Blockchain technology is transforming supply chain finance by improving transparency, automating processes, and reducing risks. Here’s what you need to know:

- What It Does: Blockchain creates a secure, shared ledger for buyers, suppliers, banks, and insurers to access real-time, tamper-proof transaction data.

- Key Benefits: It eliminates manual errors, reduces disputes, and speeds up processes like payments and credit evaluations.

- Real-World Examples: Walmart Canada reduced invoice disputes from 70% to less than 1%, saving $30 million. Komgo cut letter-of-credit issuance time by 99%.

- Smart Contracts: Automate payments and compliance checks, saving time and cutting costs.

- Credit Risk Management: Blockchain ensures data integrity, enabling precise underwriting, fraud prevention, and faster claims processing.

The article explores case studies like Walmart, Chained Finance, and blockchain consortia, showcasing how businesses are using blockchain to streamline operations, reduce credit risks, and improve financing access. Whether you’re looking to resolve invoice disputes or secure financing, blockchain offers practical solutions for modern supply chain challenges.

Blockchain Impact on Supply Chain Finance: Key Statistics and Results

Key Features of Blockchain for Credit Risk Management

Single Source of Truth and Transparency

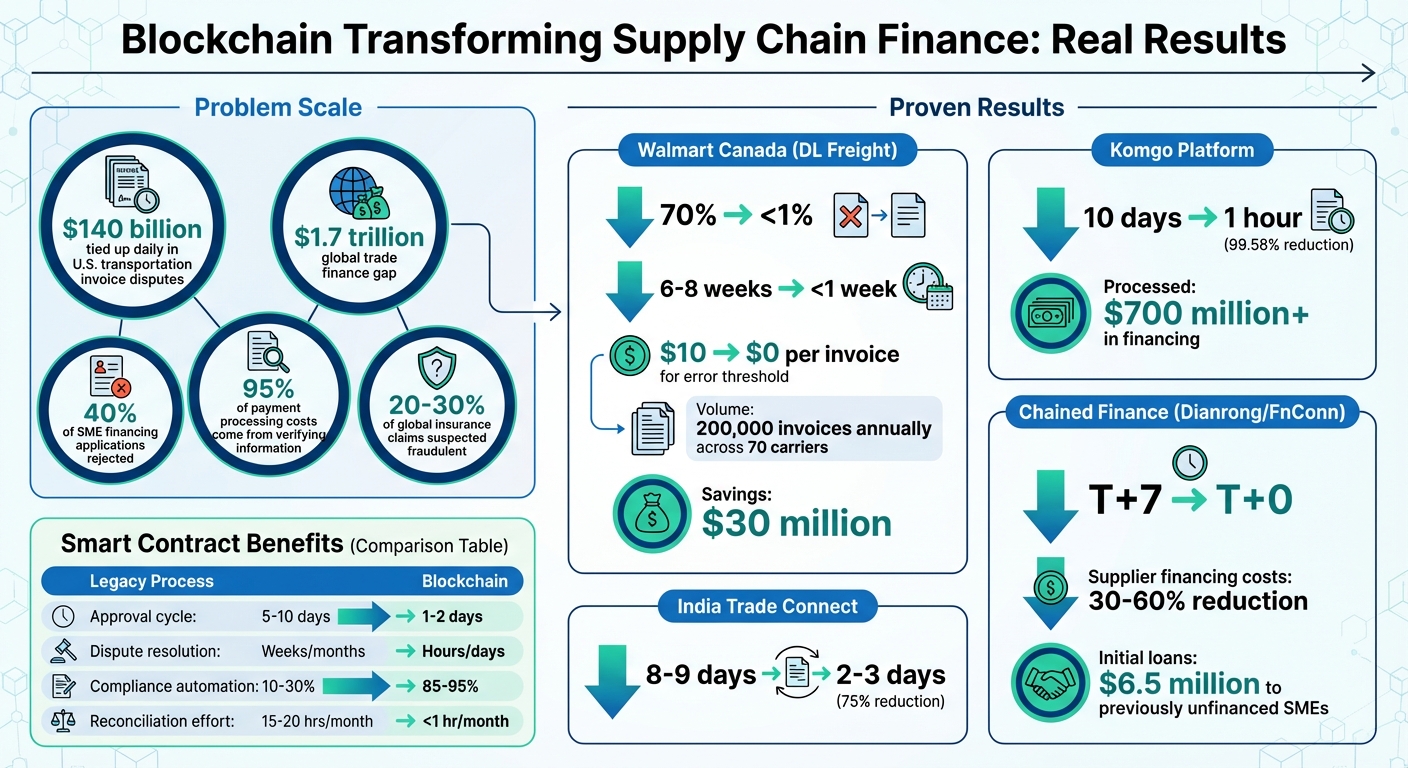

Blockchain technology addresses data inconsistencies by creating a shared ledger that stores critical documents like invoices, contracts, and bills of lading. This ledger ensures that all authorized parties access the same unchangeable record, eliminating the need for separate systems. For example, in the U.S. transportation industry, around $140 billion is tied up daily in invoice disputes due to mismatched data.

Using a consensus mechanism, blockchain prevents any single party from altering, deleting, or adding records without agreement from others in the network. This allows for real-time tracking of orders and shipments, cutting down on manual reconciliation efforts. Walmart Canada’s adoption of the DL Freight system with DLT Labs is a prime example. By tracking over 220 data points per load across 70 carriers, they managed to process 200,000 invoices annually, reducing payment approval times from six to eight weeks to less than a week by 2022.

Francis Lalonde, Vice President of Transportation at Walmart Canada, highlighted the impact by saying, "Something unusual has to occur to have a dispute now. There are small items to resolve, but as we all have the same information, there is simply no need for disputes anymore".

Platforms like Hyperledger Fabric further enhance this system by enabling private transactions through "channels" while maintaining a unified network structure. This design protects sensitive commercial information while ensuring transparency for credit risk assessments. Inefficient data management in transportation accounts for roughly 20% of administrative costs. By centralizing and verifying data, blockchain minimizes credit risks and streamlines operations.

Smart Contracts for Automation

Blockchain takes transparency a step further by automating financial processes through smart contracts. These contracts trigger payments and settlements automatically when specific conditions are met, eliminating the need for manual "match and compare" processes, which are a common cause of disputes in traditional systems.

For instance, Walmart Canada saw its error threshold improve from $10 per invoice to $0 after implementing blockchain automation. When paired with IoT sensors that monitor factors like temperature and cargo location, smart contracts can validate compliance and trigger payments in real time.

The benefits of smart contracts are clear:

| Capability | Legacy Manual Process | Smart Contract-Enabled Workflow |

|---|---|---|

| Approval Cycle Time | 5–10 business days | 1–2 business days |

| Dispute Resolution | Weeks to months | Hours to days |

| Compliance Automation | 10–30% automated | 85–95% automated |

| Reconciliation Effort | 15–20 hours per month | < 1 hour per month |

Take Contura Energy, a coal supplier based in Tennessee, as an example. They developed a Letter of Credit application on Amazon Managed Blockchain. This system uses smart contracts and Amazon Textract to detect discrepancies in documents, sending alerts in real time if errors occur. By reducing validation time and minimizing human error, these automated systems significantly lower credit risk.

Better Trade Data for Credit Insurance

Beyond automation, blockchain ensures the integrity of trade data, crucial for refining risk assessments. Every action – whether creating, approving, or amending trade documents – is cryptographically signed and timestamped. This creates a reliable audit trail that simplifies regulatory compliance and claims validation. With verified transaction histories, underwriting becomes more precise, relying on actual performance data rather than self-reported figures.

Blockchain also enables real-time risk evaluation through tokenized trade assets and IoT data. Unlike static, historical data, insurers can assess risks dynamically as shipments progress. Cryptographic verification of documents like Certificates of Origin and Bills of Lading makes forgery and double financing nearly impossible, directly reducing risk for underwriters. Notably, 95% of payment processing costs in trade finance stem from verifying information – such as who, what, when, and where – rather than the actual transfer of funds.

In January 2019, we.trade Innovation DAC – a collaboration between 12 banks, IBM, and credit bureau CRIF – launched its Hyperledger Fabric platform. This platform uses smart contracts and Bank Payment Undertakings to shift counterparty risk to banks, making cross-border trade safer for small and medium-sized businesses.

Mark Cudden, Chief Technology Officer at we.trade, remarked, "At we.trade, we are innovating the traditional trade finance model and we believe that the industry can be made much simpler, efficient and secure, enabling companies of all sizes to trade across borders".

This infrastructure equips credit insurers with reliable data to set accurate policy limits and expedite claims processing. By working from a single verified dataset, insurers can significantly reduce their credit risk exposure. For more information on how blockchain is transforming credit risk assessments and credit insurance, visit CreditInsurance.com.

sbb-itb-b840488

Case Studies: Blockchain Applications in Supply Chain Finance

Case Study: Chained Finance by Dianrong and FnConn

In March 2017, Dianrong and FnConn – a subsidiary of Foxconn – introduced a pilot program in China to address financing challenges for suppliers buried deep within supply chains. Through the Chained Finance platform, they facilitated $6.5 million (RMB 45 million) in loans for small and medium enterprises (SMEs) that previously had no access to capital. Before this initiative, only about 15% of suppliers in China could secure financing.

The platform works by converting the creditworthiness of a core enterprise like Foxconn into digital assets, which can then flow across multiple tiers of the supply chain. This setup allows smaller suppliers – often unable to secure affordable loans – to benefit from the strong credit profile of the lead company. Using a consortium blockchain initially based on Hyperledger Besu and later integrated with R3 Corda, the system creates an unalterable record of all payments and transactions, ensuring transparency and traceability.

The results were striking: financing time dropped from T+7 to T+0, and end-tier suppliers saw financing costs reduced by 30% to 60%. Financial institutions gained access to real trade data, which helped reduce information gaps and lowered risks of fraud and defaults.

"By using the Chained Finance platform, every payment, every supply chain transaction, can be more transparent, manageable and easily authenticated", said Jack Lee, Executive Director and CEO of FnConn.

This platform is particularly effective in industries with complex, multi-layered supply chains – like electronics, automotive, and garment manufacturing – where visibility into deep-tier suppliers has traditionally been elusive. The initiative highlights how blockchain can help lower credit risk, a critical challenge in supply chain finance.

Skuchain and Hyperchain offer alternative models for tackling similar problems.

Case Study: Skuchain and Hyperchain

While Chained Finance focuses on receivables financing, Skuchain and Hyperchain employ distinct approaches to achieve similar goals. Skuchain uses an inventory-backed financing model, where physical goods are tokenized into digital multi-tokens called Popcodes (based on the ERC-1155 standard). These tokens represent inventory quotas or fractional ownership, enabling suppliers to trade tokenized assets in a specialized marketplace to unlock cash flow. It also uses Distributed Ledger Payment Commitments (DLPC) to secure trade instruments.

Hyperchain, on the other hand, mirrors Chained Finance by concentrating on receivables financing. Both platforms aim to expand credit access for suppliers who lack direct relationships with anchor buyers, but their methods differ. Skuchain’s inventory-based approach suits industries with high-value inventory, while Hyperchain and Chained Finance thrive in transaction-heavy sectors where receivables are the primary assets.

| Feature | Skuchain | Hyperchain/Chained Finance |

|---|---|---|

| Primary Collateral | Inventory (tokenized goods) | Accounts receivable (digital credit transfer) |

| Financing Model | Asset-backed marketplace trading | Credit transfer from core enterprise |

| Best Fit Industries | Manufacturing; commodities with high inventory | Electronics, automotive, garment (transaction-heavy) |

| Risk Mitigation | Secure, verifiable trade instruments using DLPC | Immutable transaction records and credit verification |

These varied strategies showcase how blockchain can reduce credit risk across different types of assets and financing structures.

Case Study: Blockchain Consortia for Trade Finance

Beyond individual platforms, blockchain consortia are streamlining trade finance on a larger scale. These industry collaborations aim to mitigate credit and operational risks in cross-border trade. Examples include Contour (built on R3 Corda), which focuses on letters of credit; we.trade (using Hyperledger Fabric), which targets open-account transactions for SMEs; Marco Polo, which specializes in receivables financing; and India Trade Connect, which facilitates domestic trade finance across multiple banks.

In September 2020, HSBC Vietnam and Vietcombank completed Vietnam’s first domestic letter-of-credit transaction on Contour in just 27 minutes, compared to the usual 3–5 days. The transaction involved Kirby South East Asia Co., Ltd as the buyer and Ton Dong A Corporation as the seller.

"This transaction marks another milestone for Vietnam’s trade capabilities… undertaking domestic Letter-of-Credit transactions faster and more safely on Contour’s Blockchain platform", said Tim Evans, CEO of HSBC Vietnam.

India Trade Connect achieved a 75% reduction in cycle time for inland letters of credit, cutting the process from 8–9 days to 2–3 days during its pilot phase (March 2017 to March 2018). The platform has since moved into full production, using unique invoice identifiers to prevent duplicate financing.

During a seven-week trial in December 2019, over 70 organizations – including BMW, ABN AMRO, and Commerzbank – completed more than 700 funding requests, with users requiring an average of just one day of training. Participants highlighted the potential of distributed ledger technology to improve efficiency and cut costs for both banks and businesses.

| Consortium | Technology Platform | Focus | Key Risk Management Feature |

|---|---|---|---|

| Contour | R3 Corda | Letters of Credit | Real-time data sharing; 27-minute LC processing |

| we.trade | Hyperledger Fabric | Open Account (SMEs) | Bank Payment Undertaking transfers risk to banks |

| Marco Polo | R3 Corda | Receivables Finance | Automated receivables discounting; high connectivity |

| India Trade Connect | Infosys Finacle | Domestic Trade Finance | Unique invoice IDs prevent duplicate financing |

These consortia build upon the innovations of platforms like Chained Finance, offering standardized and secure solutions for cross-border trade. They further demonstrate blockchain’s growing role in improving credit risk management across global supply chains.

Cross-Case Insights: Blockchain and Credit Insurance

Improved Risk Assessment and Underwriting

Blockchain is reshaping how credit risk is evaluated by replacing outdated credit scores with real-time transaction data. Traditional underwriting methods often rely on financial statements and credit reports that are months old. In contrast, blockchain platforms offer a continuously updated record of payment behaviors, shipment performance, and trade history. This gives insurers a more dynamic and accurate view of a buyer’s creditworthiness.

Take Walmart Canada’s DL Freight as an example – it reduced disputes by over 98%. This single source of truth ensures all parties – insurers, lenders, and businesses – access the same verified data. With this transparency, insurers can adjust coverage limits or financing terms based on current behavior rather than relying on outdated information. It also helps cut down fraud, which is a significant issue, as around 20–30% of global insurance claims are suspected to be fraudulent.

For U.S. businesses working with credit insurance providers, blockchain-derived data allows for more precise underwriting. Insurers can monitor payment patterns in real time and make adjustments dynamically, avoiding the delays tied to annual reviews. This proactive approach minimizes risks like moral hazard and adverse selection, which are common in traditional insurance models.

This shift toward real-time insights also lays the groundwork for quicker claims processing, which we’ll explore next.

Faster Claims Validation

Blockchain technology speeds up claims processing by offering instant, tamper-proof records of shipments and invoices. Traditional claims validation often involves gathering documents from multiple sources, verifying their authenticity, and resolving discrepancies – a process that can drag on for weeks or even months.

Platforms like komgo showcase how blockchain can streamline this process. Backed by major banks like Citi and BNP Paribas, komgo reduced the time needed to issue letters of credit by an astounding 99.58% – from 10 days to just one hour. By October 2019, it had processed over $700 million in financing. This efficiency stems from digitizing trade documents and storing them on a shared ledger, giving insurers instant access to verified information.

Another example is the Irish dairy cooperative Ornua, which used the Wave blockchain platform to complete a letter of credit transaction with Seychelles Trading Company in less than four hours – down from the typical 7 to 10 days.

Jesse McWaters, Project Lead at the World Economic Forum, noted: "The process – from issuing to approval of the letter of credit, which usually takes between seven and 10 days – could be reduced to less than four hours".

For credit insurance claims, this means insurers can verify that goods were shipped, received, and invoiced correctly without manually reviewing documents. Smart contracts further enhance this process by automatically approving claims once specific conditions – like confirmed delivery or verified non-payment – are met. This automation also trims administrative costs, which can account for up to 20% of transportation fees in industries like freight.

Insured Receivable-Backed Financing

Blockchain offers a powerful solution for businesses: using insured receivables as collateral for financing, backed by real-time verification of trade data. This addresses a critical issue for U.S. businesses – the $1.7 trillion global trade finance gap, where 40% of small and medium-sized enterprise (SME) applications are rejected due to insufficient verifiable information.

When receivables are insured and recorded on a blockchain, lenders benefit from two layers of security. Credit insurance covers the risk of non-payment, while blockchain ensures the invoice’s legitimacy and prevents duplication. This combination makes financing more accessible to businesses that may not have qualified otherwise.

For instance, Figure’s March 2020 securitization (FLOC 2020-1) on the Provenance Blockchain demonstrated the financial benefits. By managing loans entirely on blockchain, Figure saved an average of 117 basis points per loan, translating to potential industry-wide savings of $163 billion in the securitization market.

The platform enabled "real-time, riskless trade settlement" by replacing manual verification with smart contracts.

The Global Shipping Business Network (GSBN) took this concept further in September 2022 with a pilot project involving Bank of China (Hong Kong), Hapag-Lloyd, and A & W Food Service. Using a "consent collection" application, the transaction was completed in under 20 minutes. This approach allowed the bank to source data directly from shipping lines for verification.

Edmund To, Chief Technology Officer at GSBN, explained: "Consent collection offers a new level of protection by allowing banks to get trusted data directly from the source. This facilitates approval processes and makes trade finance more accessible to SMEs".

These examples highlight blockchain’s ability to reduce risk and unlock working capital by leveraging verified trade data. For U.S. businesses, the key lies in ensuring that blockchain-derived trade data aligns with the documentation standards of both credit insurers and lenders. Platforms like CreditInsurance.com can help businesses structure insured receivables to maximize financing options while maintaining risk protection. These insights are critical for companies considering blockchain solutions.

Practical Considerations for U.S. Businesses Adopting Blockchain

Integration with Existing Systems

You don’t need to completely overhaul your current systems to integrate blockchain. Many businesses find success using API-driven middleware to connect their existing ERP and treasury systems with blockchain networks.

Take Walmart Canada as an example. When they launched DL Freight in January 2019, they didn’t replace their transportation management system. Instead, they introduced an "Integration Hub" – a centralized gateway linking their ERP, carrier systems, and the Hyperledger Fabric blockchain. By March 2021, this system was managing over 500,000 shipments annually across 70 carriers, cutting invoice disputes from 70% to less than 1%.

"Hyperledger Fabric is the only platform in the market which is mature enough to run a production environment and meet the security standards of major enterprises."

- Neeraj Srivastava, Co-founder and CTO, DLT Labs

For documentation-heavy processes, such as letters of credit, a hybrid storage approach can be effective. For instance, Contura Energy, a coal supplier based in Tennessee, stored large documents in Amazon S3 using Object Lock for immutability while recording cryptographically signed hashes on the blockchain.

Starting small is key. Focus on one high-friction workflow – like freight invoice reconciliation or LC processing – as your initial pilot. Once successful, you can expand blockchain integration to other areas of your supply chain. This approach not only simplifies operations but also supports better supply chain finance and credit risk management.

Legal and Risk Management Factors

Once you’ve integrated blockchain into your systems, navigating legal and regulatory challenges becomes crucial. A primary concern is ensuring digital documents are legally binding. Traditional physical documents, such as bills of lading or invoices, often carry more weight because not all regulators, customs officials, and financial institutions recognize digital versions.

"A blockchain-backed digital document only works if regulators, customs, financial institutions and all counterparties agree to recognize it."

- James Wester, Research Director for Digital Assets and Crypto, Javelin Strategy

In July 2025, U.S. Bank completed its first fully digital trade finance transaction using the WaveBL platform, in partnership with MSC Mediterranean Shipping Company and ICICI Bank. This shift reduced document transmission times from days to mere minutes. Daniel Son, Head of Working Capital Finance at U.S. Bank, highlighted the cost efficiency:

"Digital costs a fraction of courier costs, especially when there’s a mistake that you have to correct and then resend the documents back and forth"

When sharing sensitive trade data on a blockchain, access control is critical. Permissioned blockchains like Hyperledger Fabric limit access to authorized participants, ensuring compliance and security. Walmart Canada, for instance, consulted legal experts to ensure their blockchain solution adhered to all relevant regulations before launch.

For smart contracts to work effectively, all parties involved – suppliers, carriers, banks, and insurers – must agree on the business rules in advance. This includes details like fuel costs, tax rates, and payment terms. Clear agreements help avoid disputes when transactions are automated.

U.S. businesses must also navigate federal regulations from agencies like the SEC, FinCEN, and IRS. Partnering with legal counsel experienced in blockchain and regulatory compliance is essential before deploying any production system.

Aligning Blockchain with Credit Insurance Programs

Once legal safeguards are in place, blockchain can be a powerful tool for enhancing credit insurance programs. Its real-time, verified data allows insurers to assess risks more accurately. Instead of relying on outdated financial statements, insurers can access live records of payment behaviors, shipment performance, and invoice histories directly from the blockchain ledger.

To make the most of this, businesses should focus on permissioned blockchains that protect sensitive data while enabling necessary sharing with insurers and lenders. Smart contracts can also automate risk scoring and trigger claim payouts based on agreed conditions.

Integrating external data sources is another important step. Blockchain oracles can securely feed information from IoT sensors, financial reports, and other systems into smart contracts, enabling real-time underwriting. This creates a reliable, single source of truth that minimizes the information gaps often found in credit insurance relationships.

For companies using insured receivables as collateral, blockchain verification adds an extra layer of security. Lenders can confirm invoice authenticity, while credit insurance reduces the risk of non-payment.

If your business struggles with disputes or manual reconciliation, consider starting with those workflows. In the U.S. transportation sector alone, $140 billion is tied up daily in invoice disputes. Blockchain-derived data can help insurers adjust coverage dynamically, rather than waiting for annual reviews. Platforms like CreditInsurance.com can assist in structuring insured receivables to optimize both risk protection and financing options, ensuring your blockchain data meets insurer documentation standards. These steps can help close financing gaps and improve access to supply chain finance.

Why Blockchain is FINALLY Changing Trade Finance

Conclusion

Blockchain is reshaping supply chain finance by introducing a unified, reliable ledger that drives efficiency and trust. Real-world examples, like Walmart Canada reducing disputes significantly and komgo cutting letter-of-credit issuance to just one hour, show the tangible impact of this technology. These advancements translate into financial gains: smart contracts streamline reconciliation, cryptographic hashing secures documents against tampering, and real-time data feeds improve risk assessment – unlocking working capital and curbing fraud.

Consider this: in the U.S. alone, $140 billion is tied up daily in transportation invoice disputes. Blockchain offers a practical solution to improve cash flow and reduce these delays. For companies struggling with payment bottlenecks or frequent disputes, the benefits extend beyond finances – they also strengthen trust and collaboration with suppliers.

Beyond operational efficiencies, blockchain is transforming credit insurance programs. Insurers gain access to verified, real-time data for sharper risk assessments and faster claims processing. Instead of relying on outdated financial reports or cumbersome paperwork, insurers can analyze live records of payment trends, shipment reliability, and invoice histories. This paves the way for dynamic coverage adjustments and financing options based on insured receivables – innovations that traditional systems simply can’t support.

For U.S. businesses, the best starting point is tackling high-friction workflows – those areas where disputes and manual tasks drain time and resources. Integrating blockchain doesn’t mean scrapping existing systems; middleware and APIs can seamlessly link current ERP platforms to blockchain networks. As emphasized throughout this discussion, CreditInsurance.com offers tools and guidance to help businesses integrate blockchain solutions with credit insurance programs. This ensures your trade data aligns with insurer requirements while enhancing both risk protection and financing opportunities.

Blockchain has moved from experimental projects to managing billions in real-world transactions. Whether it’s freight invoicing, trade finance, or supplier onboarding, this technology lays the groundwork for secure, efficient, and transparent supply chain finance operations.

FAQs

What supply chain finance process should I pilot with blockchain first?

Recent examples highlight the benefits of starting with the trade finance process, focusing on tokenized settlements and digitized transaction management. Blockchain-powered trade finance platforms simplify cross-border transactions while cutting down on fraud risks. A notable example is Walmart Canada, which uses blockchain for freight invoicing and payment reconciliation. This approach addresses inefficiencies and reduces disputes. These applications tap into blockchain’s ability to enhance digitization, provide transparency, and automate processes, creating a solid base for tackling more advanced use cases.

How do permissioned blockchains keep trade data private but shareable?

Permissioned blockchains offer a secure way to protect trade data privacy while allowing selective sharing through controlled access. With this setup, only authorized participants can view specific pieces of information, ensuring that sensitive data remains confidential. Features like encryption and role-based permissions add an extra layer of protection, enabling stakeholders to share only the necessary details without revealing the entire dataset. This approach helps maintain transparency and trust in areas like supply chain finance and credit risk management, all while keeping proprietary or contractual information secure.

How can blockchain-verified receivables improve credit insurance and financing?

Blockchain-verified receivables bring a new level of clarity, security, and efficiency to credit insurance and financing. By enabling real-time verification, they significantly lower the risk of fraud, while the unchangeable nature of blockchain records builds confidence and supports more precise credit risk evaluations. Additionally, smart contracts simplify approval processes and reduce administrative expenses, helping insurers and financiers create more accurate policies and streamline supply chain financing. This approach fosters a dependable and efficient system for businesses, credit insurers, and financiers to operate within.