ESG reporting is now a must-have for businesses, especially those relying on trade credit insurance. Why? Insurers are integrating ESG factors into underwriting, directly impacting premiums and coverage. This means your company’s sustainability practices and data transparency can influence creditworthiness and access to insurance.

Here’s what you need to know:

- What is ESG reporting? It’s about disclosing measurable data on environmental, social, and governance factors like emissions, labor practices, and board accountability.

- Why does it matter? Poor ESG performance can hurt your business, from regulatory fines to reputational damage. Insurers now use ESG data to assess risks and set terms.

- Regulatory trends: ESG disclosures are becoming mandatory worldwide. Key frameworks include IFRS S1 & S2 (global), the EU’s CSRD (double materiality), and California’s SB 253/SB 261 (climate-focused).

- Impact on trade credit insurance: Strong ESG performance can lead to better terms, while weak practices may result in higher premiums or reduced coverage.

To stay ahead, businesses must build an ESG strategy that includes robust data systems, clear reporting standards, and compliance with global and local regulations. Insurers increasingly expect this level of commitment to sustainability.

Take action now: Treat ESG data with the same rigor as financial data, align with global frameworks, and prepare for external audits. This isn’t just compliance – it’s about staying competitive in a market where ESG is reshaping the rules.

ESG Reporting 101: How to Read & Understand It

sbb-itb-b840488

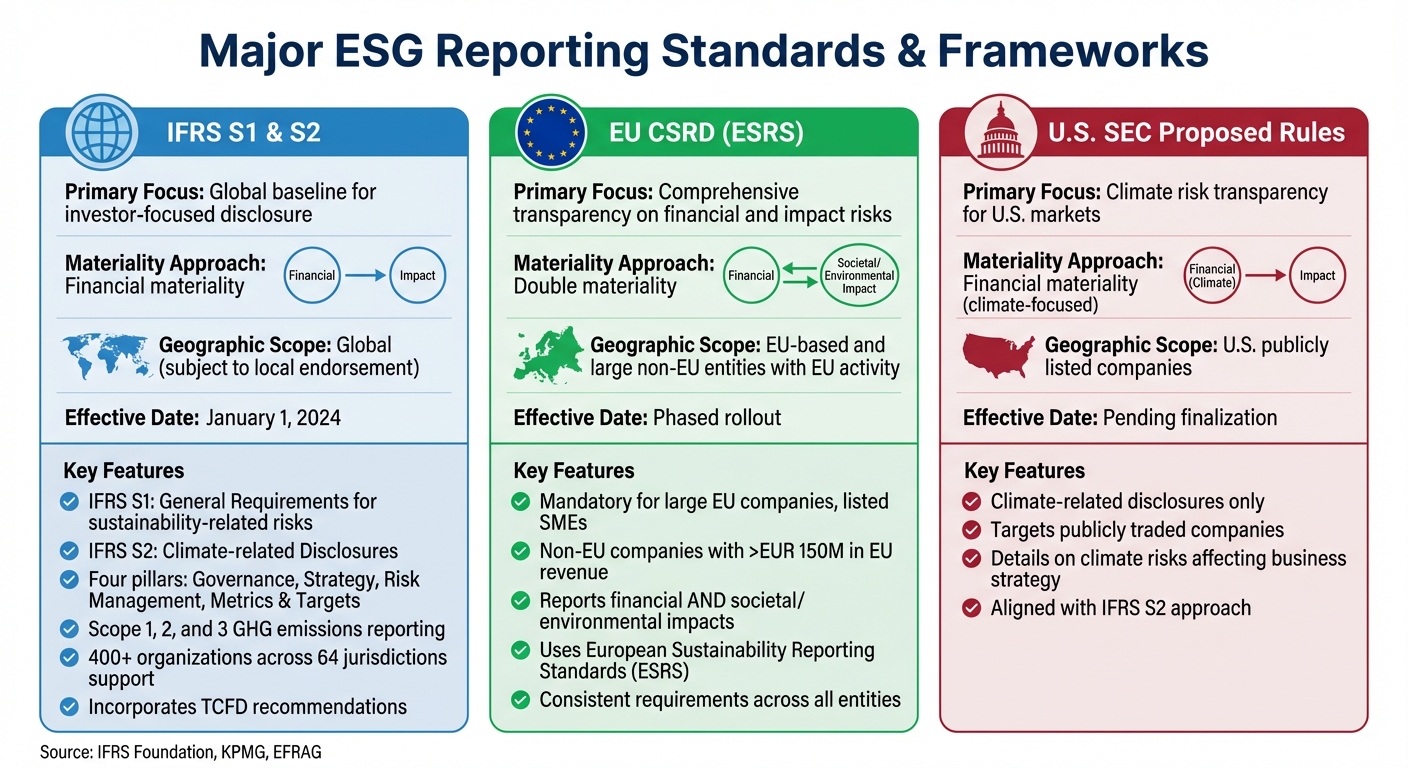

Major ESG Reporting Standards and Frameworks

Comparison of Major ESG Reporting Frameworks: IFRS, EU CSRD, and US SEC Rules

When it comes to trade credit insurance, three main ESG frameworks guide how companies report their sustainability efforts. These frameworks outline what needs to be disclosed, the methods for doing so, and the intended audience. Each has distinct requirements and applies to different regions, shaping the way companies approach ESG reporting.

IFRS Sustainability Standards (IFRS S1 and S2)

The International Sustainability Standards Board introduced IFRS S1 and S2 to provide a global foundation for ESG reporting. These standards officially apply to annual reporting periods starting on or after January 1, 2024, with the first reports expected in 2025. Over 400 organizations across 64 jurisdictions have already expressed their support for these standards.

- IFRS S1 focuses on General Requirements, requiring companies to disclose material information about risks and opportunities related to sustainability that could impact their cash flow, financing, or capital costs.

- IFRS S2 zeroes in on Climate-related Disclosures, covering both physical risks (like severe weather) and transition risks (such as regulatory changes). It also mandates the reporting of Scope 1, 2, and 3 greenhouse gas emissions, though companies have a one-year grace period for Scope 3 reporting during the initial phase.

Both standards are built around four main pillars: Governance, Strategy, Risk Management, and Metrics and Targets. They emphasize financial materiality – focusing on information that influences decisions made by investors and lenders. This approach helps insurers assess how effectively a company manages long-term risks that might affect its ability to meet financial commitments.

"The objective of IFRS S1… is to require an entity to disclose information about its sustainability-related risks and opportunities that is useful to primary users of general purpose financial reports in making decisions relating to providing resources to the entity."

The IFRS standards fully incorporate the Task Force on Climate-related Financial Disclosures (TCFD) recommendations, effectively replacing TCFD’s independent framework. For industries like insurance, asset management, and banking, IFRS S2 also includes specific requirements for reporting "financed emissions".

In their first reporting year, businesses can opt for "climate-first relief", focusing solely on climate risks under IFRS S2, while deferring broader disclosures under IFRS S1. For non-climate risks, companies can use SASB Standards for sector-specific guidance.

While IFRS aims to set a global baseline, the EU has implemented its own mandatory framework that addresses both financial and societal impacts.

EU Corporate Sustainability Reporting Directive (CSRD)

The EU’s Corporate Sustainability Reporting Directive (CSRD) introduces a double materiality approach. This means companies must disclose not only how sustainability issues affect their financial performance but also how their activities impact society and the environment. CSRD applies to large EU companies, listed SMEs, and non-EU parent companies generating over EUR 150 million in the EU, provided they have at least one large subsidiary or branch. Unlike IFRS standards, which are voluntary unless adopted into local law, CSRD is mandatory for entities it covers.

The directive uses European Sustainability Reporting Standards (ESRS), which align with the same core areas – governance, strategy, risk management, and metrics. However, ESRS enforces consistent reporting requirements across all entities, without the flexibility offered by IFRS.

"The ESRS applies a double materiality perspective… Unlike the ESRS, IFRS S1 centers solely on financial materiality. This results in a strictly investor-focused definition of materiality."

- KPMG

For U.S. businesses with operations or customers in the EU, CSRD adds another layer to existing domestic reporting requirements. To ease the process, EFRAG and ISSB have worked to align their standards, providing guidance to simplify data collection for both ESRS and ISSB reporting.

While the EU takes a comprehensive approach, the U.S. is narrowing its focus specifically to climate risks.

U.S. SEC Proposed ESG Disclosure Rules

The Securities and Exchange Commission (SEC) has proposed climate-related disclosure rules targeting publicly traded companies in the U.S.. These rules emphasize financial materiality, similar to IFRS standards, but are limited to climate-related risks rather than broader ESG factors.

Under these proposed rules, companies must detail how climate risks affect their business strategies, operations, and financial planning. This information helps insurers assess potential disruptions to cash flow or payment obligations caused by climate-related factors. Businesses already reporting under IFRS S2 may find it easier to adapt once the SEC finalizes its rules.

| Framework | Primary Focus | Materiality Approach | Geographic Scope | Effective Date |

|---|---|---|---|---|

| IFRS S1 & S2 | Global baseline for investor-focused disclosure | Financial materiality | Global (subject to local endorsement) | January 1, 2024 |

| EU CSRD (ESRS) | Comprehensive transparency on financial and impact risks | Double materiality | EU-based and large non-EU entities with EU activity | Phased rollout |

| U.S. SEC Proposed Rules | Climate risk transparency for U.S. markets | Financial materiality (climate-focused) | U.S. publicly listed companies | Pending finalization |

These frameworks not only set clear expectations for ESG reporting but also help insurers evaluate the risks tied to sustainability.

ESG Compliance Requirements by Jurisdiction

ESG criteria are increasingly influencing underwriting practices and risk assessments in trade credit insurance, with jurisdiction-specific mandates adding new layers of complexity. While global ESG reporting frameworks provide a baseline, jurisdictions like California and the European Union (EU) have introduced mandatory regulations that directly impact businesses relying on trade credit insurance. These two regions highlight contrasting approaches to enforcement and scope.

California ESG Regulations

California has taken the lead in the U.S. with mandatory climate disclosure laws, including SB 253 (Climate Corporate Data Accountability Act) and SB 261 (Climate-Related Financial Risk Act). These regulations apply to both public and private companies, affecting an estimated 5,300 entities.

SB 253 mandates that U.S. entities with annual global revenues exceeding $1 billion and "doing business" in California report their Scope 1, 2, and 3 greenhouse gas (GHG) emissions. A company qualifies as "doing business" in California if its sales in the state surpass $757,070 in 2025. The first reporting deadline for Scope 1 and 2 emissions is set for August 10, 2026, with Scope 3 reporting required in 2027. Non-compliance could result in penalties of up to $500,000 per year.

SB 261 targets entities with annual global revenues over $500 million, requiring biennial reports on climate-related financial risks and mitigation strategies that align with frameworks like TCFD or IFRS S2. However, enforcement of SB 261 is currently on hold due to a U.S. Court of Appeals injunction.

"CARB will exercise enforcement discretion for the first reporting cycle, on the condition that entities demonstrate good faith efforts to comply with the requirements of the law."

Insurance companies are exempt from both laws. Under SB 261, insurers report through the National Association of Insurance Commissioners (NAIC) framework, and in February 2026, CARB granted an incremental exemption for insurers under SB 253, though this could be revisited in the future. For businesses purchasing trade credit insurance, these regulations matter as insurers increasingly incorporate ESG data into underwriting, focusing on "insured emissions" and climate-related risks.

| Regulation | Revenue Threshold | Primary Requirement | First Deadline | Max Annual Penalty |

|---|---|---|---|---|

| California SB 253 | > $1 Billion (Global) | Scope 1, 2, & 3 GHG Emissions | August 10, 2026 (Scopes 1 & 2) | $500,000 |

| California SB 261 | > $500 Million (Global) | Climate-related financial risks | Paused (Injunction) | $50,000 |

While California emphasizes emissions reporting with strict penalties, other jurisdictions, like the EU, adopt a broader approach.

EU ESG Disclosure Requirements

The EU’s Corporate Sustainability Reporting Directive (CSRD) takes a more expansive view, requiring disclosures that integrate financial and societal impacts. The CSRD applies to large EU companies, listed small and medium-sized enterprises (SMEs), and non-EU parent companies generating more than EUR 150 million in the EU, provided they have at least one large subsidiary or branch within the region. This means U.S. companies with significant EU operations may be subject to these rules, even if headquartered elsewhere.

Unlike California’s focus on emissions alone, the CSRD employs a double materiality framework. This requires companies to disclose not only how sustainability issues affect their financial performance but also how their activities impact society and the environment.

For businesses utilizing trade credit insurance, CSRD compliance is crucial when insuring EU-based buyers or managing EU subsidiaries. Insurers use ESG disclosures to evaluate long-term sustainability and creditworthiness throughout supply chains. Interestingly, companies already meeting CSRD standards may find it easier to align with California’s requirements, as compliance with the EU’s European Sustainability Reporting Standards (ESRS) is expected to satisfy the minimum criteria of SB 261.

The CSRD is rolling out in phases, with staggered timelines for various entities. However, the direction is clear: mandatory, audit-grade sustainability disclosures are becoming the norm. Businesses operating across multiple jurisdictions may benefit from creating a unified greenhouse gas inventory that satisfies the requirements of multiple frameworks, avoiding the inefficiencies of fragmented reporting.

How ESG Affects Trade Credit Insurance Underwriting

Trade credit insurers are increasingly weaving ESG (Environmental, Social, and Governance) factors into their underwriting processes. This shift is supported by data showing that 44% of insurance CEOs believe ESG programs can improve financial performance. With 96% of G250 companies now reporting on sustainability or ESG-related issues, underwriters have access to a wealth of ESG data. This allows them to uncover risks that traditional financial metrics might miss – such as environmental disruptions, reputational damage, or governance lapses. Below, we’ll explore how ESG considerations are being integrated through industry frameworks and evaluation tools.

Principles for Sustainable Insurance (PSI) Framework

The Principles for Sustainable Insurance (PSI) serve as a guide for incorporating ESG factors across the insurance value chain. Principle 1, in particular, underscores the role of ESG in underwriting:

"We will embed in our decision-making environmental, social and governance issues relevant to our insurance business."

This framework calls for ESG integration into research, modeling, and assessments of capital adequacy. For trade credit insurance, this means evaluating whether a buyer’s ESG track record impacts their ability to meet financial obligations. Insurers also collaborate with clients to better understand and manage ESG risks. ESG has become so central to the process that it’s now referred to as the "4th factor" in credit assessments, complementing traditional financial criteria.

How Insurers Evaluate ESG Risks

Applying these principles, insurers rely on specialized tools to assess and manage ESG risks. One key method is the use of heat maps, which highlight sector-specific ESG risks. These maps allow underwriters to focus on industries with greater sustainability challenges, helping them identify the most pressing risks.

ESG risks are categorized into three main areas, each with direct implications for creditworthiness:

| ESG Category | Specific Underwriting Factors | Why It Matters for Credit Risk |

|---|---|---|

| Environmental | Climate change, pollution, biodiversity loss | Impacts asset value and operational continuity |

| Social | Child labor, human rights, workplace safety | Avoids reputational harm and legal consequences |

| Governance | Bribery, corruption, executive ethics | Reflects management quality and financial integrity |

To address these risks, insurers have established protocols to flag high-risk transactions and conduct senior-level reviews when necessary. Companies with weak ESG practices may face reduced coverage options or even exclusion, safeguarding the insurer’s reputation.

Roger Jackson, Global Insurance ESG Lead at KPMG International, highlights the growing importance of ESG in the industry:

"For insurance leaders, ESG is high on the agenda – and this means that sustainability reporting should be, too. With increasing stakeholder expectations and growing regulatory requirements, getting the sustainability reporting approach right is becoming a major strategic importance."

The push for standardized ESG due diligence is also gaining momentum. Insurers are streamlining their information requests, making it easier for business partners to provide relevant data for specific transactions. Additionally, 50% of digital leaders in the insurance sector cite ESG transparency as a major driver of organizational transformation.

Strong ESG performance can lead to better underwriting terms and greater coverage capacity. By integrating ESG analysis into their decision-making, insurers not only enhance their risk assessments but also align with global sustainability standards that are reshaping trade credit insurance.

How to Build an ESG Reporting Strategy

Creating an ESG reporting strategy requires careful planning, accurate data handling, and clear accountability. With 80% of companies worldwide now reporting on sustainability, businesses using trade credit insurance need a structured approach to navigate both regulatory requirements and insurer expectations. As ESG disclosures shift from voluntary to mandatory and standardized, building your strategy on a solid foundation from the start is non-negotiable.

Conducting an ESG Readiness Assessment

Start by evaluating your current ESG processes, internal controls, and data collection methods. This baseline assessment helps you understand what’s already in place and where improvements are needed.

Map out the regulatory requirements relevant to your business and conduct a gap analysis to pinpoint missing data, particularly around Scope 3 emissions and social metrics. These areas often involve supply chain risks, which are critical for businesses reliant on trade credit insurance. Collaborate early with your audit and legal teams to prepare for mandatory assurance. As Chirag Shah, Partner and Sustainability Leader for Insurance at KPMG in the UK, explains:

"Sustainability reporting has become commercially and strategically important and offers a number of potential benefits to those who can successfully integrate it into their operating model."

Engage stakeholders – trade credit insurers, investors, and customers – early in the process. Understanding their sustainability expectations upfront can save time and resources later. You might also consider pre-assurance diagnostics to evaluate your readiness for external verification, especially as mandatory assurance is becoming more common in many regions.

Once you have a clear baseline, the next step is to identify the ESG issues that matter most to your business and its stakeholders.

Identifying Material ESG Topics

Not all ESG factors are equally important to your operations. A double materiality assessment – evaluating both the financial impact on your business and the environmental and societal impact of your activities – forms the backbone of modern ESG reporting. This step is particularly important for insurers assessing your sustainability and creditworthiness.

Consult key stakeholders like investors, lenders, and insurers to identify ESG risks that could affect your creditworthiness and resilience. For businesses using trade credit insurance, material topics often include carbon footprints, labor rights, and governance ethics – factors that directly influence your ability to meet financial obligations.

Use industry-specific frameworks, such as SASB (now part of ISSB), to identify ESG issues that are financially relevant to your sector. A materiality matrix can help you prioritize these issues by comparing their importance to stakeholders against their impact on your business.

Focus on measurable outcomes rather than vague commitments. Insurers and lenders increasingly expect concrete metrics, such as kilowatt-hours of energy consumption, Scope 1-3 emissions, and workplace safety incident rates.

Once you’ve identified your material ESG topics, the next step is to ensure your data systems can reliably track these metrics.

Setting Up Data Collection and Reporting Systems

ESG data often comes from various departments, ranging from HR to environmental audits. To streamline this, establish a centralized ESG data management team. Tyler Thomas, Sustainability Lead at AArete, highlights the importance of standardizing data collection:

"ESG data usually lives across numerous departments, which are used to managing data in various ways, and standardizing the ESG data capture is crucial for having consistent insights."

Start by creating an inventory of your data sources. Map out where data is stored, how it’s collected, and assess its reliability. Address any gaps and determine where the data will reside long-term. Assign specific roles – such as Information Owners for data quality, Disclosure Owners for reporting, and Validators for independent review – to ensure ESG data is treated with the same rigor as financial data.

Leverage automation where possible. Automated tools can simplify data extraction from external systems, while IoT sensors can provide real-time tracking for metrics like energy and water usage. Replace manual, spreadsheet-based methods with ESG software to improve accuracy and efficiency. However, technology alone isn’t enough – reliable and complete data is the real key.

Create a centralized dashboard to act as a single source of truth for ESG metrics. This allows stakeholders to monitor performance against goals in real time. Ensure your systems maintain detailed audit trails and include documented sources for all data points, especially when using public data for estimates. With 94% of investors believing that corporate reporting includes unsupported sustainability claims, being audit-ready is critical for maintaining trust.

Finally, establish a recurring ESG reporting schedule with clear internal milestones to avoid last-minute compliance issues. Regular validation through internal audits and external reviews will help maintain credibility and reduce the risk of greenwashing. Train staff across finance, legal, and operations on ESG standards to ensure alignment and minimize data risks, creating a cohesive approach to reporting across your organization.

Conclusion

ESG reporting has shifted dramatically – from being a voluntary act of goodwill to becoming a core requirement for businesses, particularly those utilizing trade credit insurance. Today, 86% of large companies worldwide disclose sustainability information, and ESG-mandated assets are projected to hit $35 trillion. This evolution underscores its growing importance. As George Chmael II, Founder & CEO of Council Fire, aptly explains:

"ESG reporting has transitioned from a voluntary demonstration of corporate responsibility to a fundamental requirement for capital market participation."

For businesses relying on trade credit insurance, ESG performance now plays a critical role in underwriting decisions and creditworthiness evaluations. Companies with strong ESG practices can benefit from lower premiums, customized coverage options, and improved access to capital. In fact, 70% of insurance underwriters are already integrating – or planning to integrate – ESG factors into their underwriting strategies.

Beyond insurance, ESG reporting offers businesses a competitive advantage. It enhances funding opportunities, builds stronger relationships with ESG-conscious clients and investors, and fosters trust through transparency. With 80% of investors viewing ESG as vital to their decisions and 70% of companies feeling heightened market pressure to embrace sustainability, proactive ESG initiatives can set businesses apart in a marketplace increasingly driven by these values.

At the same time, regulatory demands are becoming more stringent. From the EU’s CSRD to California’s SB 253 and the global adoption of ISSB standards, mandatory ESG disclosures are no longer optional. Yet, only 29% of investors believe current corporate reporting fully reflects ESG’s real business impact. Companies that invest in robust data systems, conduct double materiality assessments, and prepare for external assurance will be better equipped to meet these growing expectations. High-quality ESG data not only ensures compliance but also strengthens market positioning.

CreditInsurance.com offers resources to help businesses navigate the intersection of ESG and trade credit insurance. By treating ESG data as rigorously as financial data and aligning reporting with established frameworks, companies can turn compliance into a strategic tool – bolstering resilience, improving risk management, and securing their place in the evolving world of trade finance.

FAQs

Which ESG framework should my company follow first?

When deciding on the best ESG framework, it’s important to consider your industry, regulatory environment, and what matters most to your stakeholders. Many U.S.-based companies start by following domestic standards for sustainability reporting to ensure compliance with local requirements. On a broader scale, globally recognized frameworks like SASB (Sustainability Accounting Standards Board) or TCFD (Task Force on Climate-related Financial Disclosures) are great options. These frameworks are widely acknowledged by investors and regulators for their thorough approach. The key is to select one that aligns well with your company’s size, sector, and objectives.

What ESG data do trade credit insurers request most often?

Trade credit insurers often seek ESG data to evaluate environmental risks like the effects of climate change and exposure to natural disasters. They also examine social and governance factors that influence a company’s ability to fulfill its financial commitments and uphold responsible practices. This information plays a key role in analyzing financial health and risk management strategies.

How can we get audit-ready for Scope 3 emissions reporting?

To get ready for Scope 3 emissions audits, prioritize improving the quality of your data, keeping detailed records, and setting up solid controls. Build emissions inventories that are clear, traceable, and meet compliance standards. Focus on managing supply chain data effectively, ensuring it aligns with global requirements, and routinely reviewing evidence files as well as internal controls. Taking these steps will help make sure your emissions data is reliable and ready for audit processes.