Predictive analytics helps businesses foresee and manage risks by analyzing data and identifying patterns that indicate potential issues. It’s widely used in industries like finance to detect fraud, predict defaults, and manage credit risks. By combining internal data (like payment histories) with external factors (such as market trends), companies can take proactive steps to prevent losses and improve decision-making.

Key Takeaways:

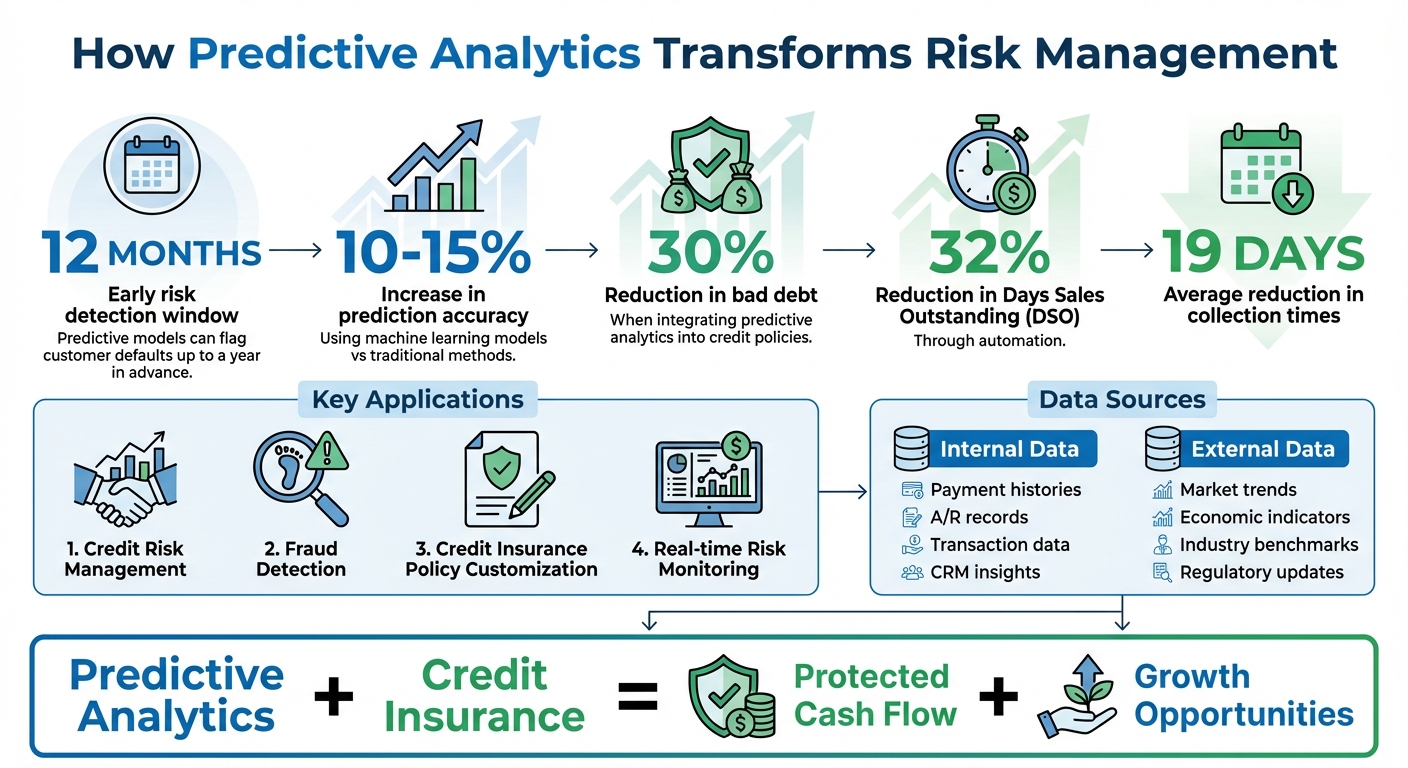

- Early Risk Detection: Predictive models can flag risks like customer defaults up to 12 months in advance.

- Data Sources: Internal data (e.g., accounts receivable) and external data (e.g., economic indicators) provide a full risk picture.

- Improved Accuracy: Machine learning models increase prediction accuracy by 10–15%.

- Applications: Used for credit risk management, fraud detection, and tailoring credit insurance policies.

- Real-time Insights: Combines historical data for long-term trends with real-time data for immediate action.

By integrating predictive analytics into credit policies, businesses can reduce bad debt by up to 30%, shorten collection times, and improve financial stability. Pairing these insights with credit insurance further protects cash flow and supports growth opportunities.

Predictive Analytics Impact on Risk Management: Key Statistics and Benefits

Predictive Models Are Reshaping Global Finance | Here’s How

sbb-itb-b840488

Data Sources for Building Predictive Models

Using predictive analytics to identify industry risks starts with tapping into a variety of data sources. Strong predictive models rely on a mix of internal records and external data to provide the full picture. Internal data lays the groundwork, while external inputs add essential context about the market forces influencing your customers.

Internal Data: Customer Payment Histories and Trends

Your internal systems hold a treasure trove of data. Accounts receivable (A/R) records are at the heart of any predictive model. These include payment history, billing and collections data, invoice-to-cash metrics, and A/R aging reports. Together, these elements paint a clear picture of which customers are reliable payers and which might be at risk of financial trouble.

Diving deeper, transactional data such as purchase orders, receipts, dispute records, and chargeback trends can reveal early warning signs of credit risk. CRM systems add another layer of insight, offering details like sales notes, call logs, and satisfaction scores that could flag potential disputes or customer churn. Financial metrics, including cash flow, revenue trends, and debt-to-income ratios, help assess a customer’s ongoing ability to pay.

"In A/R, predictive analytics would leverage your billing and collections records and data to predict the payment behaviors of current and potential customers." – Chris Couch, Invoiced

Automation in A/R processes can significantly improve efficiency, reducing Days Sales Outstanding (DSO) by 32% and shaving about 19 days off collection times. However, the accuracy of predictive models hinges on the quality of the data. Keeping records clean and up-to-date is critical for reliable results.

External Data: Market Trends and Economic Indicators

While internal data is invaluable, it doesn’t capture the broader market landscape. For example, if a customer’s payments start slowing down, how do you know if it’s due to their individual challenges or an industry-wide downturn? This is where external data sources come in. Market research, economic indicators, regulatory updates, and industry benchmarks provide the context needed to interpret internal metrics.

Key economic factors like inflation, interest rates, and sector-specific benchmarks can help distinguish between isolated customer issues and larger economic trends. Non-traditional data sources – such as social media sentiment, global threat feeds, and even satellite imagery – can further enhance model accuracy. By combining internal transaction data with external credit scores and economic insights, businesses can fine-tune risk assessments and reduce default rates.

"Organizations that rely only on internal data are navigating today’s complex business environment with partial visibility." – Certainty Infotech

When incorporating external data, it’s essential to establish clear governance protocols to ensure compliance and maintain data accuracy.

Real-Time Data vs. Historical Data

Balancing historical and real-time data is another key aspect of effective predictive modeling. Each type serves a distinct role. Historical data forms the backbone of model training, highlighting long-term patterns and establishing baseline metrics like Probability of Default (PD). It provides answers to "what happened" and uncovers recurring trends or behaviors.

On the other hand, real-time data is vital for detecting immediate risks and adjusting risk scores dynamically during sudden market shifts. For instance, real-time feeds can flag abrupt changes in a customer’s payment behavior, prompting a quick review.

The choice of data depends on the speed of decision-making. Real-time data works best for high-frequency decisions like transaction monitoring or credit approvals. Historical data is better suited for low-frequency tasks, such as annual credit policy reviews or long-term planning. Businesses that integrate both types of data into AI-driven models often achieve 10–15% higher prediction accuracy compared to traditional methods. However, models based on historical data need regular updates to keep pace with changing market conditions.

| Data Type | Primary Use | Key Advantage |

|---|---|---|

| Historical | Model training, trend analysis, long-term forecasting | Establishes baseline metrics |

| Real-Time | Immediate underwriting, fraud detection, dynamic scoring | Enables quick responses to sudden changes |

Building and Customizing Predictive Models for Industry Risks

Once you’ve gathered high-quality data, the next step is to craft models that align with your industry’s risk landscape. This involves selecting the right algorithms, training them thoroughly, and tailoring them to address specific challenges. The ultimate goal? A system that delivers actionable insights.

Choosing the Right Predictive Algorithms

The choice of algorithm depends on your objectives and the complexity of your data. For straightforward predictions, like estimating the likelihood of a loan default or calculating credit exposure, regression analysis is a reliable option. It’s particularly appealing in regulated environments because its decision-making process is easy for regulators to understand.

For more complex scenarios, decision trees and random forests excel at segmenting customers based on multiple factors, such as credit scores or fraud indicators. Random forests improve accuracy by combining the results of several decision trees running simultaneously. When dealing with massive datasets and intricate patterns, neural networks are ideal. And if you’re forecasting trends over time – like stock market movements or interest rate changes – time series analysis is the way to go.

Explainable machine learning models often outperform older predictive techniques by 10% to 15%. However, selecting between traditional statistical models and machine learning isn’t always simple. Statistical models, like regression, offer transparency and are easier to explain, while machine learning models adapt faster and provide greater accuracy in dynamic situations.

Training Models with Relevant Data

Even the most advanced algorithms can’t compensate for poor data. Start by defining clear objectives that align with both business needs and regulatory requirements, such as Basel III/IV or CECL standards. Data preparation comes next – this includes addressing missing values, identifying outliers with methods like z-score thresholds, and standardizing formats across datasets.

"Machine learning models can only perform as well as the data they ingest." – Alon Gubkin, Aporia

A critical step in this process is feature engineering, where you create variables that drive predictions. For example, behavioral features like rolling averages of late payments, derived metrics like debt-to-income ratios, and seasonal indicators for defaults can significantly boost predictive power. Tools like Principal Component Analysis (PCA) help identify key predictors, reducing data storage needs while enhancing accuracy.

Before deploying your model, validate it against a separate dataset to avoid overfitting. Use metrics like the Area Under the ROC Curve (AUC), Gini Coefficient, and Kolmogorov–Smirnov (KS) statistic to assess reliability. Continuous monitoring is also crucial – if metrics like the Population Stability Index (PSI) exceed thresholds (e.g., PSI > 0.25), it’s time for recalibration.

Customizing Models for Industry-Specific Risks

Generic models often miss critical nuances unique to specific industries. To address this, incorporate sector-specific data and variables. For example:

- In mining, include geological surveys, data on subterranean stability, and operator fatigue levels to predict collapses or equipment-related injuries.

- Transportation firms can leverage vehicle telematics, driver behavior, and traffic/weather data to optimize routes and reduce accidents.

- For manufacturing, machine vibration data and maintenance logs help foresee equipment failures, minimizing unplanned downtime.

- In retail, analyzing inventory demand cycles and customer complaint trends aids in preventing stockouts and reducing churn.

- Financial institutions can monitor borrower profiles and real-time transaction patterns to detect fraud and potential loan defaults.

| Industry | Key Data Sources | Primary Risk Applications |

|---|---|---|

| Mining | Geological surveys, subterranean stability data, operator fatigue levels | Collapse prevention, injury reduction |

| Transportation | Vehicle telematics, driver behavior patterns, traffic/weather data | Route optimization, accident prevention |

| Manufacturing | Machine vibration data, maintenance logs | Predictive maintenance, downtime reduction |

| Retail | Inventory demand cycles, customer complaint trends | Stockout prevention, churn reduction |

| Finance | Borrower profiles, real-time transaction patterns | Default detection, fraud prevention |

The secret to effective customization lies in collaboration. Pair data scientists with industry experts – like risk managers, safety officers, or operations specialists – who can provide insights that raw data alone can’t reveal. Start small with a well-defined use case, such as predicting equipment failure or customer churn, and scale up from there. To keep your models accurate, regularly update them with the latest data as market conditions shift. This approach ensures that your predictive models remain relevant and effective in managing risks.

Applying Predictive Insights to Identify and Reduce Risks

Using strong data sources and tailored predictive models, businesses can turn risk identification into actionable strategies. This approach helps spot at-risk customers before they default, prepare for economic challenges, and incorporate predictive intelligence into routine credit decisions.

Flagging High-Risk Customers and Industries

Predictive analytics can uncover early signs of risk. For instance, Probability of Default (PD) modeling – using logistic regression or neural networks – estimates the likelihood of default within a specific timeframe, often 12 months. These systems can pick up on subtle indicators like changes in payment patterns or rising debt-to-income ratios, even if a customer is still making payments on time.

By combining internal transaction data with external market trends, businesses can pinpoint vulnerabilities. Analytics tools compare a client’s performance against industry benchmarks, identifying risks tied to declining sectors or economically unstable regions. Machine learning further enhances this process by analyzing vast amounts of unstructured data, detecting complex patterns, and flagging unusual behaviors or high-risk profiles that might escape traditional models.

Take the example of Infosys, which developed a machine learning-based credit risk engine for a mining company between 2024 and 2025. By analyzing four years of historical data – such as Letters of Credit, commodity prices, and exchange rates – the system identified countries, products, and payment terms with the highest default risks. It also revealed mismatches between certain product categories and payment terms that led to spikes in defaults. Now, this system forecasts credit risks up to a year in advance and suggests tailored supply chain financing plans based on specific risk profiles. These insights also support stress testing under various economic scenarios.

| Risk Metric | Definition | Business Application |

|---|---|---|

| Probability of Default (PD) | Likelihood of non-payment within a set period (e.g., 1 year) | Used to approve or deny credit requests |

| Exposure at Default (EAD) | Total potential loss if a customer defaults | Helps set maximum credit limits |

| Loss Given Default (LGD) | Percentage of exposure unlikely to be recovered | Guides bad-debt reserves and insurance planning |

| Propensity to Pay | Likelihood of settling debt during collections | Improves and automates debt collection strategies |

Scenario Planning and Stress Testing

Predictive models allow businesses to prepare for economic shocks by simulating their potential effects on financial performance. Historical data, such as borrower default rates during the 2008 financial crisis or the COVID-19 pandemic, helps companies understand how their portfolios might respond to future stress.

Sensitivity analysis examines the impact of specific risk factors, like sudden tariffs or currency swings, on credit portfolios. Meanwhile, portfolio-level testing assesses credit exposure across regions, industries, or key counterparties to identify vulnerabilities that could lead to cascading losses. Companies using these predictive techniques in their credit departments have reported reducing bad debt provisions by 25% to 30%.

"By combining our world-class expertise with the wealth of our global data assets and the power of cutting-edge technologies (artificial intelligence, data science), our clients benefit from more intelligent solutions that inform their decisions and enable them to manage commercial risks in a more predictive way."

- Guillaume Huguet, Data Lab Director, Coface

These insights naturally refine credit risk policies, making them more proactive and responsive.

Integrating Insights into Credit Risk Policies

To make the most of predictive insights, businesses need to integrate them into daily credit operations. This includes adjusting credit lines and identifying upselling opportunities based on evolving risk profiles. Automated exposure management systems can ensure that risk exposure stays within predefined limits for each client. Early warning signals, like shifts in cash flow or debt-to-income ratios, can prompt timely interventions to prevent defaults.

For example, Experian partnered with a major retail credit card issuer between 2020 and 2023 to overhaul an outdated acquisition model. By leveraging proprietary data and advanced modeling techniques, they developed a new predictive model that improved risk identification by 10% across customer segments while adhering to strict governance standards. This demonstrates how embedding predictive insights into underwriting decisions can yield measurable improvements.

Businesses can also use these insights to modify payment terms or credit limits for high-risk clients and specific product groups. Comprehensive portfolio segmentation helps identify high-risk segments, such as industries sensitive to economic changes. Additionally, using explainable AI ensures compliance with regulations like the Fair Credit Reporting Act, making underwriting decisions transparent and easier to understand. This transparency fosters trust and keeps businesses aligned with regulatory expectations in a fast-evolving environment.

Using Predictive Analytics with Credit Insurance

Predictive analytics transforms credit insurance from a reactive tool for loss recovery into a proactive strategy for managing risk. By leveraging these insights, businesses can integrate advanced credit insurance into broader risk management plans. This approach helps identify potential defaults early, allowing companies to prevent losses rather than merely recover from them. The result? Reduced financial exposure and smarter credit extension decisions.

Improving Risk Protection with Credit Insurance

Combining predictive models with credit insurance policies enhances underwriting precision. Instead of relying on generalized industry categories, insurers can now assess risks using individualized scoring. These scores are based on internal payment records and external data sources like financial statements and geospatial trends. This means premiums and coverage limits are tailored to reflect a company’s actual risk profile rather than broad industry averages.

Real-time data integration further strengthens risk management. Insurers can dynamically adjust credit limits and policy terms as market conditions evolve. For example, predictive analytics has streamlined claims processing, boosting customer satisfaction by 15% through faster and more transparent resolutions.

Fraud detection also benefits from machine learning. By analyzing historical patterns, algorithms can identify inconsistencies in new claims 20% more effectively than manual reviews. Considering fraudulent claims cost the U.S. insurance industry about $80 billion annually, this capability offers substantial financial protection.

Beyond risk protection, predictive insights also enhance financial flexibility, turning insured receivables into assets that drive business growth.

Using Insured Receivables to Support Business Growth

Insured receivables open doors to larger credit lines and enable businesses to expand into higher-risk markets without endangering cash flow. With credit insurance backing their accounts receivable, companies can use these assets as collateral to secure better financing terms. This creates a growth cycle: predictive analytics identify reliable customers for extended credit, insurance safeguards those receivables, and the insured portfolio unlocks new capital for expansion.

By combining risk management and financing benefits, predictive analytics ensures coverage aligns seamlessly with a business’s unique needs.

Customizing Coverage Based on Predictive Insights

Predictive analytics allows businesses to fine-tune credit insurance coverage to match specific customer segments and industry risks. Instead of applying one-size-fits-all policies, companies use risk scores to determine which accounts require higher coverage and which can operate with lower premiums.

For example, predictive models can incorporate external data like commodity price fluctuations for manufacturers or geospatial trends for regional distributors, refining coverage terms accordingly. Insurers using these models have reduced loss ratios by up to 5% and increased EBIT by 20%. Additionally, Natural Language Processing (NLP) can analyze unstructured data, such as claims notes and emails, to detect early signs of financial trouble that traditional methods might overlook.

This data-driven customization ensures credit insurance policies align closely with actual risk exposure, offering maximum protection while keeping costs in check. For businesses navigating the complexities of risk-based pricing and policy customization, resources like CreditInsurance.com provide valuable guidance on selecting and tailoring coverage based on predictive insights.

Conclusion

Predictive analytics has evolved into more than just a tool for anticipating risk – it’s now a key driver of proactive financial strategies. By blending internal payment histories with external market trends and real-time monitoring, businesses can identify potential defaults as far as 12 months in advance. This kind of foresight empowers credit teams to make timely adjustments, such as revising terms, securing protective coverage, or deploying early warning systems to prevent financial challenges from escalating.

When paired with credit insurance, predictive insights offer a powerful combination: safeguarding cash flow while simultaneously opening doors to growth. This approach helps businesses strike a balance between extending credit strategically and avoiding overly cautious or risky policies. Predictive models provide clarity on which customers are suitable for extended credit and which require protective measures.

Companies that have embraced automation and predictive tools for more than half of their operations saw a 32% drop in Days Sales Outstanding (DSO) – a reduction of 19 days. Additionally, predictive risk scoring transforms insured receivables into assets that can attract better financing terms and support expansion into new markets, all without compromising financial stability.

FAQs

What data do I need to start predicting customer default risk?

To assess the likelihood of customer default, it’s crucial to gather essential information like payment history, financial data, and transaction records. These elements form the foundation for creating models that evaluate creditworthiness. Adding layers of insight – such as supply chain connections, market trends, and behavioral patterns – can improve the precision of these predictions. Access to both historical and real-time data plays a key role in making predictive analytics more effective for identifying default risks.

How often should a credit risk model be retrained as market conditions change?

Credit risk models need regular retraining to stay in tune with shifting market conditions and emerging data trends. Most often, this happens either monthly or quarterly, depending on how rapidly the market environment evolves. These consistent updates are crucial for maintaining the model’s accuracy and its ability to effectively pinpoint potential risks.

How do predictive risk scores change my credit insurance coverage and limits?

Predictive risk scores play a key role in shaping credit insurance coverage by evaluating a customer’s likelihood of default through advanced modeling techniques. When these scores indicate a higher level of risk, insurers may reduce coverage limits to protect against potential losses. On the flip side, lower-risk scores can result in increased coverage limits, giving businesses the flexibility to offer more credit to their customers. By aligning coverage with the assessed risk, these scores help strike a balance between minimizing exposure to defaults and fostering opportunities for growth.