Expanding your business credit line can be challenging, especially when unpaid invoices create financial uncertainty. Trade credit insurance provides a practical solution by protecting your business from customer non-payment risks. Here’s why it matters:

- Improves Financing Terms: Insured receivables are seen as secure collateral, increasing advance rates from 70-75% to 80-90%.

- Reduces Risks: Covers losses from customer insolvency, bankruptcy, or political disruptions, including international transactions.

- Lowers Costs: Premiums typically range from 0.1% to 0.7% of insured sales, freeing up capital tied in bad debt reserves.

- Supports Growth: Enables extending credit to new customers and entering international markets with confidence.

Trade credit insurance not only protects your receivables but also strengthens your financial position, making it easier to secure loans, reduce interest rates, and seize growth opportunities. With this policy, you can manage risks effectively and focus on scaling your business.

What is Trade Credit Insurance? | Credit Insurance explained in 5 minutes

sbb-itb-b840488

What Is Trade Credit Insurance and How Does It Work?

Trade credit insurance, often called accounts receivable insurance, is a financial safety net for B2B companies. It protects businesses from losses when customers fail to pay for goods or services provided on credit. By covering unpaid invoices, it helps stabilize cash flow and reduce financial uncertainty.

When you purchase this type of insurance, the insurer actively monitors your customers’ financial health and assigns credit limits to each buyer. If a customer becomes insolvent, files for bankruptcy, or simply doesn’t pay within a set timeframe (called "protracted default"), the insurer steps in to reimburse you – usually covering 85% to 95% of the unpaid amount. Beyond business failures, trade credit insurance also shields you from political risks, such as trade embargoes, currency restrictions, or civil unrest, which can disrupt payments – making it particularly valuable for companies working with international clients.

What Trade Credit Insurance Covers

Trade credit insurance typically addresses two types of risks: commercial risks and political risks.

- Commercial risks include situations like customer insolvency, bankruptcy, or prolonged non-payment.

- Political risks cover non-payment caused by events like war, government-imposed trade restrictions, or currency issues in the buyer’s country.

Policies are customizable to fit specific business needs. For instance:

- Whole Turnover coverage protects all your domestic and international sales.

- Key Accounts policies focus on your most important customers.

- Single Buyer coverage targets one high-value or high-risk transaction.

In 2019, the global trade credit insurance market was valued at $9.39 billion and is expected to grow to $18.14 billion by 2027. This growth highlights how essential this insurance has become for managing business risks.

To maintain eligibility for claims, you must report overdue accounts to your insurer within 30 to 90 days of the invoice due date. Missing this window could result in a denied claim, so it’s crucial for your accounting team to work closely with the insurer.

Tailored policies like these not only protect against losses but also enhance your financial standing, making it easier to secure better credit terms and expand your business.

How It Helps Increase Business Credit Lines

One of the key benefits of trade credit insurance is how it enhances your ability to secure business credit. By insuring your receivables, you shift the risk of non-payment to the insurer, making those receivables more appealing to lenders. Banks, for example, are often willing to offer advance rates of up to 90% on insured receivables, even when dealing with higher-risk buyers like foreign clients, concentrated accounts, or new customers. The insurer’s ongoing monitoring and customer credit ratings provide additional reassurance to lenders that your accounts receivable are well-managed.

Another advantage is the ability to reduce or even eliminate bad debt reserves. Unlike reserves, the premiums for trade credit insurance are tax-deductible, freeing up capital that can be reinvested into growth initiatives like inventory, equipment, or new projects. This combination of better financing terms and increased liquidity directly addresses the cash flow challenges many businesses face. In fact, 44% of financial leaders cite unpaid invoices as a primary cause of cash flow disruptions.

How Trade Credit Insurance Improves Financing Terms

Financing Terms With vs Without Trade Credit Insurance

Trade credit insurance doesn’t just protect against risks; it also improves financing terms by turning receivables into reliable, secure assets. When receivables are insured, they become strong collateral, which leads to higher advance rates, reduced interest costs, and more flexible loan agreements. Lenders see insured receivables as dependable assets rather than high-risk liabilities.

Typically, without insurance, lenders offer advances on 70% to 75% of your receivables’ value. With trade credit insurance, this figure increases to 80% to 90%. This shift can reduce interest rate margins by 25 to 75 basis points, translating into noticeable cost savings over time. These improved terms open up more financing opportunities, as explained below.

Using Insured Receivables as Collateral

Lenders often exclude certain receivables – like foreign invoices, concentrated accounts, or sales to new customers – from your borrowing base. Trade credit insurance changes this dynamic. According to the EXIM Bank, "Lenders are often willing to lend against assets otherwise excluded from the borrowing base".

To strengthen the lender’s position, insurers can issue a loss payee endorsement, which ensures claim payments go directly to the lender. For long-term security, consider requesting non-cancellable limits, which prevent insurers from withdrawing coverage during the policy period – a feature lenders highly value. Sharing key policy details, such as buyer limits and credit management procedures, with lenders early on can help you secure better financing terms.

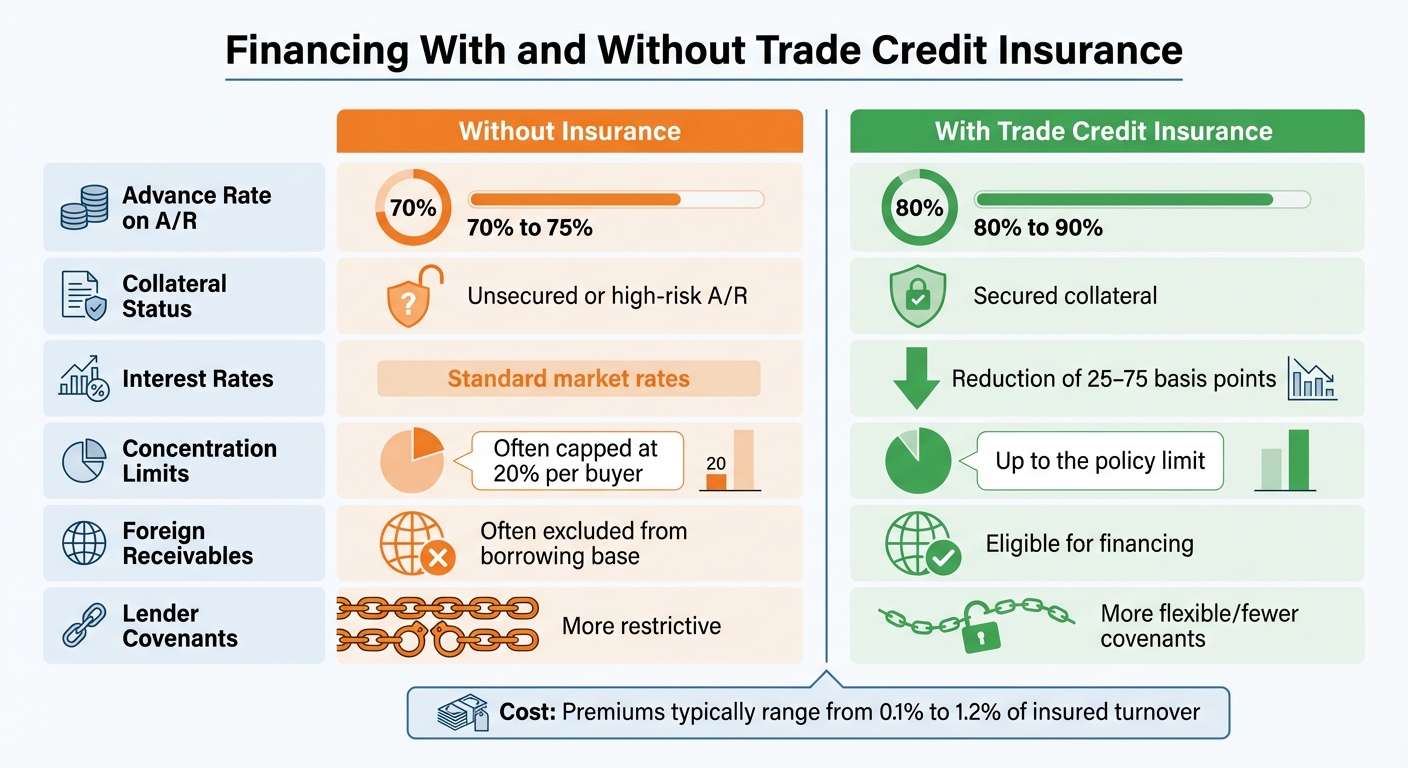

Financing With and Without Insurance: A Comparison

Here’s a breakdown of how financing terms differ when trade credit insurance is in place:

| Feature | Without Insurance | With Trade Credit Insurance |

|---|---|---|

| Advance Rate on A/R | 70% to 75% | 80% to 90% |

| Collateral Status | Unsecured or high-risk A/R | Secured collateral |

| Interest Rates | Standard market rates | Reduction of 25–75 basis points |

| Concentration Limits | Often capped at 20% per buyer | Up to the policy limit |

| Foreign Receivables | Often excluded from borrowing base | Eligible for financing |

| Lender Covenants | More restrictive | More flexible/fewer covenants |

The cost for these benefits is relatively low – premiums generally range from 0.1% to 1.2% of insured turnover, depending on your industry and risk profile.

How Trade Credit Insurance Supports Business Growth

Trade credit insurance plays a key role in helping businesses grow by breaking down barriers to reaching new customers and entering untapped markets. It not only improves access to financing but also provides a way to manage credit risks more effectively.

Reducing Risks When Extending Credit to New Customers

While new customers can drive growth, they often come with risks. Without insurance, businesses might resort to requiring prepayment or offering shorter credit terms to mitigate potential losses – practices that can discourage sales. Trade credit insurance changes the game by shifting the risk from your business to the insurer, enabling you to extend credit with greater confidence.

This insurance also eliminates guesswork when assessing new customers. Instead, objective credit ratings guide your decisions, allowing your sales team to offer competitive terms safely. As Christian Bürger, Senior Editor at Atradius, explains:

"Trade credit insurance enables companies to make better-informed decisions about where to focus their sales efforts, enhancing competitiveness".

By using these insights, your team can identify customers with strong financial health and reliable payment histories. This means you can confidently offer open credit terms, improving cash flow and streamlining the sales process. A pre-approved credit policy further simplifies negotiations, helping close deals faster.

Entering New Markets Safely

Expanding into international markets comes with its own set of challenges. Differences in legal systems, business practices, and payment norms can complicate traditional credit risk assessments. Trade credit insurance steps in to provide detailed creditworthiness analyses for these unfamiliar markets, filling gaps where in-house expertise may fall short.

For businesses looking to enter emerging markets, the insurance also covers political risks. This includes protection against losses caused by factors like currency devaluation, civil unrest, import bans, or government-imposed restrictions. Such coverage ensures that even in unpredictable environments, your business can grow with confidence.

A real-world example highlights this benefit: In July 2025, a U.S. wholesaler used EXIM-backed trade credit insurance to secure an export credit line, leading to a 20% increase in international sales.

And the best part? This protection is surprisingly affordable, with premiums typically ranging from 0.1% to 0.7% of insured sales. With trade credit insurance, businesses can offer flexible payment terms and open-account options in new markets, eliminating the need for costly alternatives like letters of credit or bank guarantees.

How to Optimize Credit Lines with Trade Credit Insurance

Lowering Bad Debt Reserves to Free Up Capital

One of the smartest ways to optimize credit lines is by tapping into the capital that’s often locked away in bad debt reserves. Businesses typically set aside these reserves as a safeguard against customer payment defaults. However, with trade credit insurance, the need for such reserves can be significantly reduced – or even eliminated altogether. This means that money previously tied up can now be put to better use, like purchasing more inventory, hiring additional staff, or scaling up operations.

When receivables are insured, businesses not only free up capital but also gain access to higher advance rates. This added liquidity doesn’t just keep the day-to-day operations running smoothly – it also strengthens your credit management process. Trade credit insurance provides tools that help you manage credit more effectively, creating a win-win situation for growth and financial stability.

Credit Management Tools Included with Insurance

Trade credit insurance does more than just free up funds – it also offers valuable credit management tools that make decision-making easier and faster. For instance, insurers often provide risk ratings that give you a clear, objective view of your customers’ creditworthiness. This allows your team to confidently extend competitive terms to trustworthy buyers while steering clear of riskier accounts.

Many policies also come with global debt collection services, saving your team from the hassle of chasing overdue payments. On top of that, online platforms provided by insurers let you handle tasks like tracking claims, adjusting credit limits, and monitoring performance – all in real time. These features not only simplify credit management but also help you spot potential risks and opportunities to fine-tune your credit lines.

Conclusion: Growing Your Business with Trade Credit Insurance

Using trade credit insurance isn’t just about managing risk – it’s a tool that can actively drive business growth. By turning your receivables into secure collateral, trade credit insurance opens the door to better financing options and greater opportunities for expansion.

Here’s how it works: insured receivables can significantly increase advance rates – from 75% up to 90%. This makes lenders more willing to include these assets in your borrowing base, giving you access to more liquidity. With this added financial flexibility, you can secure lower interest rates, reduce restrictive covenants, and free up cash to fuel growth initiatives. It’s a game-changer for businesses looking to scale.

The benefits don’t stop at financing. Trade credit insurance also empowers your sales team to push boundaries. With coverage of up to 90% of your exposure in case a customer defaults, you can confidently offer more competitive payment terms, explore new markets, and take on larger orders without worrying about undue risk. As Christian Bürger, Senior Editor at Atradius, puts it:

"Trade credit insurance does more than protect against risk, it unlocks opportunities for growth".

Given that over 80% of business failures are tied to cash flow problems, having a strong trade credit insurance policy isn’t just a good idea – it’s a critical step toward sustainable growth. Whether you’re optimizing your current credit lines or exploring new markets, trade credit insurance provides the financial security and flexibility to grow your business with confidence.

FAQs

Will my bank require a loss payee endorsement?

If your business loan is backed by assets – like equipment, property, or even insurance policies – your bank might ask for a lender’s loss payee endorsement. This step helps protect the bank’s financial stake in the collateral. It’s a common requirement when collateral is tied to the loan agreement, ensuring the bank has added security.

What are the common reasons a claim gets denied?

Claims can get denied for a variety of reasons, including disputed invoices, failure to meet claim reporting deadlines, or not following specific reporting requirements. Other common issues include submitting invoices outside of approved payment terms, misinterpreting policy terms, reporting delays, coverage exclusions, disputes between buyers and sellers, or mistakes in the application process. To lower the chances of a claim being denied, it’s essential to stick to policy guidelines and meet all deadlines.

How do insurers set credit limits for each buyer?

Insurers set credit limits by evaluating several key factors tied to a buyer’s financial stability and reliability. They carefully review financial records, consider payment history, assess risks specific to the buyer’s industry, and examine management practices. To make these decisions, they often use a combination of detailed financial documents and sophisticated scoring models to gauge risk and decide on suitable coverage levels.