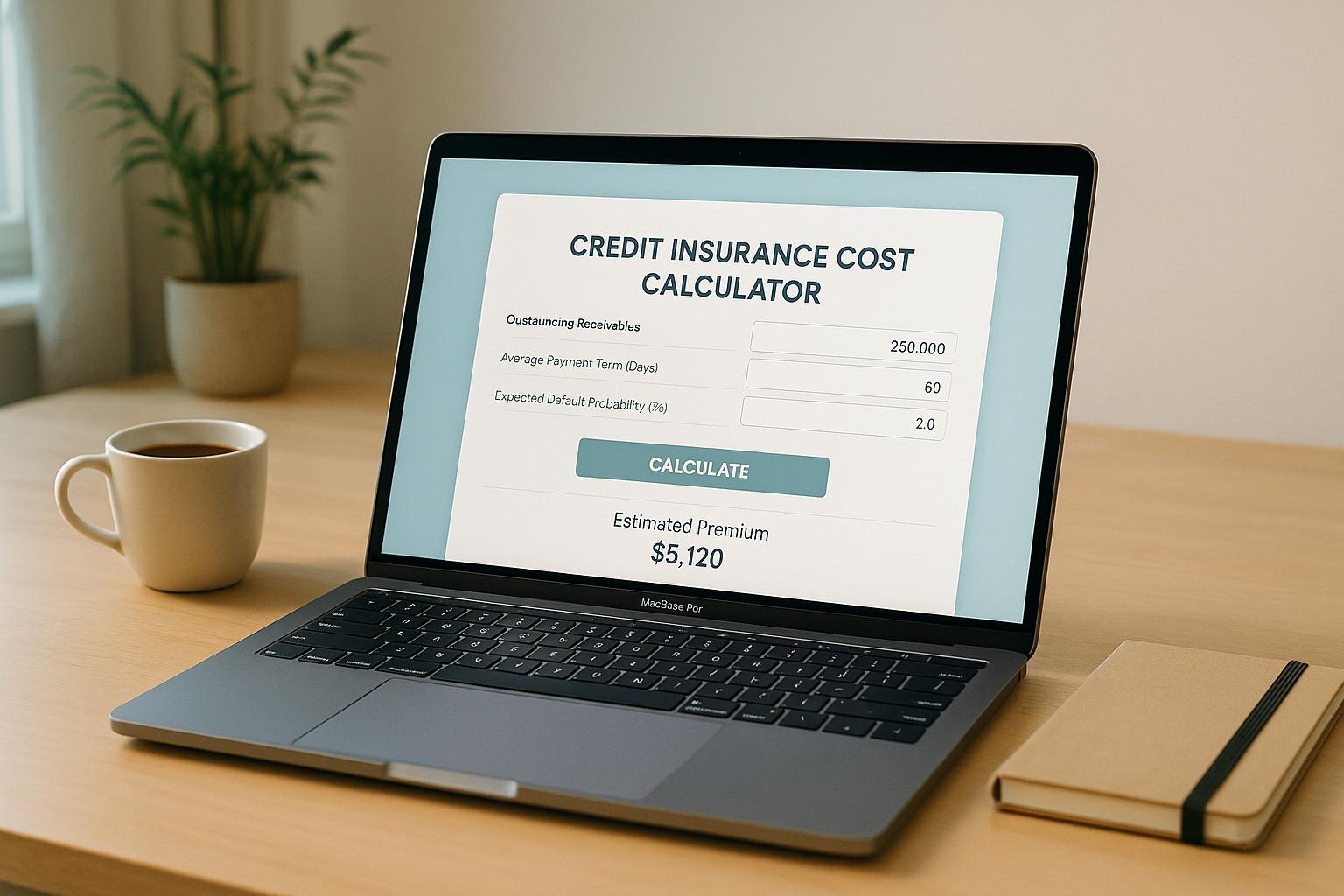

Understanding Credit Insurance Costs with Our Calculator

When taking out a loan, protecting yourself from unexpected financial setbacks is a smart move. Credit protection plans can cover your payments if life throws a curveball, but how much do they cost? That’s where a tool like our Credit Insurance Cost Calculator comes in handy. It’s designed to give you a quick, no-strings-attached estimate of what you might pay monthly to safeguard your loan.

Why Estimate Your Premium?

Loans come in all shapes and sizes, from personal borrowing to hefty mortgages. The cost of insuring that debt depends on factors like the amount you’ve borrowed and how long you’ll be paying it back. Our tool breaks it down by letting you input your specific details—think loan size and repayment term—and spits out an estimated premium in seconds. It even factors in interest rates if you’ve got that info. This isn’t just about numbers; it’s about planning ahead. Knowing the potential cost of a credit protection plan helps you budget better and decide if this safety net fits your needs. So, whether you’re curious or seriously considering coverage, start with a simple estimate to get the conversation going.

FAQs

What exactly is credit insurance, and do I need it?

Credit insurance protects you by covering loan payments if you’re unable to pay due to events like job loss, disability, or death. Whether you need it depends on your situation. If you’re worried about unexpected financial hiccups, it can offer peace of mind, especially for larger loans. But it’s not mandatory, and costs vary, so weigh the premium against your budget and risk tolerance.

How accurate is this credit insurance cost calculator?

Our calculator provides a solid ballpark figure based on standard industry formulas, like factoring in 0.5% of your loan amount as a base premium, adjusted for term length and interest rate. That said, it’s not a final quote. Actual costs depend on the insurance provider, your credit profile, and other personal factors. Use this as a starting point, then chat with a provider for specifics.

Does a longer loan term always mean higher insurance costs?

Generally, yes. A longer loan term increases the risk for insurers since there’s more time for something to go wrong, like a job loss or health issue. Our tool adjusts the premium upward based on term length—basically, it assumes more years equals more exposure. But other factors, like your loan amount or provider policies, also play a role, so it’s not a straight line.