When deciding on an insurance provider, understanding financial stability is key. Credit ratings from agencies like AM Best and Demotech help determine an insurer’s ability to meet financial obligations. Here’s the difference:

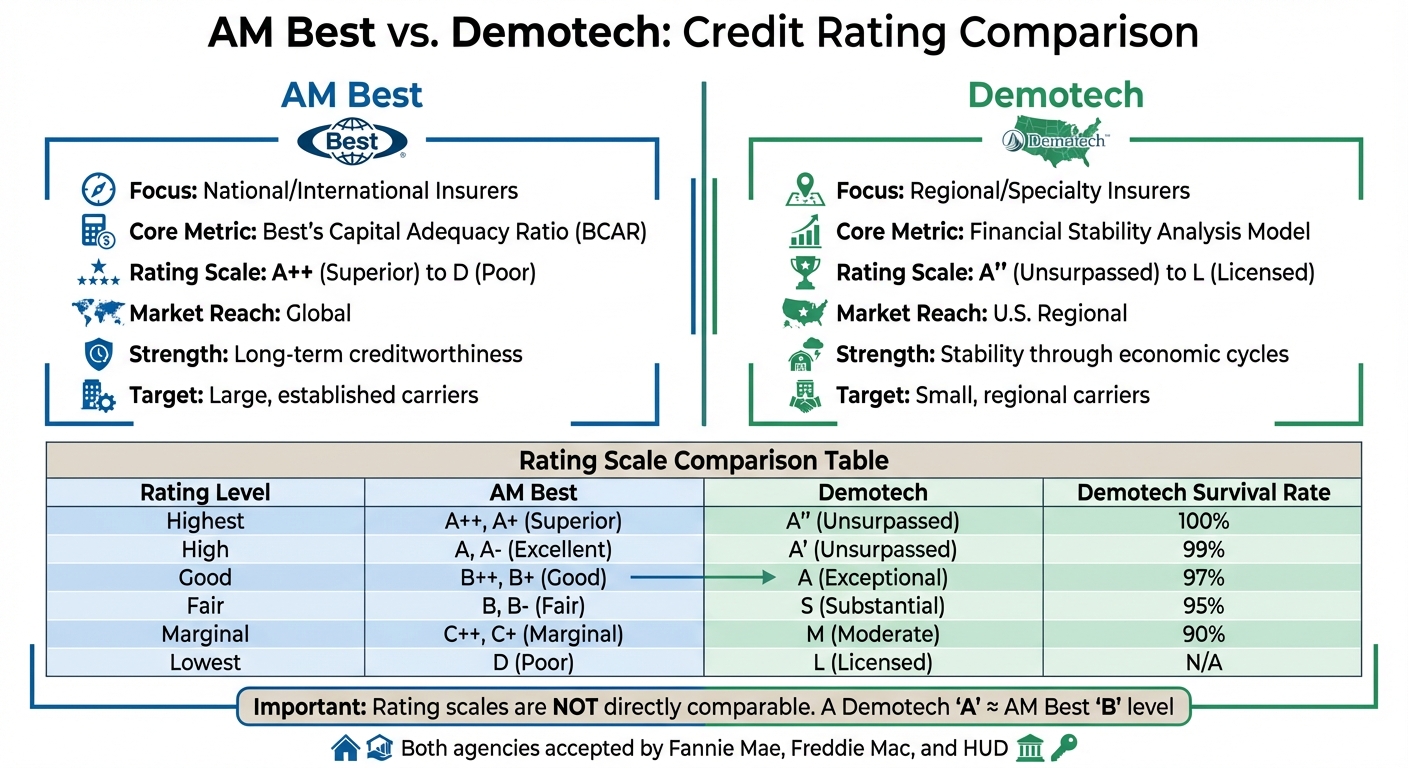

- AM Best: Focuses on large, national, and international insurers. Uses a strict evaluation process including metrics like Balance Sheet Strength, Operating Performance, and Enterprise Risk Management (ERM). Known for its global reach and detailed ratings.

- Demotech: Specializes in regional and niche insurers in the U.S. Emphasizes financial stability over size, providing ratings for smaller insurers often overlooked by AM Best. Its Financial Stability Ratings (FSRs) are widely accepted in the U.S. mortgage market.

Quick Comparison

| Feature | AM Best | Demotech |

|---|---|---|

| Focus | National/International Insurers | Regional/Specialty Insurers |

| Core Metric | Best’s Capital Adequacy Ratio (BCAR) | Financial Stability Analysis Model |

| Rating Scale | A++ (Superior) to D (Poor) | A” (Unsurpassed) to L (Licensed) |

| Market Reach | Global | U.S. Regional |

| Strength | Long-term creditworthiness | Stability through economic cycles |

Both agencies play critical roles but cater to different segments of the market. Choose AM Best for larger carriers and Demotech for regional insurers. Always review the rating scale carefully, as their evaluations differ significantly.

AM Best vs Demotech Insurance Rating Agencies Comparison Chart

Rating Agencies: AM Best, S&P, Moody’s, and Fitch – Explained!

sbb-itb-b840488

How AM Best Rates Insurance Companies

AM Best takes a tailored approach to rating insurance companies, using a "building block" methodology that blends both quantitative data and qualitative insights. Unlike generic corporate rating models, this system is specifically designed for the unique dynamics of the insurance industry. The evaluation focuses on five key areas: Balance Sheet Strength, Best’s Capital Adequacy Ratio (BCAR), Operating Performance, Business Profile, and Enterprise Risk Management (ERM).

Balance Sheet Strength evaluates whether an insurer has the capital, liquidity, and flexibility needed to pay claims and remain financially stable. Operating Performance looks at consistent earnings over time, which are crucial for building and maintaining capital. Business Profile examines market share, product offerings, distribution strategies, and geographic footprint – factors that reveal an insurer’s competitive position. Enterprise Risk Management (ERM) assesses how well a company identifies and manages risks across its operations.

Meanwhile, BCAR, a quantitative tool, measures how well an insurer’s capital is positioned to handle underwriting and investment risks, ensuring resilience under stress. AM Best’s ratings are supported by a committee-based review process and regular updates, ensuring they reflect current financial conditions accurately and without bias.

What AM Best Evaluates

Each of the five pillars is broken down into specific factors:

- Balance Sheet Strength: Focuses on capitalization, asset quality, reinsurance programs, and liquidity.

- Best’s Capital Adequacy Ratio (BCAR): Evaluates risk-adjusted capital in relation to underwriting and investment risks.

- Operating Performance: Analyzes underwriting results, investment income, and overall earnings stability, emphasizing the importance of consistent profitability.

- Business Profile: Considers market share, product diversity, distribution channels, and geographic reach.

- Enterprise Risk Management (ERM): Looks at the company’s risk culture and the effectiveness of its strategies for identifying and mitigating risks.

AM Best’s Market Coverage

AM Best applies its thorough evaluation process across global markets, focusing on property and casualty insurers, life and health providers, and large multinational insurance companies. Its ratings often target major, established insurers with international operations and a strong market presence. By using its standardized Best’s Credit Rating Methodology (BCRM), AM Best ensures consistency in its assessments across different regions and sectors.

This global perspective makes AM Best a trusted authority in evaluating complex, multi-line insurance organizations. Its ratings not only guide insurers in maintaining financial health but also help businesses and consumers make informed decisions when choosing insurance partners. This specialized, worldwide focus sets AM Best apart from other rating agencies.

How Demotech Rates Insurance Companies

Demotech has developed a unique approach to rating insurance companies. Since 1989, the firm has concentrated on independent, regional, and specialty insurers, particularly those operating in niche markets. The foundation of its methodology lies in the Financial Stability Analysis Model, which was introduced in 1988.

The company operates on a core belief: financial stability is not determined by size. As Demotech explains:

Small, well-managed Property & Casualty insurers are more financially stable than larger, highly leveraged insurers.

This principle allows regional carriers to earn high ratings based on their inherent financial strength, rather than being judged by their market share or geographic presence. This perspective sets Demotech apart from traditional rating agencies and highlights its distinctive evaluation process.

Demotech’s Financial Stability Ratings (FSRs) serve as early indicators of an insurer’s ability to navigate economic challenges. The firm places a strong emphasis on balance sheet integrity over short-term gains, prioritizing solid capitalization and high-quality reinsurance as the foundation of long-term stability. For instance, on March 19, 2026, Demotech downgraded Wilmington Insurance Company and Freedom Advantage Insurance Company, and on February 27, 2026, it assigned a new rating to Olympus Insurance Company.

What Demotech Evaluates

Demotech employs a mix of quantitative metrics and qualitative insights to evaluate insurers, whether they are established companies or start-ups. For insurers with an operational history, the firm examines statutory financials along with qualitative factors like management performance and reinsurance arrangements. A critical focus is placed on reserve adequacy, which refers to the adequacy of loss reserves and loss adjustment expenses.

For newer insurers or those with less than five years of history, Demotech adapts its approach. It evaluates pro forma financial statements, business plans, management bios, underwriting guidelines, catastrophe modeling reports, and investment strategies. This tailored method allows start-ups to obtain ratings even with limited operational history.

Key metrics include admitted assets – assets recognized by state law that are easily convertible to meet obligations – and policyholders’ surplus, which is calculated as admitted assets minus liabilities. These indicators are central to determining an insurer’s ability to meet its commitments to policyholders. Together, these factors reflect Demotech’s focus on assessing financial resilience.

Demotech’s Market Coverage

While AM Best operates globally, Demotech focuses almost exclusively on U.S.-based regional and specialty insurers, including risk retention groups (RRGs) and carriers serving high-risk markets. Its FSRs are widely accepted by the secondary mortgage market, including entities like Fannie Mae and Freddie Mac, as well as HUD programs and most mortgage lenders. This recognition is vital for regional insurers, as credible ratings are often a prerequisite for participating in these markets. Demotech’s specialized approach highlights its commitment to evaluating financial stability without relying on insurer size, setting the stage for a comparison with AM Best’s broader global framework in the next sections.

What AM Best and Demotech Have in Common

While AM Best and Demotech focus on different segments of the insurance market, they share some fundamental principles in their evaluation processes. Both agencies rely heavily on statutory filings, such as annual and quarterly statements submitted to state Departments of Insurance. As Joseph Petrelli, President and Founder of Demotech Inc., explains:

"The methodology utilized by Demotech relies on the underlying records and/or summaries prepared by responsible officers or employees of the P&C insurer and/or its parent company. We rely on the truth and accuracy of information contained in the annual statements filed with the state Departments of Insurance."

This reliance ensures that both agencies base their evaluations on verified, reliable data. They use Generally Accepted Accounting Principles (GAAP) or statutory statements as the foundation for calculating financial ratios. By adhering to these shared standards, we can better understand how their methodologies diverge later in their analytical processes.

Common Evaluation Areas

Both AM Best and Demotech evaluate similar financial metrics to determine an insurer’s ability to withstand economic challenges. Key areas of focus include:

- Policyholders’ surplus: A measure of financial stability.

- Working capital and liquidity: Indicators of short-term financial health.

- Operational performance: Metrics like net income, total revenues, and administrative expenses are analyzed to assess overall efficiency and profitability.

Additionally, both agencies scrutinize reinsurance programs and use predictive modeling to identify potential financial risks. These evaluations aim to provide a comprehensive picture of an insurer’s financial resilience.

Use of Regulatory Standards

Both agencies integrate National Association of Insurance Commissioners (NAIC) standards and state licensing requirements into their evaluations. To support their assessments, they require extensive documentation, including:

- Five years of annual statements

- The latest independent audit

- Actuarial opinions

- Management’s discussion and analysis (MD&A)

Their ratings play a critical role in regulatory compliance and market participation. For example, both AM Best and Demotech are formally recognized by Fannie Mae, Freddie Mac, and the Department of Housing and Urban Development (HUD) for property insurance ratings. This recognition allows insurers rated by these agencies to participate in the secondary mortgage market. Notably, Demotech was the first agency to have its methodology reviewed and accepted by these government-sponsored enterprises, enabling smaller, regional insurers – previously unrated – to gain access to these markets.

These shared practices highlight the foundational similarities between AM Best and Demotech, setting the stage for exploring their distinct approaches.

How AM Best and Demotech Differ

While both AM Best and Demotech base their ratings on regulatory filings and financial analysis, their methods and focus areas are quite different. Understanding these distinctions can help you make better decisions when evaluating insurer ratings for your credit insurance needs.

Geographic Reach and Target Markets

AM Best primarily evaluates large national and international insurance carriers. On the other hand, Demotech focuses on U.S.-based regional and specialty insurers [1,4].

Demotech was specifically created to cater to smaller, regional insurers that global agencies often overlook. This focus addresses a key market need. For example, as of 2014, Demotech was reviewing insurers responsible for about 60% of property and casualty policies in Florida. Today, it rates over 400 insurance companies across the U.S., with a strong presence in states like Florida and Louisiana.

Joseph Petrelli, President and Founder of Demotech Inc., explains this philosophy:

Financial stability is, in our opinion, independent of size. This implies that small, well-managed P&C insurers can have better financial stability than larger, highly leveraged P&C insurers.

This approach allows Demotech to rate newly established insurers based on business plans and pro forma statements – something AM Best is less likely to do without significant historical financial data. These differences in focus naturally lead to variations in the tools and methods each agency uses.

Different Analysis Tools

AM Best and Demotech rely on distinct tools to measure financial strength. AM Best uses its proprietary Best’s Capital Adequacy Ratio (BCAR), a complex risk modeling system that evaluates capital adequacy across various risk categories. Demotech, on the other hand, employs its Financial Stability Analysis Model®, which uses regression and multivariate analysis to identify potential insolvencies. According to Petrelli:

Our Financial Stability Analysis Model® would have flagged P&C insurers as insolvent a year before regulatory action.

Demotech’s model analyzes hundreds of financial statement indicators, such as changes in working capital and restricted cash. Unlike AM Best, which develops proprietary metrics, Demotech relies on statutory financial ratios derived directly from state Department of Insurance filings. Beyond these quantitative tools, their qualitative approaches also differ significantly.

Different Qualitative Factors

AM Best emphasizes enterprise risk management (ERM) and innovation, assessing how insurers manage emerging risks through advanced governance systems. In contrast, Demotech adopts a more hands-on "tactile review" process. This involves detailed evaluations of management discussion and analysis (MD&A), actuarial opinions, and audit reports. Demotech focuses on operational discipline, which is often more relevant for smaller insurers than the elaborate risk management frameworks favored by AM Best.

| Feature | AM Best | Demotech |

|---|---|---|

| Primary Focus | National/International Insurers | Regional/Specialty Insurers |

| Core Tool | BCAR (Best’s Capital Adequacy Ratio) | Financial Stability Analysis Model® |

| Key Qualitative Factor | ERM and Innovation | Audit & Actuarial Reviews |

| Data Source | Global Financial Data | State Department of Insurance Filings |

Source:

These methodological differences often result in varying ratings for the same insurer, reflecting the unique priorities of each agency. This distinction is worth considering when making credit insurance decisions.

Understanding the Rating Scales

After explaining how AM Best and Demotech assess insurers, it’s important to break down what their ratings actually signify.

How Each Scale Works

AM Best’s Financial Strength Rating (FSR) ranges from A++ (Superior) to D (Poor). This scale evaluates an insurer’s ability to meet its financial obligations, with multiple levels to provide more detailed insights.

Demotech’s Financial Stability Rating® (FSR), on the other hand, uses a different framework. Its ratings include A” (Unsurpassed), A’ (Unsurpassed), A (Exceptional), S (Substantial), M (Moderate), and L (Licensed). Unlike AM Best, Demotech places a stronger emphasis on an insurer’s likelihood of surviving during tough economic periods.

It’s worth noting that these scales aren’t directly comparable. For instance, a Demotech A rating doesn’t equate to an AM Best A rating.

| Rating Level | AM Best Category | Demotech Category | Demotech Survival Prediction |

|---|---|---|---|

| Highest | A++, A+ (Superior) | A” (Unsurpassed) | 100% |

| High | A, A- (Excellent) | A’ (Unsurpassed) | 99% |

| Good/Exceptional | B++, B+ (Good) | A (Exceptional) | 97% |

| Fair/Substantial | B, B- (Fair) | S (Substantial) | 95% |

| Marginal/Moderate | C++, C+ (Marginal) | M (Moderate) | 90% |

| Lowest | D (Poor) | L (Licensed) | N/A |

Understanding these scales is essential because they directly reflect an insurer’s financial reliability.

What Ratings Mean for Insurers

The ratings provided by AM Best and Demotech offer a snapshot of an insurer’s financial strength and risk levels. Higher ratings from either agency suggest stronger financial health and inspire greater confidence among clients. For example, an AM Best rating of A++ or A+ signifies a superior ability to meet financial obligations. Similarly, Demotech’s A” rating indicates unparalleled stability, even in the face of severe economic challenges.

On the other hand, lower ratings highlight increased financial risk. An AM Best D (Poor) rating signals a very weak capacity to meet obligations. Meanwhile, Demotech’s L (Licensed) rating shows that the insurer is state-licensed but has limited ability to endure economic stress.

Interestingly, Demotech has historically assigned an A or higher rating to 98% of the insurers it evaluates as of 2025. This contrasts with AM Best’s stricter approach. Between 2021 and 2023, 14 out of 15 property and casualty insurers in Florida and Louisiana that became insolvent had been rated A by Demotech within a year of their collapse.

These ratings and survival predictions are invaluable tools for businesses when selecting credit insurance providers. By understanding the differences in these rating systems, you can better evaluate the true financial strength and reliability behind each letter grade.

Why These Ratings Matter for Credit Insurance

Once you understand how each rating agency operates, the next step is recognizing how their ratings influence your credit insurance decisions. Ratings from agencies like AM Best and Demotech provide a clear picture of an insurer’s ability to fulfill claims if a customer defaults. These evaluations focus on an insurance company’s financial strength and its ability to meet obligations, making them a critical factor for businesses relying on credit insurance to safeguard against non-payment. Choosing a financially stable insurer is not just smart – it’s essential for protecting your business.

Which Rating Agency to Use

The right rating agency depends on the type of insurer you’re evaluating. For larger, national, or international carriers, AM Best is the go-to standard. Its ratings are widely trusted for assessing long-term financial stability and strength. Typically, an AM Best rating of A- or higher signals that the insurer is financially sound and reliable.

On the other hand, Demotech is particularly useful for evaluating smaller, regional, or specialty insurers that may not be rated by AM Best. Demotech’s ratings are designed to highlight financial stability regardless of the company’s size. This approach ensures that even well-managed smaller insurers can demonstrate their financial health. Major organizations like Fannie Mae and Freddie Mac recognize Demotech ratings, adding to their credibility.

Since the rating scales vary between agencies, it’s important to refer to the specific scales discussed earlier. Additionally, if you’re considering a smaller insurer, check whether their reinsurers hold strong AM Best ratings (A- or better). This extra layer of assurance can provide additional peace of mind.

How Ratings Affect Your Insurance Choices

High ratings are a safeguard, especially during economic downturns. They indicate that an insurer has the financial resources to pay claims even in challenging times. If an insurer fails, your business could lose critical protection against non-payment when it’s needed the most.

Understanding the difference between AM Best’s focus on creditworthiness and default risk and Demotech’s emphasis on stability through underwriting cycles can help you make a more informed decision. For businesses exploring credit insurance options, platforms like CreditInsurance.com can guide you in selecting the right policies and using insured receivables to improve financing opportunities.

Conclusion

Choosing between AM Best and Demotech requires understanding their different focuses. AM Best emphasizes long-term creditworthiness with stricter evaluation criteria, making it a go-to for assessing large national and international insurers. On the other hand, Demotech specializes in evaluating regional and specialty carriers, focusing on their resilience to economic changes and underwriting cycles.

It’s crucial to recognize that rating scales between the two agencies don’t align directly. For example, Demotech’s "A" (Exceptional) rating corresponds roughly to AM Best’s "B" or "C++". As Insurance Journal explains:

DemoTech’s ‘A’ financial stability ratings have long been considered to be roughly equivalent to AM Best’s ‘B’-level ratings.

This difference underscores the importance of confirming which agency issued the rating before making any decisions.

For global carriers, AM Best’s higher ratings, such as A- or above, provide greater confidence in financial strength. Meanwhile, for smaller, regional insurers, Demotech offers unique insights into their financial stability. Understanding these distinctions is key to making informed insurance decisions.

FAQs

Can I compare an AM Best rating to a Demotech rating?

When comparing ratings from Demotech and AM Best, it’s important to recognize key distinctions. For instance, Demotech’s ‘A’ (Exceptional) rating is often equated to an AM Best ‘B’ or ‘C++’ rating, indicating varying levels of financial strength. AM Best specializes in insurance credit ratings and applies a more detailed and rigorous methodology. In contrast, Demotech assesses financial stability but uses less stringent criteria. Knowing the standards each agency employs is essential for making accurate comparisons.

Which rating matters more for a regional U.S. insurer?

For regional insurers in the U.S., the importance of a rating often depends on the situation. Demotech’s Financial Stability Ratings® are well-regarded in the U.S. property and casualty insurance market, especially for smaller and regional insurers. These ratings are tailored to address the unique risks faced by these companies. On the other hand, AM Best’s ratings tend to carry more weight in global or broader contexts. For local market and regulatory purposes, regional insurers often lean on Demotech’s ratings as their primary benchmark.

What should I check if my insurer is only rated by Demotech?

If your insurer is rated exclusively by Demotech, take the time to review their Financial Stability Rating (FSR) to gain insight into the company’s financial health. Look into Demotech’s rating methodology to ensure it meets accepted industry practices. Since Demotech ratings can vary from those provided by AM Best, it’s wise to go a step further – examine the insurer’s financial statements and overall reputation to get a clearer picture of their stability and trustworthiness.