Accounts receivable insurance protects your business when customers fail to pay for goods or services. It ensures steady cash flow by covering 80% to 95% of unpaid invoices. Whether you’re dealing with customer insolvency, payment delays, or political risks in international trade, this insurance shifts the financial burden to an insurer. Here’s why it matters:

- Risk Protection: Safeguards against customer bankruptcy, protracted defaults, and political disruptions.

- Cash Flow Stability: Guarantees payment recovery, turning uncertain revenue into predictable income.

- Growth Opportunities: Enables offering competitive credit terms and improves access to financing.

- Cost Efficiency: Premiums typically range from 0.1% to 1% of insured sales.

This coverage not only minimizes financial risks but also supports business growth by improving credit management and access to funding.

Trade / Credit Insurance (Account Receivables Insurance) | BearStar Insurance

sbb-itb-b840488

How Accounts Receivable Insurance Works

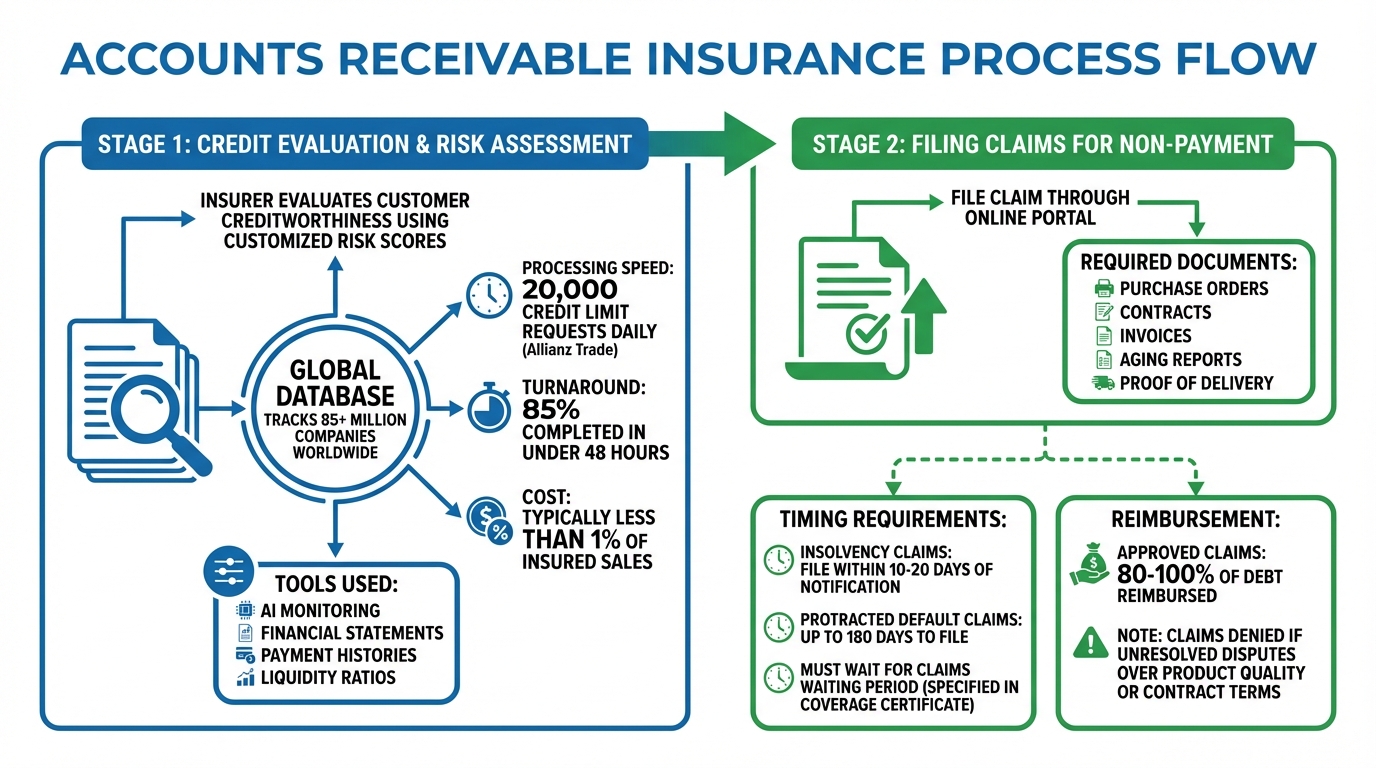

How Accounts Receivable Insurance Works: Credit Evaluation to Claims Processing

Accounts receivable insurance operates in two main stages: credit evaluation and claims processing. Essentially, the insurer acts as an extension of your credit team, helping you assess which customers are safe to extend credit to and stepping in to cover losses when payments fall through. This approach combines proactive risk assessment with responsive claims management.

Credit Evaluation and Risk Assessment

Before you extend credit to a customer, the insurer evaluates their creditworthiness using customized risk scores. These scores are based on global databases – some tracking over 85 million companies worldwide – and supplemented with local market insights from numerous countries. Specialized underwriters dive into financial statements, payment histories, liquidity ratios, and current market trends to assign specific credit limits for each buyer. Advanced AI tools also monitor patterns in behavior and alternative data sources to flag potential risks.

For instance, Allianz Trade processes around 20,000 credit limit requests daily, completing 85% of them in under 48 hours.

The cost of this coverage is typically less than 1% of insured sales, although premiums vary depending on factors like your industry, customer locations, and prior losses. This risk intelligence allows you to make quicker, data-driven decisions about extending credit to new or uncertain buyers, all while freeing up your internal resources.

Once credit is granted, the focus shifts to managing claims in case of non-payment.

Filing Claims for Non-Payment

If a customer fails to pay, you can file a claim through the insurer’s online portal. To do so, you’ll need to provide key documents, such as purchase orders, contracts, invoices, aging reports, and proof of delivery.

Timing is critical. For insolvency claims, you often need to file within 10 to 20 days of notification. For protracted default claims – cases where customers are slow to pay – you may have up to 180 days. Your policy will outline a "claims waiting period" in the Coverage Certificate, which must pass before the claim is eligible for payment. Once approved, the insurer typically reimburses 80% to 100% of the debt, depending on your policy terms.

However, insurers won’t pay claims if there’s an unresolved dispute over product quality or contract terms. Such disputes must be legally resolved first. Additionally, it’s crucial to ensure you’re filing claims against the correct legal entity, especially when dealing with subsidiaries. If you negotiate a repayment plan with a delinquent customer, you’ll need written approval from the insurer.

This process helps protect your business from financial losses while ensuring compliance with policy terms.

Risks Covered by Accounts Receivable Insurance

After understanding the claims process, it’s important to know the specific risks that accounts receivable insurance protects against. This type of insurance safeguards your business from three major threats that can disrupt cash flow.

Customer Insolvency or Bankruptcy

If a customer files for bankruptcy or enters receivership, your business could lose the outstanding payments owed. Accounts receivable insurance steps in to cover this loss, shifting the financial burden from your company to the insurer. This protection ensures your cash flow remains steady.

"By protecting your own company’s interests with a comprehensive credit insurance policy, you are guaranteeing the ability of your business to continue high levels of production, sales and profitability despite your customers’ difficulties."

– 1st Commercial Credit

Insurers also keep an eye on your customers’ financial health, offering early warnings if their creditworthiness starts to decline. With this insight, you can adjust credit terms or request upfront payments, minimizing your risk before insolvency occurs.

Protracted Default and Non-Payment

Sometimes, customers fail to pay on time without declaring bankruptcy. This is where coverage for protracted default comes into play. It protects your business against delays in payment when customers remain solvent but fail to meet their obligations within the agreed timeframe. Businesses dealing with longer payment cycles or clients with inconsistent payment habits benefit greatly from this type of protection.

Political Risks in Export Transactions

Engaging in international trade exposes businesses to risks beyond customer credit issues. Political risk coverage shields your business from losses caused by government actions like currency inconvertibility, trade embargoes, or even war and riots. For instance, if a government freezes currency conversion, the insurer compensates for the loss.

"International trade carries added risk, from political instability to foreign exchange challenges. For exporters, accounts receivable insurance doubles as a safeguard against both commercial and political risks."

– Securitas Global Risk Solutions

The Export-Import Bank of the United States (EXIM) provides coverage for 85% to 95% of the invoice amount on foreign receivables. Some policies also include pre-shipment endorsements, which protect manufacturing costs if political events prevent delivery of customized goods. Political risk claims are typically resolved within 60 days after filing. This coverage ensures that your cash flow remains reliable, even during global disruptions.

| Risk Category | Events Covered | Typical Indemnity |

|---|---|---|

| Commercial Risk | Insolvency, Bankruptcy, Protracted Default | 80–90% of invoice value |

| Political Risk | Currency inconvertibility, Trade embargoes, War, Riots, Expropriation | 85–95% of invoice value |

Cash Flow Benefits of Accounts Receivable Insurance

Accounts receivable insurance offers a game-changing advantage: it transforms unpredictable revenue into dependable cash flow. With 80% to 95% of your invoice value guaranteed even if a customer defaults, your business gains the confidence to plan operations without the constant worry of payment risks.

Maintaining Predictable Cash Flow

This type of insurance turns uncertain payments into assured cash, allowing you to forecast revenue more accurately. You can commit to future investments without the fear of unexpected gaps in income. Without this safety net, a single customer default could create financial pressure that demands significant new sales to recover.

By guaranteeing payment recovery, accounts receivable insurance keeps your cash flow steady, even when customers fail to pay. It also reduces the need for large bad debt reserves, which can otherwise tie up valuable resources.

Reducing Bad Debt Write-Offs

Instead of writing off unpaid invoices as complete losses, you transfer the risk of non-payment to the insurer. This means you can reduce the "allowance for doubtful accounts" on your balance sheet and redirect those funds into working capital.

"Before credit insurance, I was not sleeping at night. This product is changing the way we do business."

– Mike Libasci, President, International Fleet Sales

The cost of premiums, typically ranging from 0.2% to 1% of receivables, is a small price compared to the financial hit of a major default. For instance, a business with $1,000,000 in receivables might pay between $2,000 and $10,000 annually for robust coverage. By minimizing write-offs, your financial standing improves, which can also enhance your ability to secure credit.

Improving Access to Financing

Insured receivables are viewed as lower-risk collateral by banks, which can significantly boost your borrowing power. While lenders often advance 70% to 80% of uninsured domestic receivables, having insurance can increase advance rates to as much as 90%. For export sales, where banks may not advance anything on uninsured foreign receivables due to high risk, insured receivables can also fetch advance rates up to 90%.

You can even designate your lender as a beneficiary under the policy, giving banks direct assurance of payment in case of customer defaults. This arrangement often leads to higher credit limits and lower interest rates, providing additional capital for growth and day-to-day operations.

"Banks typically limit what you can borrow based on the perceived risk of international receivables, concentration of sales to large customers, or age of certain accounts. When your domestic and international receivables are covered… you may be able to borrow more – often at more favorable rates."

– Allianz Trade

Types of Accounts Receivable Insurance Policies

Maintaining steady cash flow is crucial for any business, and accounts receivable insurance offers several tailored options to help manage risks tied to customer payments.

Whole Turnover Coverage provides insurance for all your accounts receivable across your entire customer base. This comprehensive approach is ideal for businesses with a wide range of clients, offering broad protection. Additionally, having your entire receivables insured can make these assets more appealing as collateral when seeking financing.

Key Accounts Coverage zeroes in on your largest customers. If a significant portion of your revenue comes from just a few clients, this policy protects against major losses without requiring you to insure every account. It’s an efficient solution for businesses with concentrated risk in a handful of key relationships.

Single Buyer Coverage is designed to protect against the default of one specific customer. This is particularly useful for businesses heavily reliant on a single major account or those looking to secure better credit terms. Coverage can be as high as 90% for private buyers and up to 100% for sovereign buyers.

For businesses handling occasional large transactions, Transactional Coverage offers protection on a per-deal basis. This option works well for one-time big orders or sales to new customers, especially in high-risk markets or when dealing with buyers who have limited credit histories.

These options allow you to customize your coverage to match your business’s specific needs, ensuring your risk management plan supports consistent cash flow.

Setting Up Accounts Receivable Insurance

Assessing Your Insurance Needs

Before diving into a policy, it’s crucial to evaluate your business’s specific risks. Start by examining your customer concentration. If a significant portion of your revenue hinges on just a few clients, consider how your business would handle the financial hit of unpaid invoices from those accounts. This evaluation can help you decide whether you need broader whole turnover coverage or if focusing on key accounts coverage is a smarter choice.

Take a close look at your payment patterns too. Are certain clients consistently late in paying? Prolonged delays can wreak havoc on your cash flow and make it harder to meet your own financial obligations. If your business involves exporting, factor in geographic and political risks. Consider the stability of the countries you’re selling to, keeping an eye on issues like political unrest, trade restrictions, or currency fluctuations.

When you’re ready to apply, gather essential documents for underwriters. These typically include a description of your product, average credit terms, a list of your top 15 customers, a breakdown of domestic versus export sales forecasts, and a record of recent losses. This information helps insurers assess your risk profile and creditworthiness. Once your application is submitted, insurers can often craft a policy and provide a quote within about a week.

Premiums usually fall between 0.10% and 0.20% of your total sales, depending on your risk profile. Policies often cover 80% to 90% of an invoice’s value, and the premiums may even be tax-deductible for your business. By preparing thoroughly, you can streamline the process and get the coverage you need with ease through CreditInsurance.com.

Working with CreditInsurance.com

After evaluating your needs, CreditInsurance.com offers tools to simplify the entire process. Their platform allows you to compare policies side-by-side, breaking down costs, processing times, and coverage options. This makes it easy to prioritize what matters most to your business – whether that’s lower premiums, faster claims, or robust international coverage.

The site also features an online learning portal and glossary to demystify technical terms like "protracted default" and "insolvency". Additionally, they offer hypothetical examples to show how insurance can protect your business in situations like late payments, customer insolvency, or political instability.

For more tailored support, CreditInsurance.com connects you with specialists who can craft custom solutions based on your business’s unique needs. These experts go beyond generic policies to help you decide whether trade credit insurance or a specialized policy is the better option. Plus, quotes are typically free and come with no obligation to commit.

Conclusion

Accounts receivable insurance transforms one of your company’s largest assets – often accounting for 40% of total assets – from a vulnerable IOU into a secure revenue stream. By covering losses caused by customer insolvency, bankruptcy, or prolonged non-payment, it helps stabilize cash flow and reduces the uncertainty that comes with extending credit.

Consider this: for a business with a 5% profit margin, a $100,000 non-payment could require generating $2,000,000 in new sales just to recover the lost profit. By transferring this risk off your balance sheet, accounts receivable insurance frees up capital that would otherwise be tied up in bad debt reserves, softening the blow of significant write-offs.

This type of coverage also opens doors to better financing opportunities. Lenders often view insured receivables as high-quality collateral, which can lead to larger credit lines, lower interest rates, and more flexible working capital arrangements. When combined with the confidence to extend credit to new or higher-risk customers, this creates a strong foundation for long-term growth.

"Accounts receivable insurance protects cash flow, strengthens financing options, and reduces the impact of customer defaults, making it an essential risk management tool for businesses of all sizes." – Kirk Elken, Co-founder, Securitas Global Risk Solutions

Premiums for accounts receivable insurance typically range from a fraction of one percent to just a few percentage points of insured sales, while coverage often protects 80% to 95% of invoice values. With such a clear cost-benefit ratio, the decision becomes straightforward. CreditInsurance.com offers the resources and expertise to help you create a policy aligned with your specific risk profile, turning accounts receivable from a potential vulnerability into a strategic asset.

FAQs

What invoices aren’t eligible for a claim?

Invoices cannot be claimed if they are tied to disputes over product quality or contractual disagreements with customers. Similarly, any losses stemming from damage to accounts receivable records – whether due to events like a fire or a flood – are excluded from coverage.

How fast do insurers set credit limits for new customers?

When insurers set credit limits for new customers, they typically evaluate several factors, including the customer’s financial stability, payment history, and the risks associated with their industry. Based on this assessment, the insurer may grant a full credit limit, a partial one, or even deny it altogether. The entire process is usually completed quickly, although the exact timeframe depends on the insurer’s specific evaluation methods.

Can this insurance help me get a bigger bank line of credit?

Accounts receivable insurance can play a key role in helping you secure a larger bank line of credit. By bolstering your financial statements and increasing the value of your collateral, it provides lenders with greater confidence. This reduced risk for the bank often translates into higher advance rates and more favorable financing terms, making it easier for your business to access the capital it needs.