Government-backed export credit programs help U.S. businesses manage the risks of international trade, like non-payment or political instability, and compete globally. These programs, offered by agencies like the Export-Import Bank of the United States (EXIM) and the Small Business Administration (SBA), provide tools such as:

- Export Credit Insurance: Covers up to 95% of sales invoices against risks like buyer insolvency or political disruptions.

- Loan Guarantees: Secures up to 90% of loans from private lenders for exporters.

- Direct Loans: Offers financing directly to foreign buyers or exporters when private funding isn’t available.

These programs are designed to fill gaps left by private lenders, enabling U.S. exporters to sell in high-risk or emerging markets. While offering strong risk protection and improved financing terms, they come with requirements like a minimum of 50% U.S. content in goods or services and exclusions for military-related sales.

Key Benefits:

- Protection against non-payment risks.

- Access to high-risk markets.

- Ability to offer competitive payment terms (e.g., up to 180 days).

- Boosted borrowing power using insured receivables as collateral.

Challenges:

- Documentation requirements.

- Limited coverage for certain high-risk countries.

- Exporters retain a small portion of the risk (typically 5–15%).

These programs are a practical solution for businesses aiming to expand globally while safeguarding their financial interests.

Export Credit Insurance

sbb-itb-b840488

What Are Government-Backed Export Credit Programs?

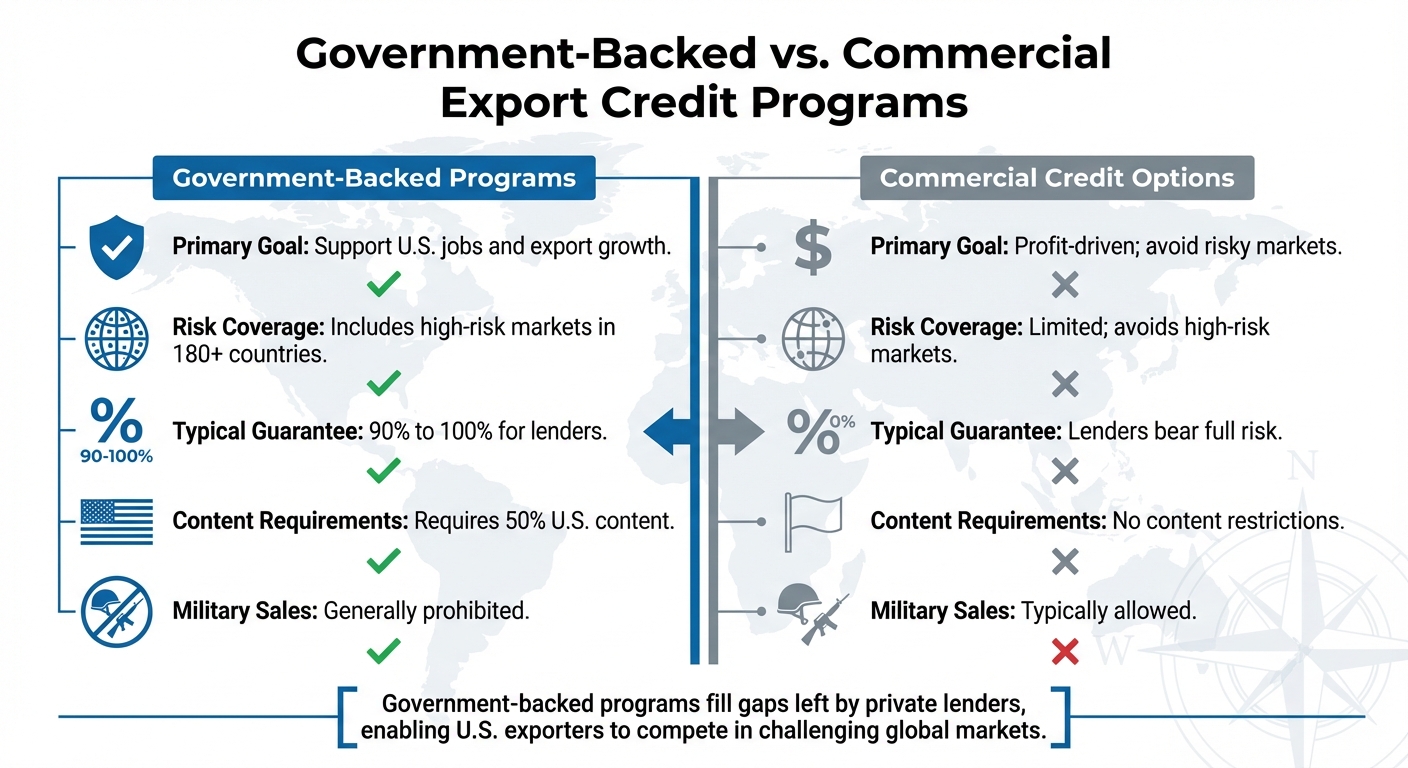

Government-Backed vs Commercial Export Credit Programs Comparison

Definition and Main Features

Government-backed export credit programs are financial tools provided by official Export Credit Agencies (ECAs) to assist U.S. companies in selling their goods and services internationally. These programs address credit and country risks – like buyer insolvency or political instability – that private banks often avoid.

These programs work through three main mechanisms:

- Export credit insurance: Protects exporters if foreign buyers fail to pay due to reasons like bankruptcy, war, or currency issues.

- Loan guarantees: Cover up to 90% of loans from private lenders, encouraging banks to finance export deals.

- Direct loans: Provide financing directly to foreign buyers or exporters when private funding isn’t available.

What sets these programs apart is the extent of protection they offer. For example, they can cover up to 98% of losses from commercial defaults and 100% for political risks. Additionally, for loans to businesses owned by minorities, women, or those in rural areas, the Export-Import Bank of the United States (EXIM) can extend its working capital guarantee to 100%. These protections are available in over 180 countries, offering U.S. exporters a safety net in markets where private insurers typically avoid operating.

How They Differ from Commercial Credit Options

The key distinction between government-backed programs and commercial credit lies in their purpose and risk tolerance. While commercial lenders prioritize profit and risk avoidance, government programs exist to support U.S. jobs and help American exporters compete with foreign companies backed by their governments. This allows these programs to finance deals in emerging or politically unstable markets that private banks might steer clear of.

There are also practical differences in their terms. Government-backed programs often offer more favorable conditions, such as advance rates of up to 75% on inventory and 90% on foreign receivables – terms that are generally more flexible than those offered by commercial lenders. However, these programs typically require at least 50% U.S. content in the goods or services financed and generally exclude military-related sales.

| Feature | Government-Backed Programs | Commercial Credit Options |

|---|---|---|

| Primary Goal | Support U.S. jobs and export growth | Profit-driven; avoid risky markets |

| Risk Coverage | Includes high-risk markets in 180+ countries | Limited; avoids high-risk markets |

| Typical Guarantee | 90% to 100% for lenders | Lenders bear full risk |

| Content Requirements | Requires 50% U.S. content | No content restrictions |

| Military Sales | Generally prohibited | Typically allowed |

These features make government-backed programs an essential resource for U.S. exporters looking to enter challenging markets where private lenders hesitate to operate.

The Role of Export Credit Agencies (ECAs) in Supporting Exporters

Reducing Financial and Political Risks

Export Credit Agencies (ECAs) serve as government-backed entities offering financial solutions that go beyond what private lenders typically provide. With around 115 official ECAs operating globally, they collectively support approximately $430 billion in international business activities each year.

ECAs play a critical role in protecting exporters from both commercial risks – like buyer insolvency, bankruptcy, or prolonged payment defaults – and political risks, such as war, expropriation, currency inconvertibility, or the revocation of import/export licenses.

For exporters dealing with custom-made goods, ECAs can offer pre-shipment guarantees that cover production costs if political disruptions prevent shipment. In cases where a crisis occurs during transit, ECAs can assist exporters in rerouting shipments to minimize financial losses.

This level of protection allows exporters to provide competitive open account terms – often up to 180 days – rather than demanding cash upfront. This flexibility makes U.S. exporters more appealing in global markets. By reducing risks, ECAs not only safeguard businesses but also help drive export growth.

Supporting Export Growth

Beyond mitigating risks, ECAs act as "lenders of last resort", stepping in to fill financing gaps when private lenders are hesitant to take on the risks associated with international trade. For example, in 2020, the Export-Import Bank of the United States (EXIM) authorized $5.4 billion in loan guarantees, insurance, and direct loans. This support facilitated an estimated $10.8 billion in U.S. export sales and helped sustain approximately 37,000 jobs.

Small businesses were a significant focus, accounting for nearly 89% of EXIM’s total transaction volume that year, with authorizations exceeding $2.0 billion.

This kind of financial support underscores how ECAs empower U.S. exporters to remain competitive, particularly in markets where private financing options are scarce. By bridging these gaps, ECAs open doors for businesses to thrive on an international scale.

Main U.S. Government Programs for Exporters

The U.S. government offers key programs to help exporters overcome financial barriers and compete in global markets.

Export-Import Bank of the United States (EXIM)

EXIM serves as the nation’s export credit agency, helping U.S. businesses secure opportunities abroad when private lenders are hesitant to take on risks tied to international transactions. It provides three core financing tools: export credit insurance, working capital guarantees, and guarantees for commercial loans to foreign buyers. These tools ensure that U.S. companies can confidently enter and thrive in global markets.

To participate, businesses must meet certain criteria: they need to have been operational for at least three years, employ at least one full-time worker, and maintain a positive net worth. Products must be made in the U.S., or services must be delivered by U.S. workers to meet EXIM’s content requirements.

Exporters also need to register on SAM.gov to obtain a Unique Entity Identifier (UEI) and a Dun & Bradstreet number. Additionally, EXIM charges exposure fees based on the transaction’s risk level and duration.

USDA GSM-102 Program

The USDA’s Export Credit Guarantee Program (GSM-102), managed by the Foreign Agricultural Service and the Commodity Credit Corporation (CCC), is focused on supporting U.S. agricultural exports. By offering credit guarantees, the program minimizes financial risks for lenders, facilitating up to $5.5 billion in agricultural exports annually.

The CCC guarantees cover 98% of the principal and part of the interest, with repayment terms capped at 18 months. In 2015, major markets for this program included South America, Mexico, and South Korea. The program supports a wide range of products, from wheat, soybeans, and feed grains to high-value items like meat, fruits, vegetables, wine, and frozen foods.

Here’s how it works: foreign financial institutions issue irrevocable, dollar-denominated letters of credit, which U.S. exporters typically assign to American banks. This setup ensures exporters receive payment upon shipment, while U.S. banks extend credit to the foreign institutions.

Both U.S. exporters and financial institutions must be pre-approved by the CCC to participate. Exporters pay a guarantee fee tied to the dollar amount guaranteed, with rates determined by factors such as country risk, the foreign bank’s risk level, and repayment terms. The program is designed to cover its own costs over time through these fees.

How to Access and Use These Programs

Application Process

To get started, you’ll need to register on SAM.gov to obtain both a Unique Entity Identifier (UEI) and a Dun & Bradstreet number.

If you’re applying for EXIM programs, you must meet a few basic requirements: at least three years of operation (or one year for working capital guarantees), a positive net worth, at least one full-time employee, and products with at least 50% U.S.-made content. For help, you can reach out to an EXIM field office or use their Insurance Broker Locator.

For the USDA GSM-102 program, the process differs slightly. Start by submitting an Exporter Qualification Application to the Foreign Agricultural Service and setting up a USDA eAuthentication account. Each user will need their own eAuthentication ID to access the GSM Online System. Once qualified, negotiate your sales contract and ensure the foreign importer opens a Letter of Credit at a USDA-approved foreign bank in your favor. Afterward, apply for the CCC guarantee online and pay the required fee before shipping your goods.

Once approved, you can incorporate these credit coverage options into your regular business operations.

Using Credit Coverage in Your Business

After securing credit coverage, you can use these tools to strengthen your financial position and improve cash flow. Export credit insurance allows you to offer competitive "open account" terms to international buyers – typically up to 180 days for consumer goods – instead of requiring upfront payments or letters of credit. This flexibility can often make the difference in securing international deals.

Your insured foreign accounts receivable can also serve as collateral. Use these receivables to boost your borrowing base, improve cash flow, and access additional working capital.

"EXIM doesn’t replace your private bank; it simply backs their loan and increases your borrowing power".

If you’re using an EXIM working capital guarantee, you may even qualify for a 25% discount on premiums for multi-buyer insurance policies.

To keep your EXIM coverage active, report each shipment on time and pay the necessary premiums. For USDA GSM-102 participants, make sure to apply for the payment guarantee before the export date and retain transaction documents for five years in case of audits. The guarantee fee is typically included in your selling price during contract negotiations.

Benefits and Limitations of Government-Backed Export Credit Programs

Benefits for Exporters

Government-backed export credit programs are a game-changer for businesses looking to expand globally. They offer a safety net against non-payment risks, covering both commercial risks (like buyer insolvency) and political risks (such as war, currency issues, or expropriation). For medium-term transactions, these programs typically insure about 85% of the net contract value.

Another major perk is improved financing terms. With insured foreign receivables backed by the U.S. government, businesses can increase their borrowing power and improve cash flow. This means exporters can offer competitive open account terms – up to 180 days – rather than demanding upfront payments. Plus, the cost is relatively low, with most multi-buyer policies priced at less than 1% of insured sales.

These programs also open doors to emerging markets where private insurers often hesitate to operate. Small businesses, in particular, benefit from additional incentives, like a 25% premium discount on multi-buyer insurance policies when using an EXIM working capital guarantee.

Despite these advantages, there are some hurdles exporters need to navigate.

Limitations and Challenges

While these programs offer substantial benefits, they come with certain restrictions. For starters, products must contain at least 50% U.S. content to qualify, meaning they need to be largely American-made. Additionally, the Country Limitation Schedule can restrict or block support in high-risk regions. Military-related products and sales to foreign military entities are usually excluded as well.

Exporters also need to shoulder some of the risks themselves, as coverage typically only accounts for 85% to 95% of losses. Claims can be denied if policy conditions aren’t met, and coverage doesn’t include physical damage to goods – separate insurance, like marine or casualty coverage, is required for that. On top of that, the process can be time-consuming due to the extensive documentation and underwriting requirements.

| Aspect | Benefits | Limitations |

|---|---|---|

| Financial Protection | Covers 90–95% of invoice value against non-payment | Exporters retain 5–15% of the risk |

| Market Access | Supports entry into high-risk emerging markets | Limited by the Country Limitation Schedule |

| Competitiveness | Enables offering open account terms (up to 180 days) | Requires at least 50% U.S. content; excludes military sales |

| Capital & Liquidity | Boosts borrowing capacity with insured receivables | Involves premium costs and requires extensive documentation |

Conclusion

Government-backed export credit programs play a crucial role in helping U.S. exporters compete on the global stage while managing the risks of international trade. Programs like EXIM offer comprehensive risk protection, allowing businesses to explore opportunities in over 180 countries, including markets where private insurers may not operate.

These programs also enable exporters to offer open account terms – up to 180 days – without requiring upfront payment. Additionally, insured receivables can be used as collateral to secure improved financing terms, giving businesses more flexibility.

That said, there are limitations to consider. For example, exporters must meet a minimum 50% U.S. content requirement, and coverage may exclude certain high-risk countries or military-related products.

Whether you’re just starting out or have years of exporting experience, understanding these programs is essential. Resources like CreditInsurance.com can guide you through the complexities of export credit insurance, helping you evaluate your coverage options and make informed decisions to safeguard your foreign receivables while pursuing growth.

Taking advantage of these programs early – before payment issues arise – can protect your business and enhance your global competitiveness. Working with specialists who understand your unique export needs ensures you get tailored solutions that align with your goals.

FAQs

Do I qualify for EXIM or SBA export support?

When it comes to securing export support, whether through EXIM or SBA, it all hinges on your business’s specific needs and situation. EXIM Bank offers tools like export credit insurance and financing options aimed at U.S. exporters. To qualify, businesses generally need to demonstrate creditworthiness and active involvement in exporting.

On the other hand, the Small Business Administration (SBA) provides export loans, which come with a guaranty of up to 90%. These loans are tailored for small businesses that have solid export plans in place.

To figure out if you qualify, it’s a good idea to connect with your local SBA office or reach out to an export lender for guidance.

How much U.S. content do my products need?

The amount of U.S. content needed varies depending on the program’s specific requirements. For export credit insurance policies, there are usually set thresholds for U.S. content that products must meet to qualify for coverage or financing support. Be sure to review the program’s guidelines carefully to confirm your products meet these standards.

What happens if my foreign buyer doesn’t pay?

Export credit insurance can be a lifesaver if your foreign buyer fails to pay due to commercial or political risks. This type of insurance covers nonpayment, giving you the ability to file a claim and recover your losses. Most claims are processed within 60 days, providing not only financial security but also a sense of reassurance.