Underwriter-broker collaboration is the backbone of effective trade credit insurance. This partnership ensures businesses get tailored coverage while navigating complex terms and risks. Brokers act as client advocates, finding the best policies and simplifying the process. Underwriters focus on evaluating financial risks and setting credit limits. Together, they help businesses protect receivables, increase financing options, and reduce non-payment risks.

Key Takeaways:

- Brokers negotiate with insurers, explain policy terms, and help avoid claim denials.

- Underwriters assess risk, set credit limits, and ensure policies align with financial realities.

- This collaboration supports growth by safeguarding receivables and improving access to financing.

Benefits:

- Protect against non-payment risks.

- Boost bank financing options with insured receivables.

- Simplify policy management and claims processes.

The article dives into the roles, responsibilities, and stages of this partnership, offering insights on how businesses can leverage it for better risk management and tailored solutions.

Roles and Responsibilities

Insurance Broker vs Underwriter: Roles and Responsibilities Comparison

What Underwriters Do

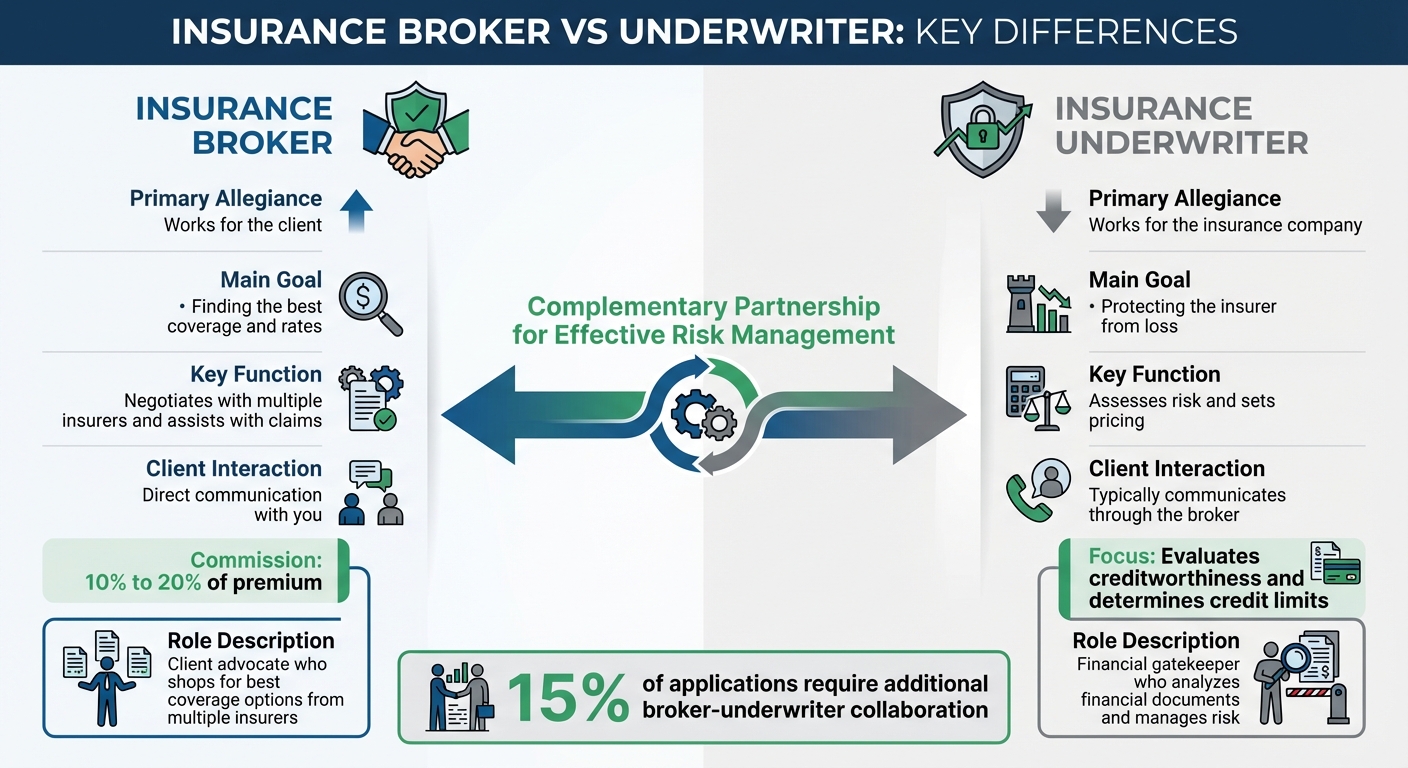

Underwriters serve as the financial gatekeepers in credit insurance, carefully evaluating the creditworthiness of your customers before offering coverage. Their job is to analyze critical financial documents like balance sheets, cash flow statements, payment histories, and credit ratings. Based on this analysis, they determine credit limits – the maximum coverage amount for each buyer – balancing your business growth with responsible risk management. As circumstances shift, underwriters adjust these limits to reflect the latest conditions.

"Underwriters are the backbone of the credit insurance process. Their primary role is to evaluate the creditworthiness of a business’s customers and determine the level of risk associated with insuring those receivables."

– Christian Bürger, Senior Editor, Atradius

Underwriters also structure the terms of your policy, set premium rates (usually a percentage of your sales value), and define deductibles. If a claim is filed, they verify its validity and calculate the payout based on compliance with the policy.

What Brokers Do

Brokers work on your behalf, not for the insurance company. Their role is to advocate for your interests by understanding your business operations, risk profile, and receivables management needs. They use this information to shop for the best coverage options from multiple insurers. Brokers help identify any gaps in coverage and negotiate terms that align with your goals.

But brokers do more than just find quotes. They present your business in a way that helps underwriters see the full picture beyond the numbers. For instance, in June 2025, a homeowner worked with a broker who highlighted a recent roof replacement in their application to three insurers. The additional context allowed the underwriter to apply a risk credit, reducing the final premium to $1,656 – much lower than the initial quotes, which were as high as $2,400. This level of detail fosters collaboration and sets the foundation for effective risk management. Brokers typically earn a commission of 10% to 20%, which is included in your premium cost.

How These Roles Work Together

Underwriters and brokers bring complementary skills to the table, creating a well-rounded approach to managing credit risk. Brokers provide operational insights, claims history, and business context in a format that underwriters can efficiently review. This partnership is especially important since underwriters often reach out to brokers for clarification – approximately 15% of applications require additional input.

| Feature | Insurance Broker | Insurance Underwriter |

|---|---|---|

| Primary Allegiance | Works for the client | Works for the insurance company |

| Main Goal | Finding the best coverage and rates | Protecting the insurer from loss |

| Key Function | Negotiates with multiple insurers and assists with claims | Assesses risk and sets pricing |

| Client Interaction | Direct communication with you | Typically communicates through the broker |

When challenges arise – like a carrier recommending costly safety upgrades – brokers step in to negotiate practical solutions that work within your budget while satisfying the underwriter’s risk criteria. This collaboration not only improves the accuracy of risk assessments but also ensures that policies remain financially viable for insurers and practical for your business. It’s a partnership that streamlines the process and enhances client support.

sbb-itb-b840488

Key Stages of the Collaboration Process

Working from the established roles of underwriters and brokers, the collaboration progresses through several stages designed to maintain effective risk management.

Application and Quote Submission

The process begins with your broker submitting essential documentation to underwriters. This typically includes audited financial statements, a 12-month accounts receivable aging report, loss history, and a detailed description of your operations. The thoroughness of this submission is crucial – submissions that are incomplete or lack clarity are often rejected outright.

"Submission quality is critical. Each time a broker provides a submission to an underwriter, he or she hopes to receive a timely acknowledgment; however, this response is predicated on the quality of the information provided." – Keith Boyer, Managing Partner, KMRD Partners

To streamline the process, many brokers now use digital platforms to upload documents and monitor the application’s progress in real time. Skilled brokers also consult with underwriters early on to confirm whether the opportunity aligns with their criteria. Once underwriters receive the submission, they assess it based on exposure data and risk management strategies. If the application falls short, underwriters often provide constructive feedback to help brokers refine future submissions.

Trade credit insurance premiums typically range between 0.15% and 0.80% of the insured turnover, although high-risk industries may see rates climb to 1.2% or more. Coverage generally provides indemnity levels of 80% to 95% of insured losses.

Credit Risk Assessment and Policy Customization

After receiving the initial submission, underwriters conduct a detailed analysis. They evaluate factors like liquidity ratios, debt levels, sector-specific risks, and country-level economic conditions to determine creditworthiness. During this phase, your broker serves as an advocate, explaining the unique aspects of your business or negotiating for higher credit limits.

As your business grows or changes, your broker communicates updates to underwriters, who adjust credit limits and policy terms accordingly. Increasingly, underwriters are using artificial intelligence and machine learning to improve accuracy, particularly for portfolios with large numbers of buyers. Once quotes from multiple carriers are gathered, your broker simplifies the complex policy details, ensuring you fully understand the coverage terms and any requirements for maintaining eligibility for future claims.

"Our service doesn’t end with a policy sale. We continuously update servicing plans based on our clients’ sales, revenue changes, and evolving credit requirements." – Kirk Elken, Co-founder, Securitas Global Risk Solutions

With a customized policy in place, the focus shifts to claims handling and preparing for renewal.

Claims Handling and Policy Renewal

The collaboration doesn’t stop after the policy is customized. Claims handling and policy renewal are key parts of the ongoing relationship. During renewal, underwriters reassess the risk, handle tasks like cancellations or reinstatements, and ensure compliance with regulations while determining final pricing. This stage emphasizes the importance of continued communication and adaptability.

Your broker remains actively involved throughout the policy’s lifecycle. They work with underwriting assistants to ensure all policy-related details are clearly communicated. In specialized industries, such as Life Sciences, underwriters collaborate with claims professionals to provide expert guidance during claims processing. A carrier’s ability to resolve claims efficiently and fairly is critical – brokers rely on this reliability to maintain client trust. For a smooth renewal process, brokers must submit updated exposure data, loss records, and any new risk management strategies.

"Keeping open lines of communication with the people I deal with daily makes for a successful day." – Denise Howell, Senior Underwriting Assistant, Admiral Insurance Group

Best Practices for Working Together

The dynamic between underwriters and brokers is shifting. What once were purely transactional exchanges are now evolving into strategic partnerships built on trust and openness. Both sides bring unique strengths to the table – brokers often act as the proactive "offense", while underwriters take on the role of the cautious "defense". Recognizing this balance is key to fostering the trust needed for long-term collaboration. Here are some ways to make these partnerships even more effective.

Maintaining Clear Communication

Starting with strong communication can save a lot of headaches later. A simple phone call early in the process to discuss risk details or align on expectations can cut down on endless email chains and avoid confusion. When underwriters decline a risk, explaining the reasoning and suggesting alternatives can go a long way in maintaining trust. This is important, especially when only 45% of brokers feel there’s a fair balance between their interests and those of carriers.

"A quick phone call early on to talk through the background of a risk or align expectations can prevent lengthy email chains and misunderstandings further down the line." – Abbie Mansfield, Underwriter, Arch UK

High-quality submissions also help streamline the process. With E&S underwriters reviewing 16–20 submissions daily, a brief cover letter or summary email that highlights key concerns can save valuable time. For more complex cases, following up with a phone call instead of relying solely on email adds clarity and builds stronger relationships. Quick responses – ideally within one business day – help maintain momentum and trust.

Using Technology and Data Tools

Modern tools like broker portals and underwriting workbenches are making the quote-to-bind process more transparent. These platforms eliminate the frustrating "black hole" where brokers submit applications and then hear nothing back. AI-powered systems now extract and organize data from PDFs, Excel files, and emails, cutting manual entry time by over 40%.

Real-time appetite modeling is another game-changer. By using AI to evaluate the fit and likelihood of success for submissions, brokers can get faster decisions – sometimes an immediate yes or no. Unfortunately, many insurance CIOs still allocate up to 90% of IT resources to manual tasks, leaving little room for innovation. Custom submission fields in broker portals can help ensure underwriters receive all the necessary information upfront, reducing back-and-forth. For the best results, choose tools designed specifically for the insurance industry – ones that can handle ACORD forms and P&C-specific terminology, rather than generic solutions. These advancements not only improve efficiency but also strengthen the client-focused approach discussed next.

Putting Client Needs First

Strong partnerships thrive when client needs take center stage. Joint client meetings, for instance, give underwriters valuable insights beyond the usual proposals. Brokers can improve outcomes by submitting risks with a higher likelihood of success. Meanwhile, carriers can add value by offering services like loss control, risk engineering, or guidance on complex issues, positioning themselves as trusted advisors rather than just price-focused providers.

"The core of underwriting and broking will always be people: using judgment, empathy, and genuine understanding to make informed decisions." – Abbie Mansfield, Underwriter, Arch UK

Empathy is crucial. Underwriters should understand the challenges brokers face in a hard market, while brokers need to recognize the stricter criteria carriers require to maintain financial stability and ensure claims can be paid. Regular meetings – whether monthly or quarterly – to review new business and share feedback help both sides stay aligned with market trends. This kind of collaboration not only strengthens partnerships but also leads to better outcomes for clients.

Benefits of Strong Partnerships

Strong partnerships between underwriters and brokers can lead to measurable improvements across several key areas. By fostering genuine collaboration, businesses can achieve better risk management, tailored policies, and cost efficiencies.

Better Risk Management

Collaboration transforms how risks are identified and managed. When brokers share detailed operational data and claims histories, and underwriters contribute insights from their intelligence networks, both parties can assess risks with greater precision. This exchange of information leads to more accurate pricing and improved profitability.

Working together also helps close coverage gaps that might otherwise go unnoticed. Brokers and underwriters can anticipate and address emerging risks before they escalate. For instance, Allianz Trade monitors over 85 million companies daily using its proprietary intelligence network, enabling its partners to avoid bad debt and make better trade decisions.

"As a broker we are incredibly lucky to have daily interactions with insureds and insurers to understand their pain points, but we also need to think more broadly about the risks they are not yet thinking about." – Lucy Stanbrough, Head of Emerging Risks, WTW

This level of collaboration not only improves risk management but also opens the door to more personalized coverage options.

Customized Policies for Growth

Partnerships make it possible to craft policies tailored to a business’s specific needs, moving away from one-size-fits-all solutions. Underwriters and brokers working closely together can design coverage that aligns with operational goals, whether a business is exploring new markets, bidding for major contracts, or tackling ambitious projects.

This consultative approach repositions underwriters as strategic advisors rather than mere gatekeepers. Instead of simply processing applications, they work alongside brokers to address unique challenges and create solutions that directly address client pain points. This is especially critical in today’s market, where only 8% of property and casualty insurers use automated, data-driven underwriting recommendations. For complex risks, human judgment and understanding remain irreplaceable.

Efficiency and Cost Savings

Strong partnerships also reduce administrative burdens. Currently, underwriters in commercial and personal lines spend 41%-43% of their time on tasks like data entry and record keeping, leaving only 32%-33% for actual risk assessment and premium calculation. High-quality submissions from brokers allow underwriters to focus on viable opportunities instead of sifting through incomplete proposals.

"The underwriter, who will typically be long on pending proposals and short on time, will appreciate the consideration shown by a broker who does not clutter his in basket with born losers." – Keith Boyer, Managing Partner, KMRD Partners

Conclusion

The relationship between underwriters and brokers has grown into something far more dynamic than mere transactions. Today, these connections resemble strategic partnerships, built on openness, shared objectives, and mutual respect. As Abbie Mansfield from Arch UK aptly put it:

"The broker-underwriter relationship continues to positively evolve into partnerships that are increasingly transparent, collaborative and solution focused"

This shift has brought tangible benefits across various business areas. Working together, brokers and underwriters craft tailored policies that not only drive business growth but also improve operational efficiency by cutting costs and speeding up policy issuance. In 2025, Tokio Marine HCC International demonstrated their dedication to this approach by hosting nine "Risk Surgery" and training events, which drew over 300 brokers, fostering a deeper understanding of the trade credit market.

Striking the right balance between a broker’s proactive client focus and an underwriter’s expertise in managing risks lays the groundwork for lasting partnerships.

CreditInsurance.com plays a vital role in this ecosystem by connecting businesses with a wide network of trade credit insurance providers and skilled brokers. This platform simplifies the complexities of risk management, offering unbiased coverage options tailored to unique needs. Whether safeguarding against non-payment risks, entering new markets, or improving cash flow, businesses gain from better-informed decisions, supported by predictive insights from providers monitoring over 85 million companies worldwide every day.

The value of these partnerships is echoed by industry voices like Keith Boyer, Broker Representative, who highlights the core principles behind effective collaboration:

"The keys to success in just about any relationship also apply to the underwriter/broker relationship: respect, honesty, regard for each other’s abilities, an understanding of each other’s constraints, reasonable expectations, collaboration, communication and consistency"

When these principles come together, businesses gain not just coverage but strategic allies committed to supporting their long-term success through meaningful collaboration.

FAQs

What documents do I need to apply for trade credit insurance?

To apply for trade credit insurance, you’ll usually need to provide a few key pieces of information:

- Application Form: This will require basic business details, including your company’s name, address, and any subsidiaries.

- Financial Information: Be prepared to share financial statements or projections to help assess your business’s financial health.

- Receivables and Buyer Details: You’ll need to supply data about your receivables, buyers, requested credit limits, and payment history.

- Broker or Agent Information: If a broker or agent is assisting with the application, their details will also need to be included.

It’s always a good idea to confirm the exact requirements with your insurer, as they may vary.

How can my broker help me get higher credit limits or better terms?

Your broker plays a key role in helping you secure higher credit limits or more favorable terms by using their expertise and connections with credit insurers. They know how to present your business’s financial standing and payment history in a way that highlights its strengths. Beyond that, they guide you through the application process step by step. Brokers also break down underwriting criteria, making sure your application aligns with what insurers are looking for. This approach not only boosts your chances of approval but also helps you secure credit terms that fit your specific needs.

What can I do to avoid claim denials under my policy?

To ensure your claims are processed without issues, it’s crucial to stick to your insurer’s guidelines and procedures. Here are some key practices to follow:

- Report claims promptly: Timely reporting is essential to avoid delays or denials.

- Provide accurate information: Double-check the details you provide during the application process to prevent discrepancies.

- Understand your policy: Familiarize yourself with your coverage limits and exclusions to avoid surprises.

- Keep communication clear: Maintain open and transparent communication with your insurer throughout the process.

- Submit proper documentation: Ensure all required paperwork is complete and submitted on time.

- Be mindful of restrictions: Some policies may have geographic or industry-specific limitations, so be aware of these.

Avoiding delays, especially in claim reporting, can make the entire process much smoother and improve the chances of approval.