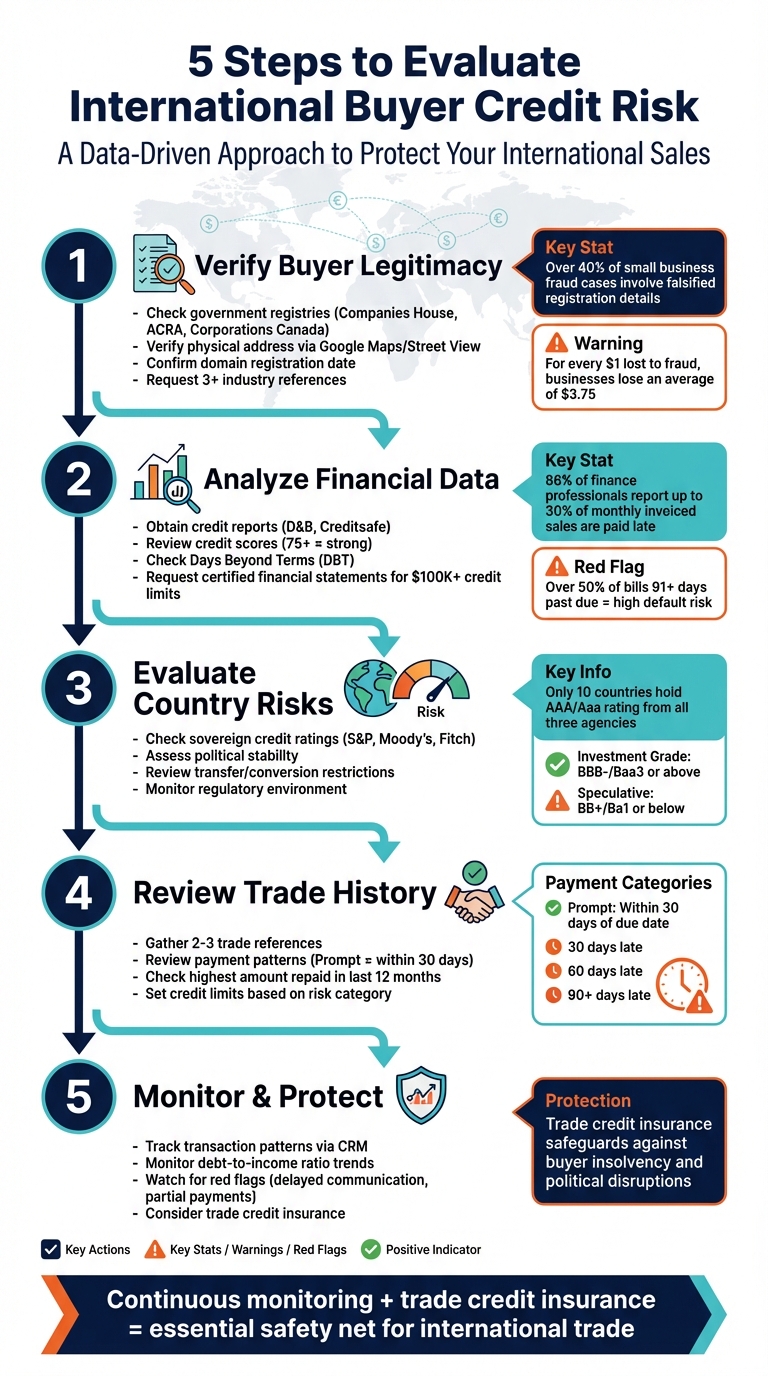

Selling to international buyers can boost your revenue, but it comes with risks, especially when offering open credit terms. Here’s a quick guide to help you evaluate buyer credit risk effectively:

- Verify Buyer Legitimacy: Confirm the buyer’s registration, address, and online presence to avoid fraud.

- Analyze Financial Data: Use credit reports and financial statements to assess payment behavior and stability.

- Evaluate Country Risks: Check political, economic, and currency risks in the buyer’s country.

- Review Trade History: Look at the buyer’s payment patterns with other suppliers and set appropriate credit limits.

- Monitor Activity: Continuously track buyer behavior and safeguard receivables with trade credit insurance.

5-Step International Buyer Credit Risk Evaluation Process

The 3 kinds of risks in international trade finance. – FITTskills online.

sbb-itb-b840488

Step 1: Verify Buyer Legitimacy and Background

Before diving into financial analysis, it’s critical to confirm that your potential buyer is a legitimate, operating business. Fraud is a major concern – over 40% of small business fraud cases involve falsified registration details. Even worse, for every $1 lost to fraud, U.S. businesses lose an average of $3.75, making upfront verification a must.

Confirm Company Registration and Business Details

Start by checking official government registries like the UK’s Companies House, Singapore’s ACRA, or Corporations Canada. These platforms can help you confirm essential details such as legal status, company name, registration number, and director information. For a more global approach, tools like OpenCorporates compile public records from over 130 jurisdictions, while credit reporting agencies like Creditsafe and Dun & Bradstreet provide instant access to reports on more than 430 million businesses across 200 countries. If you need deeper insights, the U.S. Commercial Service offers International Company Profiles (ICPs) prepared by in-country specialists.

To ensure physical legitimacy, verify the company’s address using Google Maps or Street View. Call their listed phone number to confirm it’s active, and use WHOIS to check the domain registration date of their website. For instance, a company claiming decades of experience but with a domain registered only weeks ago is a major warning sign.

Once you’ve confirmed the basics, shift your attention to uncovering any red flags in their online presence.

Identify Warning Signs

Be on the lookout for inconsistencies in their digital footprint. Poor grammar, mismatched language styles, low-resolution images, and missing job listings are all potential indicators of a fraudulent or "shell" website. A cautionary tale: in early 2024, a U.S. importer lost $2.3 million to a fake entity posing as an Asian supplier. The fraudulent website and invoices were nearly identical to the real vendor’s, but the domain had only been registered three weeks earlier.

"In an era where fraud is on the rise, it’s much better to be forewarned than to be caught by surprise."

– Steve Carpenter, Country Director, North America, Creditsafe

Ask for at least three industry references, including contact names and emails, to verify credibility. Be wary of buyers who request shipments to addresses different from their registered location or who place small, prepaid orders initially to gain trust before requesting larger orders on credit and disappearing. Cross-check the executive team listed on their website’s "About" page with LinkedIn profiles to confirm identities, and ensure their site includes clear Terms & Conditions and Privacy Policies, especially if they operate in regions with strict regulations like GDPR.

Step 2: Analyze Credit Reports and Financial Data

Once you’ve confirmed the buyer’s legitimacy, it’s time to evaluate their financial trustworthiness. Credit reports and financial statements provide a clear picture of whether the buyer has the resources and discipline to meet their payment commitments. This step is essential – 86% of finance professionals report that up to 30% of their monthly invoiced sales are paid late.

Review Credit Reports and Payment History

Start by obtaining a credit report from sources like Dun & Bradstreet or Creditsafe. These reports often include a numerical credit score (typically 1–100, with scores above 75 considered strong) or a letter grade (A–E), which predicts how likely a buyer is to pay on time. Pay close attention to metrics like Days Beyond Terms (DBT), which measures how many days past the due date a buyer typically pays. A steady DBT is a good sign, but irregular spikes and drops could indicate financial trouble.

Analyzing payment trends is equally important. Compare current payment speeds to the same period last year. A sharp increase in delays over 12 months may point to financial instability. Additionally, review the aging of accounts – if more than 50% of outstanding invoices are over 91 days past due, the risk of default is high. Cross-check this data with trade references from other suppliers (aim for 2–3 references). In global trade, "prompt" payment usually means settling invoices within 30 days of the due date. Also, look for tax liens, legal judgments, collections, or bankruptcy filings in public records.

"The quality of a credit report you should expect for a hotdog vendor in New York City is going to be very different to a large corporation anywhere in the world. Filing laws vary drastically by country."

– Leighton Weston, Product Expert and Global Account Director, Creditsafe

To ensure fairness across markets, use standardized international scoring models and group customers by size and region rather than applying a uniform policy. In regions where private credit data is limited, the U.S. Commercial Service offers International Company Profiles (ICPs), which include management details, financial data, and an expert opinion on the company’s viability.

Next, dive into the buyer’s financial statements to deepen your assessment.

Examine Financial Statements

For credit limits exceeding $100,000, always request certified financial statements, including the most recent year-end balance sheet and profit/loss (income) statement. While the balance sheet shows the company’s assets and liabilities, the cash flow statement is critical for understanding whether they have the liquid capital to cover invoices while waiting for payments from their own customers. A company might appear stable on paper but still struggle to meet short-term obligations if too much cash is tied up in inventory or receivables.

Look for consistent profitability in the income statement as an indicator of long-term stability. Cross-check these financial documents with credit reports to identify any outstanding debts, lawsuits, or liens that could affect their ability to pay. With the buyer’s permission, you can also contact their bank to verify their average daily balance and check for a history of overdrafts, which may signal cash flow problems. If a buyer refuses to share financial documents or bank references, treat this as a warning sign.

| Indicator | Positive Sign | Red Flag |

|---|---|---|

| Payment Consistency | Pays within 5–10 days of agreed terms | Erratic spikes in Days Beyond Terms (DBT) |

| Outstanding Debt | Majority of bills are current | Over 50% of bills are 91+ days past due |

| Cash Flow | Sufficient to float own receivables | Heavily reliant on bank lines for daily operations |

| Currency Preference | Willing to pay in USD or stable reserve currency | Insists on volatile local currency to shift FX risk |

These indicators can help you decide whether further investigation is necessary. For example, if a buyer insists on paying in their local currency instead of USD, it’s worth questioning their motives. As Leighton Weston of Creditsafe explains:

"If you ask to be paid in USD and they insist on using their local currency, that’s worth questioning. Why don’t they want to deal in the world’s reserve currency?"

This is especially relevant in markets like Argentina or Turkey, where currencies can fluctuate by 2% to 10% in just a few days, potentially undermining the buyer’s ability to meet USD obligations.

Step 3: Evaluate Country and Economic Risks

Once you’ve analyzed financial risks, it’s time to consider how the buyer’s country conditions might impact payment. For instance, governments may impose capital controls that block currency conversion or take drastic measures during economic crises, creating transfer and conversion challenges. A prime example occurred in 2019 when Argentina introduced strict policies aimed at curbing foreign exchange outflows, which complicated international transactions. Similarly, in 2017, protests in Ethiopia targeted specific companies perceived as politically aligned, leading to significant cash flow disruptions and payment defaults. Incorporating country risk data into credit scoring models can refine evaluations of buyer reliability. After addressing buyer-specific risks, the focus shifts to external factors that could influence payment outcomes.

Review Country Credit Ratings and Political Conditions

Start by checking sovereign credit ratings from agencies like S&P, Moody’s, and Fitch. These ratings reflect a government’s ability and willingness to meet its debt obligations. For S&P and Fitch, a rating of BBB‑ or above is considered "investment grade", while BB+ or lower is classified as "speculative" or "junk". Moody’s uses slightly different terms, with Baa3 or higher labeled as investment grade, and Ba1 or below as speculative. Globally, only 10 countries – including Australia, Canada, Germany, and Singapore – hold the highest AAA/Aaa rating from all three agencies. However, in August 2023, Fitch downgraded the United States from AAA to AA+, citing concerns over governance standards.

When reviewing sovereign ratings, pay close attention to risks like government-imposed transfer restrictions or non-payment issues, especially with state-owned or heavily regulated entities. Also, consider a country’s import cover and sovereign non-payment risk. For instance, Export Development Canada reported in 2019 that Nigeria’s sovereign rating was downgraded due to rising external debt, slow structural reforms, and growing security challenges.

"A country risk rating measures the risk of non‑payment by companies in a given country. This risk is due to conditions or events outside any company’s control."

– Allianz Trade

Political instability is just as critical as economic factors. For example, in October 2019, protests in Ecuador escalated to attacks on government offices over the removal of fuel subsidies, showing how political unrest can lead to sudden policy changes and disrupt business operations. Assess the likelihood of political violence, such as demonstrations or conflicts that could result in government overthrows or abrupt economic policy shifts. Also, consider the risk of government interference, including cancellations of permits, regulatory changes, or even asset expropriation. Evaluating these external risks strengthens the credit scoring process for international buyers.

From here, move on to analyzing how regulatory and market conditions influence a buyer’s ability to meet their obligations.

Assess Regulatory and Market Factors

Take a closer look at the regulatory environment and market conditions that may impact buyer payments. Tools like Allianz Trade’s SBE rating provide insights into a country’s legal system, corruption levels, and ease of doing business. Credendo rates currency inconvertibility and transfer restriction risks on a scale of 1 to 7, offering a clear view of whether a buyer can access the foreign currency needed for payment. Coface also evaluates over 160 countries and 13 sectors, combining macroeconomic, financial, and political data to estimate the average credit risk for businesses in a particular country.

Short-term risk indicators are equally important. Allianz Trade’s Financial Flows Indicator (FFI) helps identify immediate threats to trade receivables and financing risks over the next 6–12 months. Their short-term risk scale ranges from 1 (lowest) to 4 (highest). Additionally, keep an eye on macroeconomic volatility. Factors like high inflation, rising interest rates, and currency fluctuations can significantly increase borrowing costs, reducing a buyer’s liquidity and their ability to pay international suppliers.

"Country risk encompasses transfer and convertibility risk (i.e. the risk a government imposes capital or exchange controls that prevent an entity from converting local currency into foreign currency and/or transferring funds to creditors located outside the country) and cases of force majeure (e.g. war, expropriation, revolution, civil disturbance, floods, earthquakes)."

– Organisation for Economic Co-operation and Development (OECD)

Step 4: Check Trade History and Set Credit Limits

After assessing financial and country risks in the earlier steps, it’s time to dive into the buyer’s trade history. This step offers a practical look at how reliable the buyer is when it comes to payments. While financial statements can give you a sense of their cash flow, trade references provide a real-world snapshot of how they handle their obligations to suppliers. Some buyers may have strong bank credit lines but still struggle with managing supplier credit. That’s why feedback from other vendors is invaluable. These trade insights, combined with financial data, help you fine-tune credit terms and maintain ongoing risk management.

Review Payment Patterns with Other Suppliers

To evaluate a buyer’s payment behavior, gather 2–3 trade references using a standardized Trade Reference Form. This form should include details like the length of the supplier’s relationship with the buyer, the highest amount repaid in the last 12 months, and payment performance (categorized as Prompt, 30 days late, 60 days late, or 90+ days late). In international trade, a buyer is generally considered "prompt" if they pay within 30 days of the invoice due date.

"While your customer’s financials can show a healthy cash flow, references from other suppliers exhibit how they have been actually paying their invoices." – Jennifer Simpson, Regional Director at EXIM Bank

Keep an eye on Days Beyond Terms (DBT), as outlined in Step 2. Pay special attention to any spikes or significant delays compared to previous years – like if a buyer suddenly takes three times longer to pay than before. It’s also a good idea to verify the buyer’s legal standing through third-party reports to uncover any lawsuits, judgments, or ownership changes. Additionally, historical shipment data can provide useful context, such as consignment dates and items purchased.

Once you’ve confirmed their payment behavior, you can confidently set credit limits that match the buyer’s risk level.

Set Credit Limits Based on Risk Factors

Categorize buyers into low, medium, and high-risk groups based on their trade history and financial health. Assign credit limits that reflect these risk levels. Be cautious not to set limits that far exceed the buyer’s historical purchasing patterns or their highest repaid credit with other suppliers. For credit limits exceeding $100,000, request recent certified financial statements to ensure accuracy.

Leverage real-time monitoring tools to automatically adjust credit limits as a buyer’s financial health or market conditions shift. If a buyer has limited trade history, consider alternatives like Letters of Credit or Export Factoring to mitigate potential insolvency risks. For buyers with a strong payment track record, establish a master sales agreement to clearly define lending terms and reduce the chance of disputes down the line. By keeping credit limits flexible and responsive to market changes, you can manage exposure while still supporting dependable buyers as they grow.

Step 5: Monitor Buyer Activity and Manage Risk

Managing credit risk isn’t a one-and-done task – it’s an ongoing process. A buyer’s financial stability can shift for various reasons, from internal challenges like the passing of a key owner or a lack of succession planning to external factors such as political unrest. By pairing established credit limits with continuous monitoring, you can respond quickly to emerging risks.

Track Changes in Financial and Trade Behavior

Using CRM tools can help you spot changes in a buyer’s transaction patterns that may signal increased risk. For example, watch for behaviors like sudden spikes in order volumes, delayed communication (e.g., a buyer who usually responds in 24 hours now takes days), or partial and late payments. These red flags often appear well before a buyer defaults.

"A good credit score does not necessarily mean a customer is a low risk." – Allianz Trade

Another key metric to monitor is a buyer’s debt-to-income ratio. If this ratio shows a steady upward trend over several years, it could mean their creditworthiness is declining. Advanced tools can simplify this process by analyzing customer profiles against vast datasets, automatically flagging potential risks that might otherwise go unnoticed.

While keeping an eye on buyer behavior can reveal early warning signs, it’s wise to pair this vigilance with an added layer of protection: trade credit insurance.

Use Trade Credit Insurance for Protection

Even with diligent monitoring, some risks can’t be entirely avoided. That’s where trade credit insurance comes in – it safeguards your cash flow against buyer insolvency and political disruptions. This is especially critical in international trade, where recovering funds from a defaulting buyer can be particularly challenging.

Credit insurers track millions of buyer relationships and transactions worldwide, offering insights and data that most businesses wouldn’t have access to on their own. Plus, having insured receivables can improve your financing terms, making it easier to secure funding. If you’re exploring this option, resources like CreditInsurance.com can guide you in understanding how trade credit insurance works and selecting the right coverage for your needs.

Conclusion

Evaluating international buyer risk calls for a clear, data-focused approach. Incorporating advanced credit scoring tools into five key steps – verifying buyer authenticity, examining financial records, evaluating country-specific risks, reviewing trade history, and maintaining ongoing oversight – turns uncertainty into well-informed actions. This method simplifies complex risk data into practical insights.

Global trade comes with its fair share of challenges. From buyer insolvency to political instability, currency swings, and regulatory shifts, each factor can disrupt cash flow. To mitigate these risks, gathering data from various sources – such as bank references, credit reports, and government ratings – is crucial for identifying fraud and assessing potential hazards. With ever-changing markets and shifting political landscapes, regular monitoring and trade credit insurance serve as indispensable safety nets.

"Credit insurance is an essential shield that protects against risks associated with payment defaults"

– Coface

FAQs

What’s the fastest way to spot an international buyer scam?

When navigating early negotiations in international trade, it’s crucial to stay alert for warning signs. Be wary of inflated financial figures, irregular trade patterns, or any indications of fraudulent activity. To verify a company’s legitimacy, start by checking their registration details, reaching out to references, and reviewing credit reports.

Requesting recent financial statements and directly contacting references can help uncover potential inconsistencies. Additionally, tools like shipment data and credit reports offer a quick way to evaluate a company’s credibility. Spotting these red flags early can significantly lower the risk of falling victim to scams.

How do I set a safe credit limit for a new overseas buyer?

When determining a safe credit limit for a new overseas buyer, it’s important to dig into their financial stability. Start by reviewing their credit reports, financial statements, and payment history. These offer a clear picture of their financial health and reliability.

It’s also helpful to reach out to other suppliers for references and examine the buyer’s payment behavior. This can reveal patterns that might not show up in reports. Don’t overlook country-specific risks either – factors like political instability or economic challenges in their region can impact their ability to pay.

For buyers with limited history, tools like credit scoring systems and credit insurance can add an extra layer of insight. These resources help you make a more informed decision and minimize potential risks when setting a credit limit.

When should I use trade credit insurance for international receivables?

Trade credit insurance can be a smart choice for safeguarding your international receivables. It offers protection against risks like non-payment, customer insolvency, or even political instability in foreign markets. This type of coverage becomes especially important when you extend credit terms to overseas buyers. By reducing the financial impact of potential losses, trade credit insurance helps maintain steady cash flow, even in unpredictable global economic climates. This way, your business can stay financially secure while navigating the complexities of international trade.