growth; improves financing terms; tax-deductible premiums | May require separate PRI for political risks; limited to specific credit limits per buyer |

| Political Risk Insurance | Essential for operations in volatile regions; covers government interference and sovereign defaults | Excludes commercial insolvency; premiums vary widely by region; generally more expensive than TCI |

| Accounts Receivable Insurance | Protects cash flow; stabilizes liquid assets; helps retain nearly 100% of customers | Limited to specific buyers; excludes disputed invoices until resolved |

The global trade credit insurance market was valued at $9.39 billion in 2019 and is expected to grow to $18.14 billion by 2027, with a compound annual growth rate of 8.6%. This growth reflects increasing demand, driven by shifting market conditions. Factors like tariff volatility and geopolitical risks have led insurers to tighten coverage limits, making it even more critical to select the right mix of insurance solutions for your business. For expert advice on choosing the best insurance for your trade operations, visit CreditInsurance.com.

Conclusion

When selecting insurance, it’s important to consider your operating regions, customer base, and the specific risks your business faces. If your main concern is financial losses due to customer insolvency or late payments across a large group of buyers, Trade Credit Insurance provides a practical option. It’s particularly useful for managing routine commercial risks, like bankruptcy, but additional coverage may be needed if you operate in areas prone to instability.

For companies exposed to risks like expropriation, currency inconvertibility, political violence (including war and terrorism), or arbitration award defaults, Political Risk Insurance becomes essential. While premiums can vary by region, this type of policy offers critical protection for businesses in politically unstable environments.

On the other hand, Accounts Receivable Insurance is ideal for addressing high-concentration risks. If a significant portion of your revenue depends on one or two key customers, this coverage shields you from losses if those customers file for bankruptcy or undergo restructuring. It’s a focused solution that fills gaps left by broader insurance policies.

To decide what’s right for your business, start by evaluating your risk profile. If most of your sales – say 80% to 90% – are with financially stable domestic buyers, Trade Credit Insurance might be all you need. But if you’re exporting to countries with political or economic instability, adding Political Risk Insurance can provide extra peace of mind. Similarly, if a single customer accounts for more than 30% of your revenue, Accounts Receivable Insurance offers an essential safety net.

The insurance industry now safeguards over $3 trillion in annual sales and financings, covering more than 100 million businesses worldwide. Protecting your receivables isn’t just smart – it’s necessary. The challenge is finding the right mix of solutions for your unique risks. For personalized advice tailored to your business, check out CreditInsurance.com.

FAQs

What policy should I choose for tariffs disrupting buyer payments?

Trade disruption insurance or tariff-specific coverage can be a smart safety net for businesses dealing with trade-related losses caused by tariffs. These policies are designed to shield your business from financial setbacks, particularly those stemming from payment problems linked to tariff impacts. By offering this protection, they help maintain your company’s financial stability and reduce the risks associated with disrupted buyer payments.

What documents do I need to file a claim on a missed invoice?

To file a claim for a missed invoice, you’ll need to collect documents that confirm the invoice was issued and remains unpaid. Commonly required documents include:

- The original invoice: This serves as the primary proof of the amount owed.

- Proof of delivery or service completion: This could be a signed delivery receipt or a completion certificate to show the work or goods were provided.

- Communication records: Emails, letters, or messages discussing the unpaid invoice can help establish follow-up efforts and timelines.

- Relevant contractual agreements: Any contracts or terms that outline the payment agreement add further evidence.

It’s important to review your insurance policy or reach out to your provider for specific details on what documentation they require.

How do these policies affect my bank line of credit?

Using these policies as collateral can strengthen your bank line of credit by reducing the lender’s risk. This extra layer of security might allow you to negotiate improved financing terms and even qualify for higher credit limits.