Trade credit insurance and accounts receivable insurance both protect businesses from financial losses caused by unpaid invoices, but they serve different purposes. Here’s a quick breakdown:

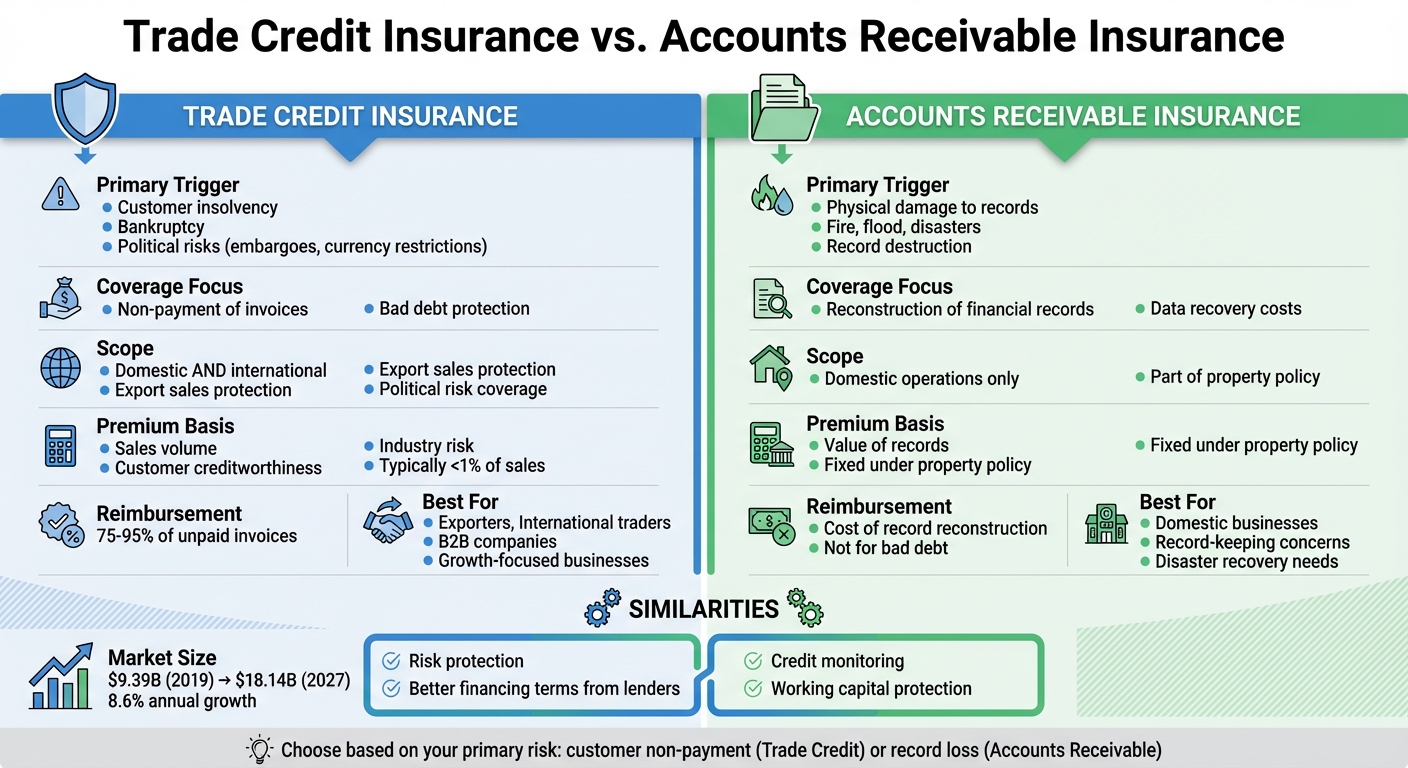

- Trade Credit Insurance: Protects against customer non-payment due to insolvency, bankruptcy, or political risks (e.g., trade embargoes). Ideal for businesses extending credit, especially in international markets.

- Accounts Receivable Insurance: Covers the cost of reconstructing financial records after physical damage (e.g., fire or flood). Typically part of a property insurance policy.

Key Differences:

- Trigger for Coverage: Trade credit insurance focuses on customer non-payment, while accounts receivable insurance addresses physical damage to records.

- Scope: Trade credit insurance protects entire customer portfolios or specific accounts, including international risks. Accounts receivable insurance is limited to domestic operations and record restoration.

- Premium Calculation: Trade credit insurance is based on sales volume and customer risk; accounts receivable insurance is tied to the value of records.

Quick Comparison:

| Feature | Trade Credit Insurance | Accounts Receivable Insurance |

|---|---|---|

| Primary Trigger | Customer insolvency, bankruptcy, or political risks | Physical damage to records |

| Coverage Focus | Non-payment of invoices | Reconstruction of financial records |

| Scope | Domestic and international | Domestic only |

| Premium Basis | Sales volume and customer risk | Value of records under property policy |

For businesses concerned about customer payment risks, trade credit insurance is the better option. If your primary worry is record loss due to disasters, accounts receivable insurance under a property policy is more suitable.

Trade Credit Insurance vs Accounts Receivable Insurance Comparison Chart

What Is Trade Credit Insurance?

Trade credit insurance is a safety net for B2B companies, protecting them from financial losses when customers fail to pay for goods or services provided on credit. It covers non-payment caused by insolvency, bankruptcy, or prolonged default. For businesses operating internationally, it also guards against political risks like currency inconvertibility, political unrest, expropriation, or trade embargoes.

Insurers set specific credit limits for each customer based on their financial stability. If a buyer defaults, the policy typically reimburses 85% to 95% of the unpaid invoice, turning uncertain receivables into more reliable assets.

"Trade credit insurance is your financial safety net and is a risk management tool that protects your business from bad debts." – Atradius

But this coverage isn’t just about risk protection. It also brings financial perks, such as better financing opportunities. By converting risky receivables into strong collateral and monitoring customer creditworthiness through buyer ratings, it helps businesses avoid risky partnerships before extending credit. Here’s a closer look at how trade credit insurance makes managing credit risks easier.

Main Features of Trade Credit Insurance

Trade credit insurance offers flexibility to suit your business needs. You can choose to cover your entire customer base, specific groups, or just key clients. This adaptability ensures you can tailor the policy to match your risk profile, whether you have numerous small accounts or a few major clients.

Each policy includes pre-approved credit limits for buyers, determined by the insurer’s evaluation of their financial health. Losses are only covered within these limits, which not only protect your cash flow but also help you make informed credit decisions while safeguarding your capital.

The coverage supports both domestic and export sales. In fact, trade credit insurance underpins over $600 billion in annual U.S. sales and reached a global exposure of EUR 3.5 trillion in 2024.

Additionally, insured receivables give lenders more confidence, enabling you to secure better credit lines and borrowing terms. This allows businesses to offer competitive payment terms to attract larger buyers without locking up capital in reserves or relying on factoring services, which can cost 10% to 30% of the invoice value.

Which Businesses Benefit from Trade Credit Insurance?

Exporters and international traders gain substantial advantages from trade credit insurance, as it addresses political risks like currency restrictions and instability – issues that standard credit management practices can’t cover.

Manufacturers, wholesalers, and service providers with diverse customer bases use this coverage to stabilize cash flow and protect working capital. Businesses heavily reliant on a few key customers – where a single default could have disastrous consequences – find it particularly useful.

For growth-focused companies, trade credit insurance is a game-changer. It allows them to expand into new markets or attract larger buyers by offering generous credit terms without fear of default. The policy provides the confidence to pursue opportunities that might otherwise seem too risky. For example, during the 2020 economic downturn, many businesses turned to trade credit insurance to safeguard themselves against market disruptions and revenue losses.

The cost of coverage is typically less than 1% of sales, with premiums based on factors like trade volume, buyer creditworthiness, industry risk, and payment terms. Payments are often calculated monthly, based on either current sales or outstanding receivables, making it a manageable investment for most businesses.

sbb-itb-b840488

What Is Accounts Receivable Insurance?

Accounts receivable insurance provides protection for businesses when customers fail to pay their invoices due to insolvency, bankruptcy, or prolonged payment delays. This type of insurance focuses specifically on safeguarding receivables, a critical asset for many companies, ensuring they remain protected even in challenging financial situations.

Receivables often make up around 40% of a company’s total assets, making them a significant financial component. When a customer defaults on payment, the insurance policy typically reimburses between 80% and 95% of the invoice amount, reflecting the value of the insured asset. To manage this, insurers evaluate the creditworthiness of each customer and assign credit limits, offering a level of protection that goes beyond standard credit risk management practices.

This coverage also allows businesses to offer open account terms instead of requiring upfront payments, making them more competitive in the marketplace. As Ori Ben-Amotz, CFO at Hadco, puts it:

"With [accounts receivable] insurance, we don’t have to ask for cash up front or payment on delivery, which makes us much more competitive. This is the tool we needed to take more market share from our competitors."

Main Features of Accounts Receivable Insurance

Accounts receivable insurance offers a variety of coverage options tailored to different business needs and risk levels. These include:

- Whole Turnover Coverage: Protects receivables from all customers.

- Key Accounts Coverage: Focuses on the largest clients.

- Single Buyer Coverage: Insures receivables from a specific major buyer.

- Transactional Coverage: Covers individual transactions.

Insurers typically process credit limit requests quickly. For example, Allianz Trade handles 85% of approximately 20,000 daily credit limit requests within 48 hours. Indemnity levels usually range from 80% to 100% of the debt, while premiums are calculated as a small percentage of insured sales. Costs vary depending on factors like industry, customer creditworthiness, and overall risk. These flexible options allow businesses to align their insurance coverage with their specific risk profiles.

It’s important to note that accounts receivable insurance is distinct from "accounts receivable coverage" found in property insurance policies. While the former protects against customer non-payment, the latter covers losses from physical damage to records, such as those caused by a fire.

Which Businesses Benefit from Accounts Receivable Insurance?

This type of insurance is particularly valuable for businesses with high concentration risk, where a few large customers account for most of the revenue. If one of these customers defaults, it can severely disrupt cash flow. Coverage options like Key Accounts or Single Buyer are specifically designed to address this kind of vulnerability.

For businesses operating on tight profit margins, unpaid invoices can have an outsized impact. For instance, in a business with a 5% profit margin, losing $100,000 to bad debt would require $2 million in new sales to recover the lost profit. Cathy Jimenez, Credit Manager at Del Campo, highlights this balance:

"When you think about the benefits and what you could lose if a customer went bankrupt or just failed to pay, the cost of credit insurance balances out."

Small to mid-sized businesses also use accounts receivable insurance to improve their borrowing capacity. Banks often provide better rates and higher credit lines when receivables are insured, as they are seen as lower-risk collateral. This dual benefit of risk protection and enhanced access to working capital is emphasized by Mike Libasci, President of International Fleet Sales:

"Accounts receivable insurance has allowed us to take on customers and transactions we wouldn’t have felt comfortable taking on by ourselves."

How Trade Credit Insurance and Accounts Receivable Insurance Are Similar

Coverage Elements Both Types Share

Both trade credit insurance and accounts receivable insurance address critical commercial and political risks. On the commercial side, they cover issues like customer insolvency, bankruptcy, or extended non-payment. Politically, they protect against challenges such as trade embargoes, political unrest, or government actions that prevent payment.

When a covered event occurs, these policies generally reimburse between 75% and 95% of the unpaid invoice, cushioning the financial blow of bad debts.

Another shared benefit? Banks often view insured receivables as lower-risk assets, which can lead to better financing terms. As Jody Gilliam from Billtrust puts it:

"Financial institutions view insured receivables as lower-risk assets, which often translates to access to larger credit lines, improved financing terms, lower borrowing costs, and greater flexibility in working capital management."

This overlap in coverage not only mitigates financial losses but can also enhance a company’s financial position.

Business Benefits Both Types Provide

By addressing similar risks, both types of insurance allow businesses to confidently extend credit while maintaining steady cash flow. This is especially vital in a landscape where 80% of companies experience late payments, and 25% of bankruptcies stem from unpaid invoices. In the U.S., nearly one-third of small business owners report waiting over 30 days to get paid.

Another shared advantage is their ability to provide ongoing credit monitoring. These policies track customer creditworthiness and flag potential issues early, helping businesses avoid bad debt altogether.

The demand for these insurance products reflects their value. The global market was worth $9.39 billion in 2019 and is expected to grow to $18.14 billion by 2027, with an annual growth rate of 8.6%.

Cost-effectiveness is another strong point. With premiums typically under 1% of insured sales volume, these policies are far more economical than factoring, which often discounts receivables by 10% to 30%. This makes them a smart choice for managing risks and protecting profitability.

How Trade Credit Insurance and Accounts Receivable Insurance Differ

Although both trade credit insurance and accounts receivable insurance aim to protect a business from financial losses, they address entirely different risks and operate under distinct mechanisms. Trade credit insurance steps in when customers fail to pay due to reasons like insolvency, bankruptcy, or political disruptions such as currency restrictions or trade embargoes. On the other hand, accounts receivable insurance – typically part of a business property policy – covers losses stemming from the physical destruction of records that document what customers owe.

Policy Structure and Coverage Scope Differences

The main difference between these two types of insurance lies in what triggers the coverage. Trade credit insurance is activated by customer payment defaults, whether caused by financial insolvency, extended non-payment, or geopolitical events. This makes it particularly useful for businesses engaged in international trade, where both commercial and political risks are higher.

In contrast, accounts receivable insurance is designed to help businesses recover amounts owed when physical records of receivables are damaged or destroyed due to incidents like fires or natural disasters. As explained by the FCIS Team:

"The intent of accounts receivable coverage is not to collect on bad debt, but to assist an insured business after a covered physical loss to recover sums of money owed as a result of damage to accounts receivable records."

Here’s a side-by-side comparison of the two:

| Feature | Trade Credit Insurance | Accounts Receivable (Property Policy) |

|---|---|---|

| Primary Trigger | Customer insolvency, bankruptcy, or political events | Physical damage to accounting records |

| Coverage Focus | Broad protection against commercial and export risks | Restoration of financial data and records |

| Scope | Covers entire customer portfolios or specific high-value accounts | Focuses on all domestic receivables documented in records |

| International Coverage | Includes export and political risk protection | Typically limited to domestic operations |

With these structural differences in mind, the way premiums are calculated for each policy also reflects their distinct purposes.

How Pricing and Premiums Are Calculated

The methods for determining premiums for these policies align with their differing objectives. Trade credit insurance premiums are based on sales volume – calculated as a percentage of your yearly turnover or insured sales. Insurers evaluate factors like the number of customers covered, their financial health, the risk profile of your industry, and the payment terms you extend (e.g., net 30 or 60 days). Additionally, insurers assign credit limits to individual trade partners, and premiums adjust based on the perceived risk associated with those limits.

In contrast, accounts receivable insurance premiums are typically fixed and tied to the value of your records under your property policy. This difference underscores how trade credit insurance scales with business activity, while accounts receivable insurance is more static, focused on the replacement value of financial records.

Choosing Between Trade Credit Insurance and Accounts Receivable Insurance

Deciding between trade credit insurance and accounts receivable insurance comes down to understanding your specific risks. If your primary concern is non-payment from customers, trade credit insurance shields you from bad debt. On the other hand, if you’re worried about losing financial records due to physical disasters, accounts receivable insurance under a property policy might be the better fit. These policies serve different purposes, so identifying your biggest vulnerabilities is the first step. Let’s explore how these factors apply in real-world business situations.

What to Consider When Choosing

Start by assessing the type of risk you face. Trade credit insurance is designed to protect against bad debt – whether from customer insolvency, bankruptcy, or political events that prevent payment. Meanwhile, accounts receivable coverage under property policies only reimburses the expense of reconstructing financial records after events like fires or floods. For businesses focused on growth and maintaining steady cash flow, trade credit insurance often aligns better with their needs.

Think about your customer base and operational reach. If you sell internationally, trade credit insurance offers broad protection against both commercial and political risks. But if your operations are domestic and you have strong systems for keeping records, basic accounts receivable coverage may suffice for disaster recovery.

Your financing needs and growth plans also play a role. Trade credit insurance usually costs less than 1% of insured sales volume, but its benefits go beyond just risk protection. Lenders often provide better financing terms when your accounts receivable are insured. Plus, you can confidently extend more attractive credit terms to customers without jeopardizing your working capital.

CreditInsurance.com offers tools to help businesses evaluate these factors and choose the coverage that matches their risk profile, industry demands, and growth plans.

Example Scenarios for Each Type

Here are some examples to illustrate how businesses might choose between these coverages:

A machinery manufacturer exporting to Latin America would likely benefit from trade credit insurance. With the global trade credit insurance market expected to grow to $18.14 billion by 2027 (up from $9.39 billion in 2019), exporters are increasingly recognizing the importance of protecting against both commercial and political risks. This manufacturer could choose to insure its entire customer portfolio or focus on a single high-value client, depending on where the greatest risk lies.

On the other hand, a regional accounting firm serving domestic clients might find accounts receivable coverage under a property policy sufficient. If a fire destroys their office and billing records, this coverage would help cover the cost of reconstructing client account data. However, it wouldn’t protect against clients who refuse to pay or declare bankruptcy – that’s where trade credit insurance would be necessary.

A wholesale distributor competing for large retail contracts is another clear candidate for trade credit insurance. In industries where competitors already have credit insurance, having a policy becomes essential to offer the flexible payment terms that big retailers expect. During the economic challenges of 2020, the adoption of trade credit insurance surged as businesses sought stability in a disrupted market, making it a competitive tool as much as a risk management strategy.

Conclusion

Trade credit insurance safeguards businesses against customer non-payment caused by issues like insolvency, bankruptcy, or political disruptions. In contrast, accounts receivable insurance, typically part of property policies, focuses on recovering records after physical damage.

Beyond risk protection, credit insurance – costing less than 1% of insured sales – can improve lending terms and allow businesses to offer more competitive credit terms, helping attract larger buyers. With the global trade credit insurance market expected to grow to $18.14 billion by 2027 (up from $9.39 billion in 2019), many businesses now view these policies as tools for growth rather than just financial safety nets. Choosing the right coverage is essential to addressing your specific business risks.

If customer insolvency poses a threat to your cash flow, trade credit insurance may be the better choice. On the other hand, accounts receivable coverage is more appropriate for concerns about physical record loss. For most growing businesses – especially those operating internationally or competing for significant contracts – trade credit insurance often aligns better with their strategic objectives.

To help you navigate these options, CreditInsurance.com provides resources to assess your risk profile, compare coverage types, and select policies that balance protection with your growth goals. Whether you’re entering new markets or simply looking to secure your existing sales, understanding these insurance options is a critical step toward stronger financial risk management. By tailoring your coverage to your unique risks, you can build a more resilient and forward-thinking financial strategy.

FAQs

Can I carry both coverages at the same time?

Yes, you can hold both trade credit insurance and accounts receivable insurance at the same time. These two types of coverage often complement each other, offering enhanced protection against risks such as non-payment or customer insolvency. Together, they can also help businesses confidently pursue growth opportunities while minimizing financial uncertainties.

What isn’t covered by trade credit insurance?

Trade credit insurance is designed to safeguard businesses against non-payment risks like insolvency, bankruptcy, or political issues. However, it does not extend to losses stemming from intentional fraud, contractual disputes, or insolvencies linked to illegal activities. Fraudulent acts and certain legal disagreements fall outside the scope of this coverage.

How do credit limits work for each customer?

Credit limits play an important role in both trade credit insurance and accounts receivable insurance, though they are handled differently in each case. With trade credit insurance, the insurer determines these limits after evaluating the creditworthiness of the customer. On the other hand, accounts receivable insurance allows businesses to set their own limits, often with the help of tools provided by the insurer. In both scenarios, credit limits are essential for managing risk, safeguarding cash flow, and preventing excessive credit exposure to customers who may pose a higher risk.